The eWpG

With the Electronic Securities Act (eWpG), German lawmakers have created the possibility of issuing electronic securities. Thus, the traditional understanding of a security – a paper certificate – has been transformed by the eWpG coming into force.

Currently, only bearer bonds and shares in investment funds can be issued in electronic form. According to German lawmakers, crypto securities will in future also comprise company shares.

Strong growth expected for crypto securities in Germany

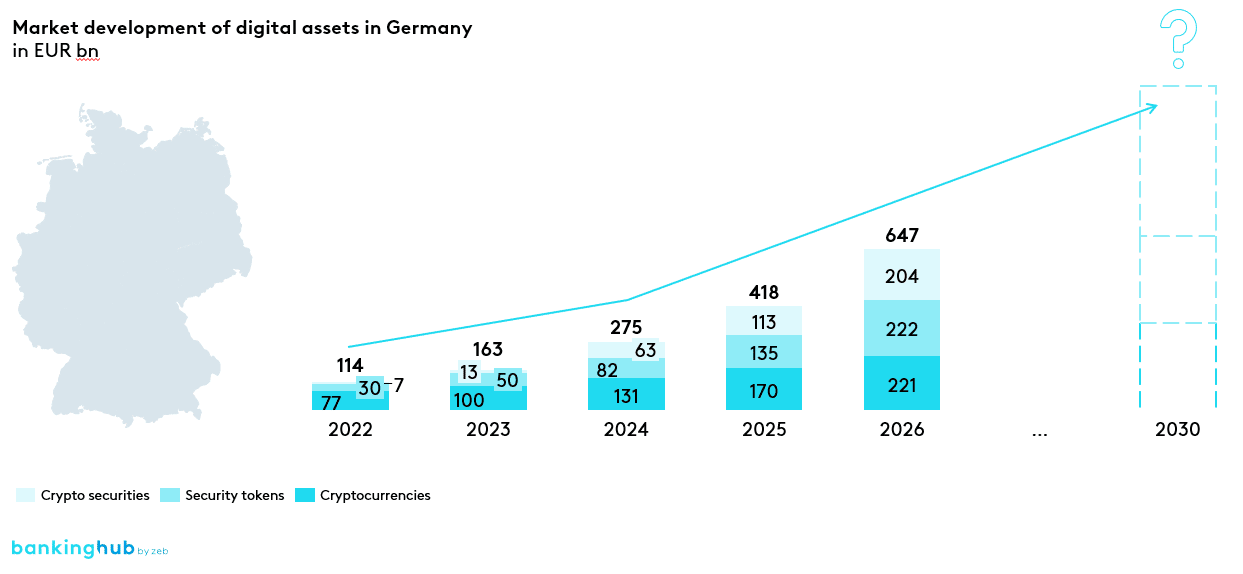

Strong development of the market for crypto securities can be expected in the near future. This year, for example, the market volume in Germany will already amount to an estimated € 7 bn and is expected to grow exponentially to € 63 bn by 2024 as the market infrastructure is progressively established and industry standards are developed. By 2026, the market volume of crypto securities is expected to reach approximately € 200 bn. This would mean that crypto securities would grow faster than other types of digital assets, such as cryptocurrencies or security tokens.

As a result of this development, market participants already offering digital asset services have the opportunity to expand their portfolio to include crypto securities registry services. At the same time, there is an attractive opportunity for firms who are not yet active in the rapidly growing digital asset market to establish a service offering and thus generate new revenue streams.

Crypto securities offer time and cost saving benefits through streamlined processes, reduced intermediation and increased automation

To issue crypto securities, an issuer designates a crypto securities registrar entity. If an issuer does not designate a service provider for the crypto securities registry services, the issuer itself is deemed to be the registrar entity.

However, in these cases, the issuer also needs supervisory permission, which is often overlooked in practice. The lawmakers justify this requirement with the position of trust associated with keeping and managing the register.

In contrast to central registers, the operation of crypto securities registers is not reserved for central depositaries for securities and custodians (holders of a permit for custody business).

From an issuer’s perspective, issuing crypto securities has four key advantages over issuing traditional securities:

- fast and cost-effective issuance due to lean processes (elimination of the central securities depositary),

- automatic and algorithm-based management and updating of the register, as well as the possibility of automating corporate actions (such as coupon payments) by using smart contracts,

- increased transparency and security through the use of a tamper-proof recording system, and

- improved image among technology-savvy customers by offering fully digital products.

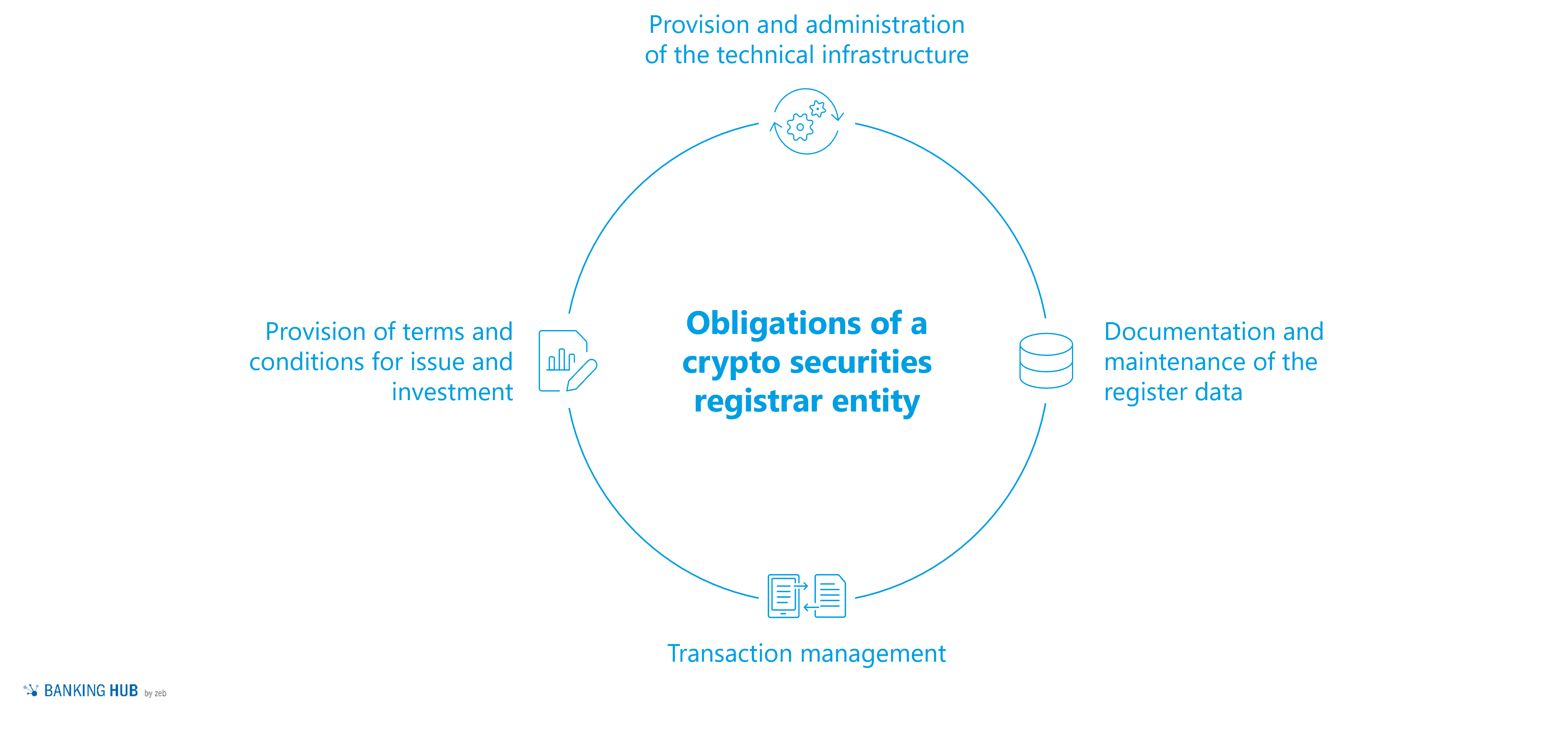

Extensive requirements defined for crypto securities registrar entities

The obligations of a crypto securities registrar entity are essentially derived from the eWpG and the Ordinance on Requirements for Electronic Securities Registers (currently available as an updated draft bill).

The extensive regulatory requirements can be summarized into four key obligations, as shown in the following figure:

Figure 2: Obligations of a crypto securities registrar entity

Figure 2: Obligations of a crypto securities registrar entityProvision and administration of the technical infrastructure

A crypto securities register must be maintained using a tamper-proof recording system in which data is sequentially recorded and stored in a manner protected against unauthorized deletion and subsequent modification.

Such a recording system is a decentralized structure in which control rights are distributed to participating entities according to a predetermined pattern to ensure the integrity and authenticity of the entries. Distributed ledger technology (DLT) systems such as blockchain are particularly suitable for this purpose.

For the technical operation of the crypto securities register and the provision of the infrastructure, the registrar entity may rely on an external service provider.

Documentation and maintenance of the register data

To create an entry for a crypto security, a crypto security registrar entity must document several mandatory details in the crypto security register. The scope of these details depends on whether the security is registered as an individual entry or collectively and includes information regarding the issuer, holder, issue volume and amount, interest rate and maturity of the crypto security. Additionally, the characteristics and the consensus mechanisms of the recording system, as well as the cryptographic methods used, must be specified.

Transaction management

If investors wish to buy or sell crypto securities, an order must be entered via a suitable investor interface.

To carry out the associated transaction, the entry regarding the holder of the crypto security needs to be amended; thus ownership of the crypto security is transferred. Prior to this, the holders who submit a corresponding transfer instruction must prove their identity to the registrar entity by providing suitable evidence.

The crypto securities registrar entity is an obliged entity pursuant to the German Money Laundering Act.

Provision of terms and conditions for issue and investment

It must be ensured that investors have immediate access to the terms and conditions of the issue or investment at any time. For this purpose, the crypto securities registrar entity must store the terms and conditions as a permanent electronic document, publish them on the Internet and link them accordingly in the register.

In addition, the time of changes to the terms and conditions of the issue or investment must be recorded, and changes to the terms and conditions must be numbered consecutively.

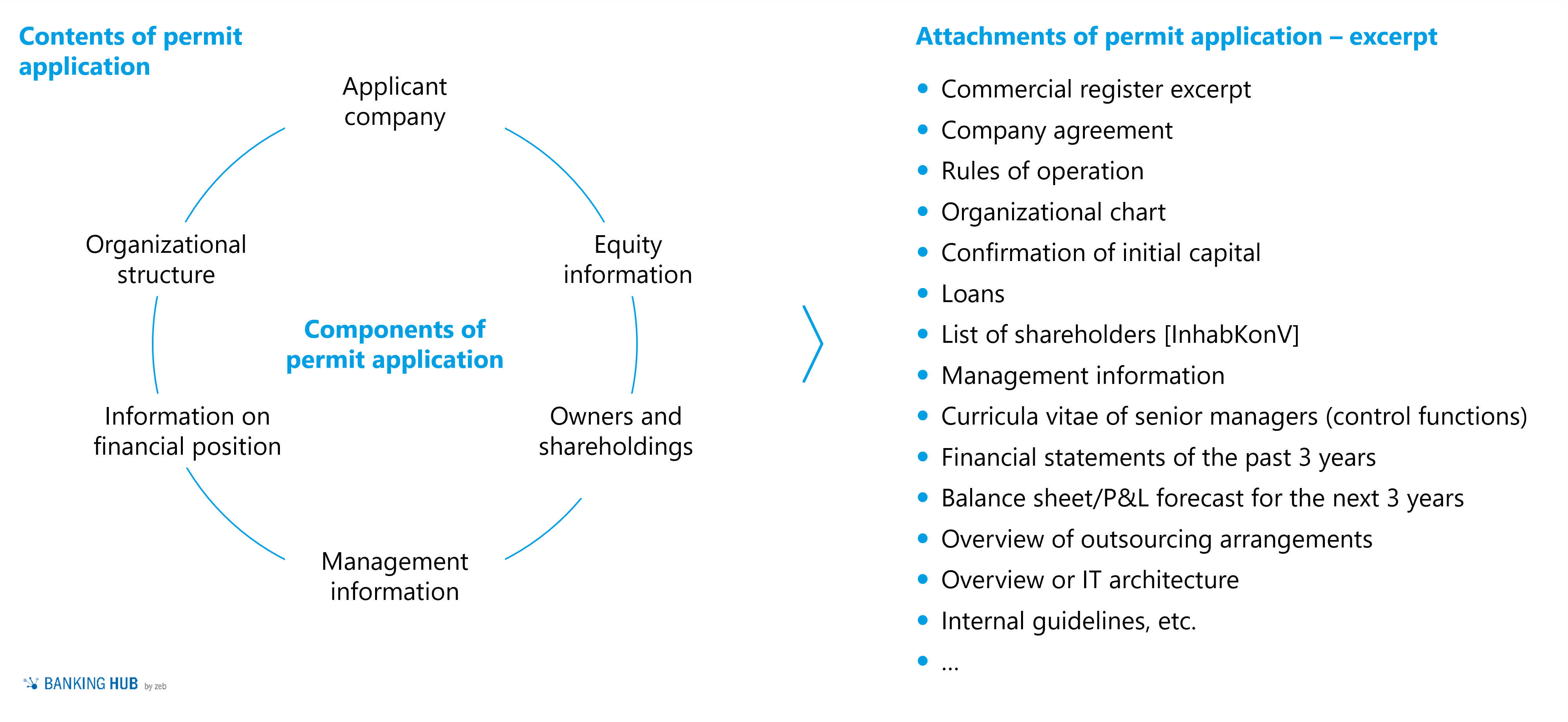

Permit requirement for crypto securities registry services

To operate a crypto securities register, companies require a permit from BaFin.

The application for a permit to operate a crypto securities register must be submitted in writing by the future registrar entity to BaFin and must meet its requirements.

Figure 3: Structure and content of permit application for crypto securities registry services

Figure 3: Structure and content of permit application for crypto securities registry servicesAcute pressure to act arises in particular for companies that have already commenced business operations in December 2021 under the grandfathering arrangement. These companies must submit a full permit application to BaFin by June 10, 2022, at the latest.

However, other market participants who are primarily seeking to strategically develop their business model and wish to offer the crypto securities registry service should also submit a permit application in a timely manner to benefit from a first mover advantage.