Overview of current merger and acquisition activities (M&A) in the payments market

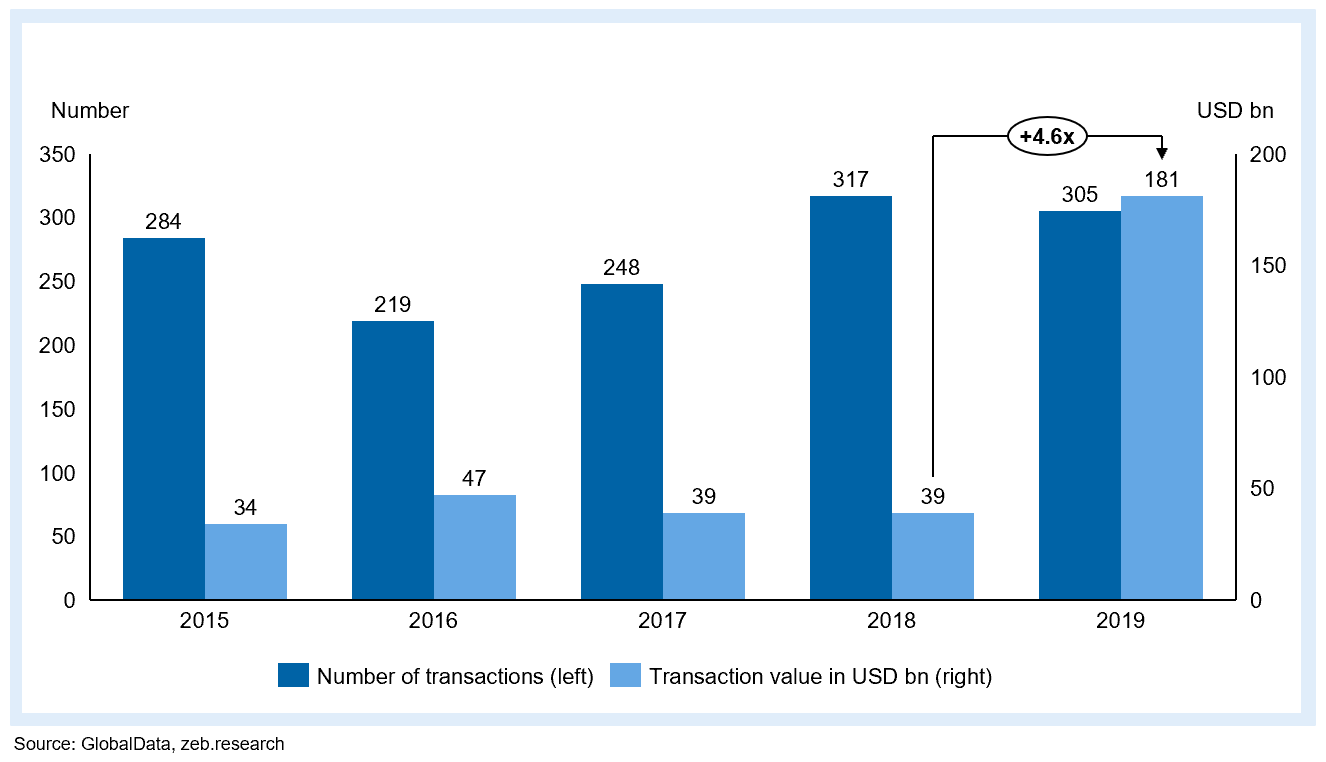

The ongoing consolidation of the payments sector began as early as in 2000 with some smaller activities amongst bank-independent payments-specialists. In particular, the withdrawal of banks from the payments business (e. g., the sale of Concardis by a consortium of German private banks, cooperative banks, the savings bank sector and DZ BANK in 2017) and the trend towards digital payments contributed to this development. Since then, we are observing a steady increase in transactions, with over 300 M&A deals both in 2018 and 2019.[2] There are two clearly identifiable trends. First, the payments industry currently holds great appeal for investors. For instance, private equity leading firm KKR bought Heidelpay while a consortium of Bain Capital and Advent acquired Concardis, only to exchange shares with nets shortly afterwards, which is owned by investors Hellman & Friedman. Second, the industry itself consolidates at all levels.

Figure 1: (Worldwide) M&A transactions in the payments sector

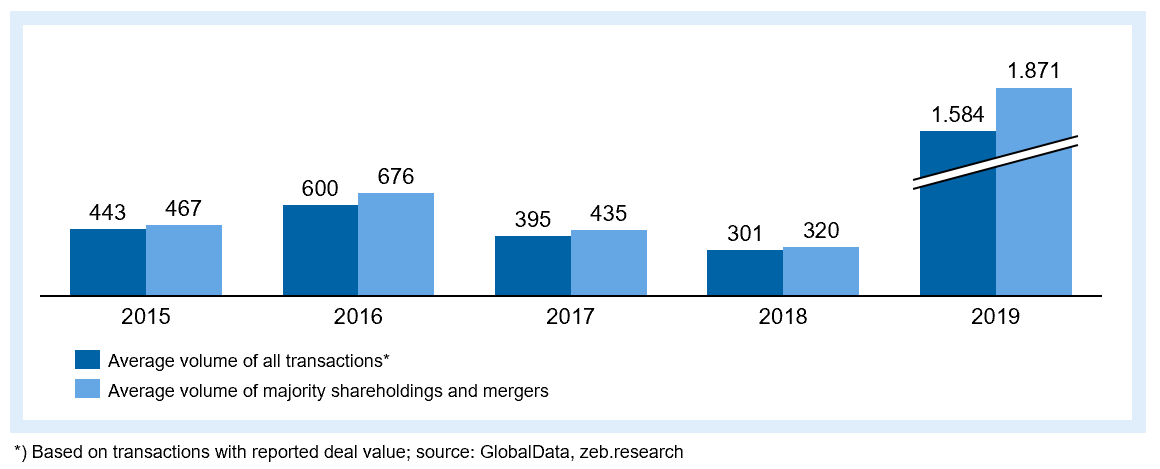

Figure 1: (Worldwide) M&A transactions in the payments sectorIn 2019 for example, the volume of transactions communicated in connection with large acquisitions (e. g., Fidelity Information Services (FIS) and Worldpay or Fiserv and First Data) totaled at approximately USD 180 bn, which surpassed the combined total of the previous period from 2015 to 2018. A closer look at the average deal volume of all completed M&A activities reveals a sharp increase in 2019.[3] In other words, this means that the average value of a transaction (irrespective of the equity stake) was around USD 1.6 bn in 2019. Taking into account only majority deals, this ratio even rises to just under USD 1.9 bn (see Figure 2). These dynamics appear to continue in 2020 and underline the trend that individual players can achieve growth and market share gains especially through acquisitions.[4]

Figure 2: Average transaction value in the payments sector (worldwide, in USD m)

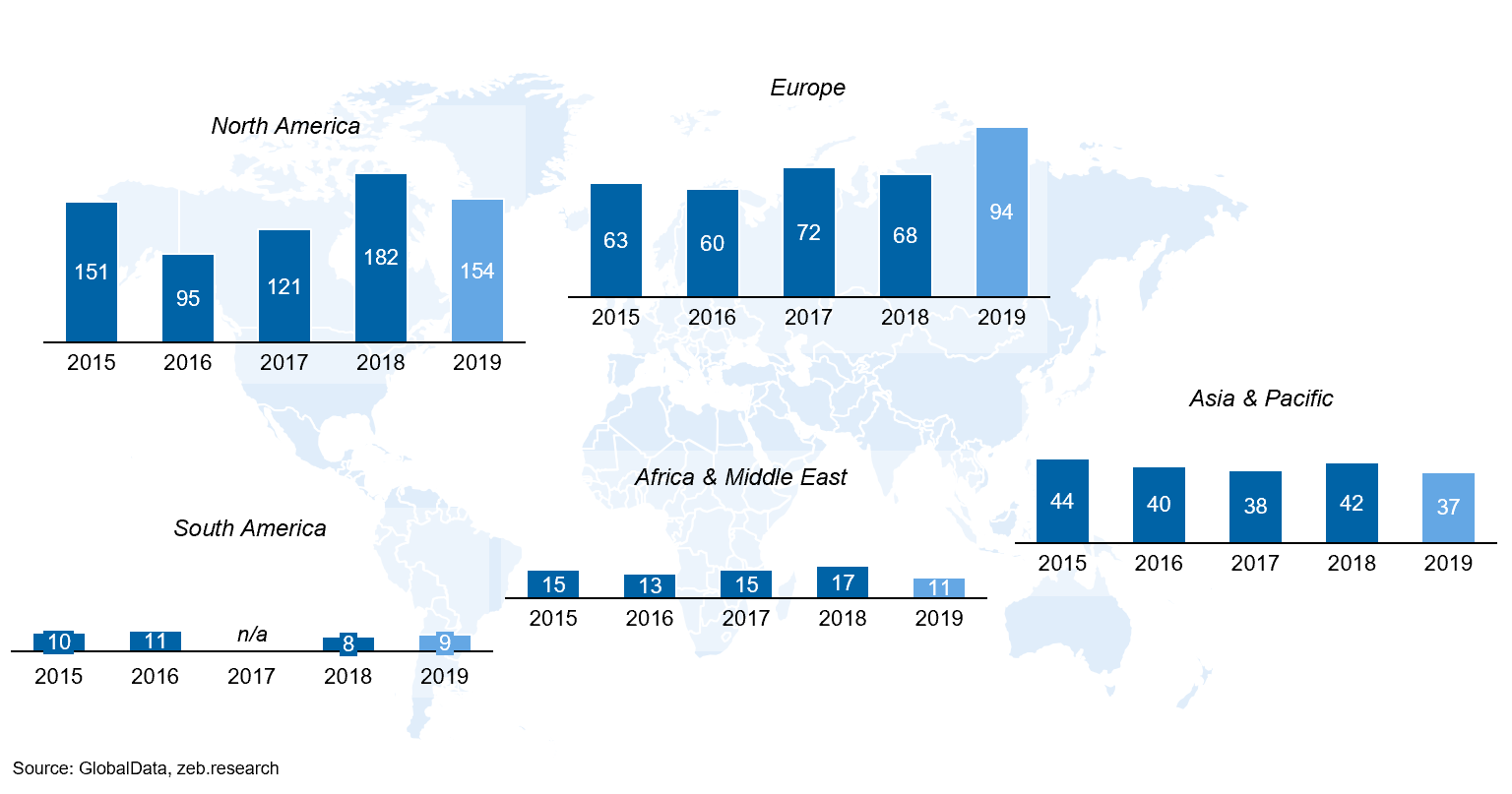

Figure 2: Average transaction value in the payments sector (worldwide, in USD m)The consolidation of the payments sector is a global phenomenon. Nevertheless, activities to date are largely limited to acquisitions and mergers within individual regions. North America and Europe are the most active regions with 154 and 94 M&A deals respectively in 2019. By comparison, we observe significantly fewer transactions in Asia, which have remained at a constant level over the past years.

Figure 3: Number of transactions in the payments sector by region

Figure 3: Number of transactions in the payments sector by regionM&A rationales in the payments market

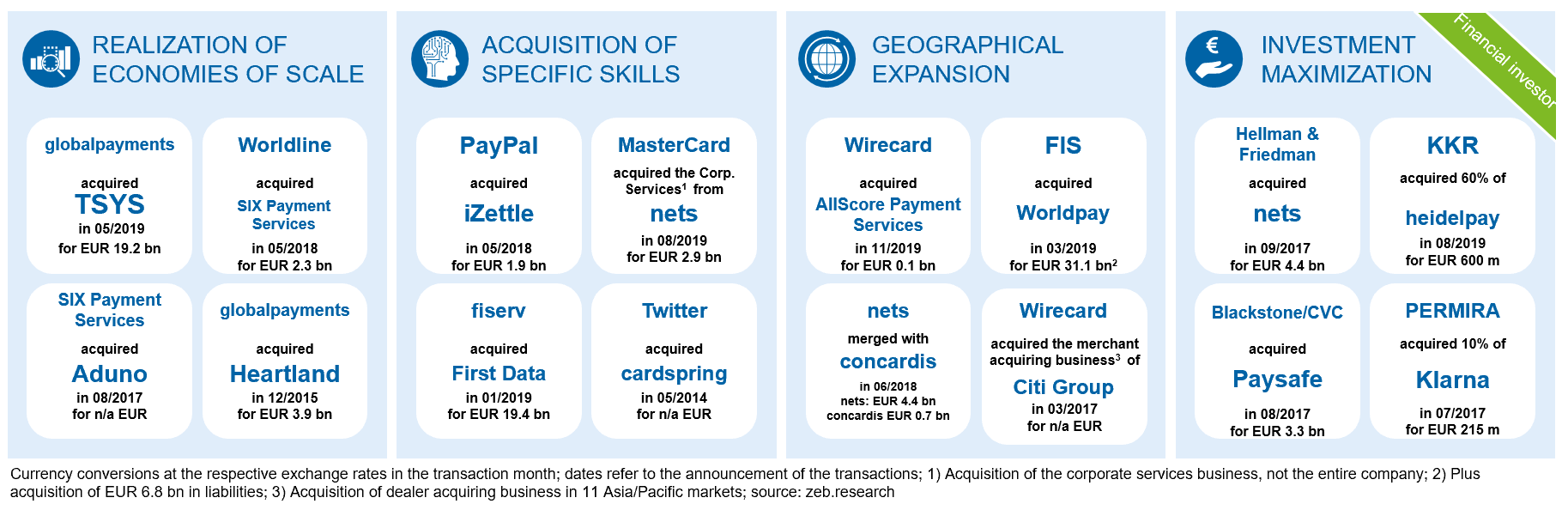

Three main drivers for strategic investors account for the observable consolidation activities in the payments market.

- Realization of economies of scale

By acquiring competitors, payment providers can quickly broaden their customer base and, in addition to cross-selling potential, improve infrastructure utilization and thus realize cost advantages. Especially in payment processing and considering the systems required for regulatory purposes, fixed cost degression results in clear cost synergies. As a mass business, payment processing as such generates low earnings per transaction and is therefore not immediately highly profitable. Thus, it is also possible to amortize the high investments currently required in IT and infrastructure[5] more quickly. One goal of increased size may also be to remove smaller competitors from the market via acquisitions.The merger between Global Payments and Total System Services (TSYS) in May of 2019 with a volume of around EUR19 bn represents a good example of such a strategic move.[6] This large-scale merger created a leading global payments specialist, which provides payment technology and software for more than 3.5 million merchant customers and 1,300 financial institutions in over 100 countries. Besides realizing economies of scale, the two US companies designed their merger specifically to expand the market position in the area of payment software. The creation of a globally operating and diversified payment transaction specialist enables a broad orientation towards the most attractive markets. In addition, the merged entity also benefits from an improved financial profile and increased financial flexibility. - Acquisition of specific skills

Mergers and acquisitions can serve to acquire specific (complementary) skills of the target company. If payment service providers specialize in certain market niches or offer specific technologies, competencies or resources that cannot be build up organically or within a short time span, these companies are attractive targets for M&A activities. In particular, the acquisition of innovative payment technologies against the background of rapidly changing customer needs and mobile payments are key drivers. Purchasing data analytics expertise can play a decisive role for payment service providers. The systematic evaluation of cash flows can provide valuable information for the company’s own risk management and for calculating credit default probabilities, among other things. Furthermore, companies can also implement additional approaches to monetize the data, whereby the particularly good access to consumer and merchant data of the payment providers represents a significant added value. Companies operating outside the payment or financial services market can also (once again) extend their value chain to include payment transactions.

In August of 2019 for example, Mastercard acquired a majority stake in the corporate services business of the Danish company nets. The targeted acquisition of technology and services served to provide real-time account-to-account (A2A) payments and underlines the continuation of the strategic expansion of Mastercard’s own positioning beyond the card business. To this end, the creation of concrete use cases for instant payments and thus the supplementation of already completed acquisitions (e. g., VocaLink or Transactis) plays a decisive role.

In addition, we perceive that the acquisition of new skills related to the core business (e. g., data analytics and focus on overall shopping experience) gains in importance. Acquirers are currently building up issuing capacities in some areas. Originally, pure payment processors, such as PayPal or Klarna, have recently started offering (small) loans to improve the shopping experience and could also use specific transactions for this purpose. PayPal, for example, has just taken the next step with the acquisition of Honey in the USA and invested several billion Euros into shopping experience. - Geographical expansion

Various hurdles significantly impede organic growth in new geographical markets. The expanding providers are mostly unknown in the target market, are unfamiliar with specific market practices and are exposed to competition from established players. Mergers with and acquisitions of existing payment service providers in the target markets enable a well-directed cross-border expansion of the business area to develop these markets. This minimizes country‑specific risks and facilitates the roll out one’s own successful business model into other markets. The merger of Danish payment specialist nets and German Concardis Payment Group in 2018, for example, has created a leading payment service provider within the payments market with Europe-wide ambitions. The market leader in Northern Europe and one of the leading providers in the DACH region are thus joining forces to accelerate their European expansion. The newly formed group intends to expand its service offering and bring product innovations even faster to a broad European market.

In addition to the three aforementioned rationales, financial investors, such as private equity investors, who pursue different integration approaches and focuses, dominate the payments market. Thus, the business-specific characteristics of many payment service providers are particularly suitable for participating in the often exponential growth curve as well as the observable multiple expansion[7] in the M&A growth market. This is often done by implementing classic measures, such as increasing the management’s professionalism, making add-on acquisitions to optimize the strategic orientation and revising the business model. Through their commitment, they act as catalysts for consolidation in the payments market.

Figure 4: M&A rationale in the payments sector and example transactions

Figure 4: M&A rationale in the payments sector and example transactionsOutlook for merger and acquisition activities

Consolidation in the payments market will continue, particularly due to the intensified competition and the associated pressure on margins. Payment providers need to adapt to rising regulatory hurdles, high fixed-cost infrastructure and growing or rapidly changing customer requirements in order to achieve market relevance. However, they can only accomplish this organically to a limited extent.

zeb believes that the specific characteristics of the payments market and the merger and acquisition activities already observed suggest four core theses on future developments.

- Emergence of a few large and globally active “full-service” providers

We expect a consolidation, especially with regard to payment infrastructure and processing, down to five or six major global players. In particular, we assume that there will be at least one European, one US American and one Asian “champion”, respectively[8], although each of these possess their own world-wide network. Each economic region intends to promote its own system, thereby protecting local players and the local economy. We anticipate further supra-regional and international mergers along the way. Mastercard, for example, is currently in the process of expanding its own portfolio. In the course of the ongoing consolidation process, the number of record deals will decrease as the number of available or suitable assets in a consolidating industry dwindles and regulatory and antitrust requirements become stricter. - Expansion of non-financial service providers’ payments activities

We expect continued M&A activity with regard to payments, especially from online merchants and the major internet ecosystems. Technology companies such as Amazon, Google, Apple and Facebook, for example, are looking for the expansion of their existing payment solutions. A logical step in this context is to strengthen their own payment solutions by integrating further add-on transactions. Small niche providers in particular should be interesting targets. - Emergence of a few selected payments specialists for individual niches

Specialist providers will emerge for individual fields and will, by the means of M&A, bundle related technologies to create a functional, market-leading solution and offer it globally. Similarly, smaller start-ups or disruptors will join forces to better fill their niches through mergers and acquisitions. In this context, key drivers are maximum customer focus and the greatest possible convenience for the customer. Data analytics also plays a major role in better meeting customer demands. A niche may also be a clearly defined regional footprint, for example in cryptocurrencies, as a unique selling point. - Merger of payments and security providers

The increasing importance of mobile payments, among others, further enhances the issue of security as a key aspect of payment transactions. Making account access available within the framework of PSD II[9] requires strong identity and customer authentication as well as improved risk identification and fraud prevention. To strengthen security, we expect an increase in M&A activities between payments service providers and specialists for cybersecurity, fraud prevention and risk detection. In this context, the use of artificial intelligence (AI) for the automated detection of unauthorized access or fraud plays a major role. Providers can generate decisive competitive advantages, especially in the B2B sector with large volumes of individual transactions. We have already noticed initial trends in this area in the past, such as PayPal’s acquisition of Simility, a platform for fraud prevention, and Mastercard’s acquisition of the Canadian company Ethoca, a service provider for identifying and combating fraud in online commerce.[10]

Payment service providers and investors should work out a clear M&A strategy at an early stage, explicitly taking into account the increasing regulatory requirements. Active consolidators face the question of industrializing the M&A deal flow and the subsequent integration.

In this context, the question of how banks will position themselves in the payments market in the future is still open. At present, they often merely provide the account infrastructure that forms the basis of many transactions. Unless they actively address this issue, their room for maneuver will be increasingly restricted. In the face of growing payment service providers, banks also urgently need a clear strategic positioning.

As a “partner for change”, zeb supports financial services providers, investors and fintech companies from strategy definition to implementation. zeb’s holistic consulting approach and in-depth market insight offer special opportunities—from the strategic orientation of payment transactions to buy- and sell-side support in the context of commercial or IT due diligence and the successful and value-oriented integration of an M&A transaction.