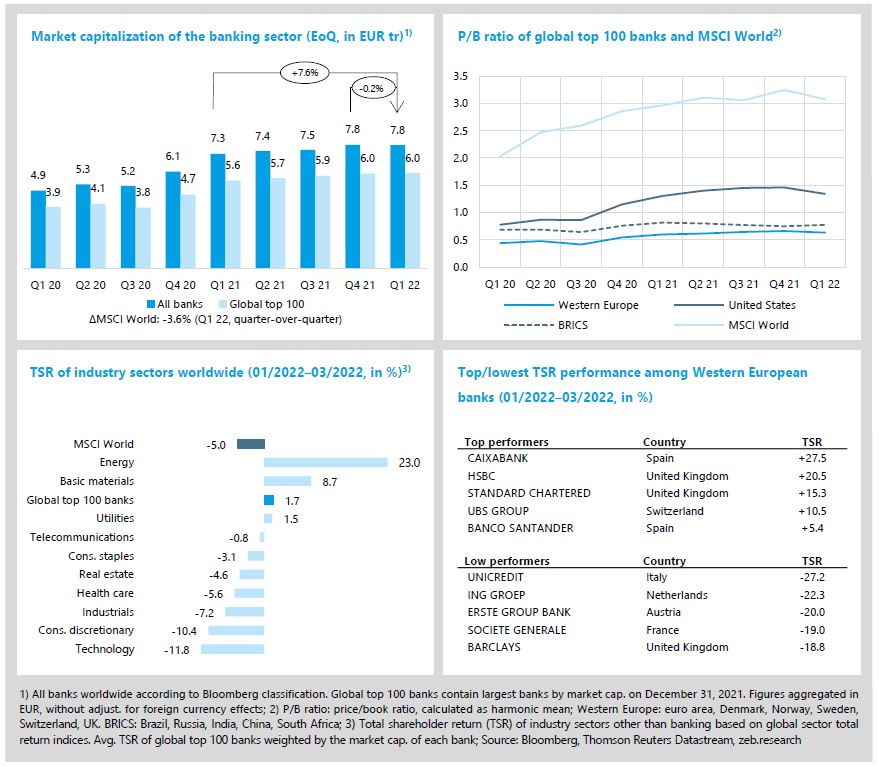

Turbulent first quarter: bank stocks clearly lost momentum

-1.7% QoQ TSR performance of Western European banks

- The Russia-Ukraine war has shocked the world in Q1 2022 and global capital markets went into correction mode (MSCI World TSR -5.0% QoQ).

- Western European banks showed a strong TSR performance during the first weeks of 2022 but lost temporarily around -25.0% and ended Q1 with a TSR of -1.7% QoQ.

After a steady recovery over the previous year, the Russia-Ukraine war has shocked the world in the first quarter of 2022 and global capital markets went into correction mode (MSCI World TSR -5.0% QoQ, market capitalization -3.6% QoQ). Corresponding economic turmoil and dampened interest rate hike fantasies weighed heavily on Western European as well as U.S. bank shares. Especially Western European banks showed a strong performance during the first weeks of 2022 but with the beginning of the war, they lost temporarily shareholder value of around -25.0%. Despite a slight recovery since mid-March, Western European banks ended Q1 2022 with a negative TSR of -1.7% QoQ (vs. global top 100 banks +1.7% QoQ).

- Market capitalization of the overall global banking industry stopped climbing in Q1 2022 but remained on a high level at EUR 7.8 tr (-0.2% QoQ), still +7.6% YoY and even +59.2 % compared to the previous low value in Q1 2020 (EUR 4.9 tr).

- In the first half of Q1 2022, the global top 100 banks continued the strong TSR performance 0f the previous year (+7.4% until mid of February) but lost some momentum since mid of February and ended Q1 2022 with a value of +1.7% QoQ.

- Compared to Western European banks, U.S. banks had a less strong start into the year and lost shareholder value of on average -7.7% QoQ. BRICS banks, dominated by Chinese and Brazilian banks, remained nearly unaffected by the latest market developments and showed a quarterly TSR of +4.7%.

- Average P/B ratios showed corresponding corrections. European banks’ average valuation declined by -0.03x QoQ to 0.63x and U.S. banks’ valuation by -0.12x QoQ to 1.34x (BRICS banks: 0.78x, +0.03x QoQ).

- Among the European low performers of Q1 2022 are in particular banks with significant Russian exposure, mainly from Austria, Italy and France. Unicredit, for example, as one of the largest foreign banks in Russia, ranking 12th by total assets.

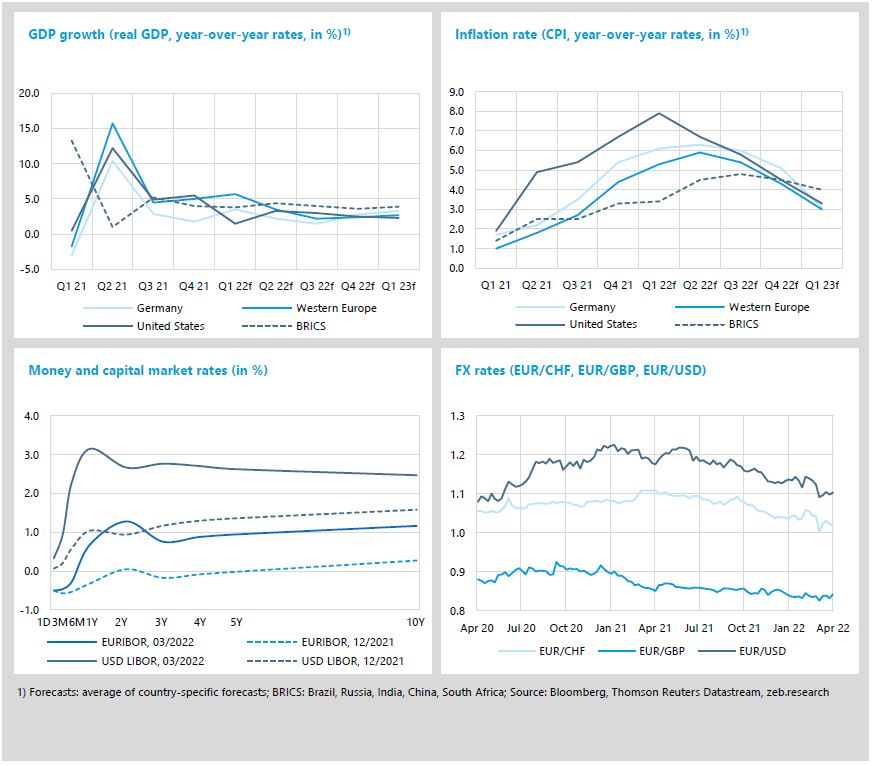

Economic growth prospects deteriorate and inflation is running hot

+5.9% YoY expected Western European inflation rate in Q2

- Economic growth prospects deteriorated in Q1 and inflation is expected to reach new record highs (Western Europe: 5.9% YoY in Q2 22, U.S.: 7.9% YoY in Q1 22).

- Rising inflation expectations have also caused medium to long-term interest rates to increase remarkably, shifting the U.S. and euro area yield curve upwards.

The Russia-Ukraine war has significantly darkened the global economic environment. Supply chain disruptions and increasing energy prices reduced growth expectations already at the beginning of the year but are now becoming a heavy burden on the post-COVID economic recovery. Inflation is expected to reach new record highs (U.S.: 7.9% YoY in Q1 2022, Western Europe: 5.9% YoY in Q2 2022) as prices soar across the board. Rising inflation expectations have also caused medium to long-term interest rates to increase remarkably, shifting the U.S. and euro area yield curve upwards.

- In Q1, the economic growth forecasts for 2022 were revised downwards in the wake of the Russia-Ukraine war. U.S. GDP growth is now expected to reduce to 1.5% YoY in Q1 2022 and afterwards improve again to 2.5% YoY in Q4. Growth in Western Europe is likely to improve by still 5.7% YoY in Q1 but will then also reduce to just 2.5% YoY by the end of 2022.

- The U.S. inflation rate is expected to reach 7.9 YoY in Q1 2022, the highest value since 1982 and will decrease continuously to 4.5% YoY in Q4 2022. Western European rates will peak with a quarter delay and are expected to reach 5.9% YoY in Q2 and will also stay at a high level of 4.3% YoY in Q4, more than twice the common 2.0% benchmark.

- U.S. and euro area yield curves shifted upwards significantly (10Y rates +89 bp compared to Q4 2021) while the U.S. curve has also inverted. The U.S. Fed and even the ECB are now clearly focused to tackle inflation dynamics. The Fed raised their target rates by 0.25% in Q1 while the ECB will accelerate the winding down of its asset purchase program which leaves the possibility of rate hikes later in the year.

- The different speed in monetary tightening is also reflected in the EUR/USD rate. In Q1 2022, the EUR lost -3.0% again the USD and fell below 1.10, the lowest value in almost 2 years.

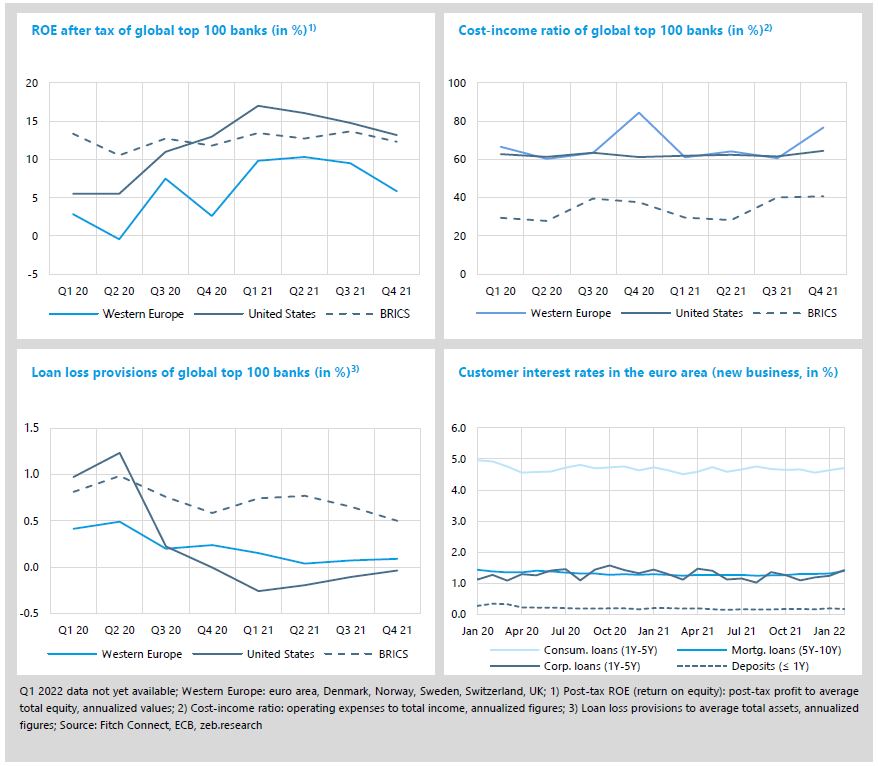

The largest global banks have reported solid fourth quarter results. Although trading business normalized in the fourth quarter, the core banking business remained strong and the banking sector completed an overall successful year. U.S. banks’ average profitability reached strong 13.2% and Western European banks 5.8% in Q4 2021. An increasing yield environment could bring further tailwinds for banks’ 2022 results, although the current Russia-Ukraine war and the corresponding economic turmoil weaken those expectations (see our special topic for details).

- In Q4 2021, Western European banks were not able to hold the strong average profitability of around 10% of previous quarters. However, with 5.8%, the average RoE is far above previous year’s level (+3.2%p YoY). U.S. and BRICS banks’ average RoE reduced only slightly year-over-year and remained again far above the level of their European competitors.

- European banks’ cost-income ratios increased significantly by +25.4%p QoQ to 77% due to a higher cost base as some seasonal HR expenses or additional costs in line with ongoing restructuring plans were generally posted in the final quarter. European banks’ revenues remained flat QoQ but increased by +8.6% YoY while costs reduced by -1.3% YoY.

- As expected, Western European and U.S. banks’ loan loss provisions (LLPs) increased slightly but remained on a very low level. In Q4, Western European banks’ risk provisions increased by just +0.02%p QoQ to 0.09% on average. U.S. banks’ time of meaningful provision releases seems over as LLPs increased by further +0.07%p QoQ to -0.04%.

- First euro area yield curve effects are becoming reflected in the customer rates. Mortgage loan rates continued to rise and reached 1.4% at the end of February (+16bp since October 2021), but also corporate and consumer loan rates improved in the first two months of 2022.

Special topic

Post-war economic perspectives and impact on banks

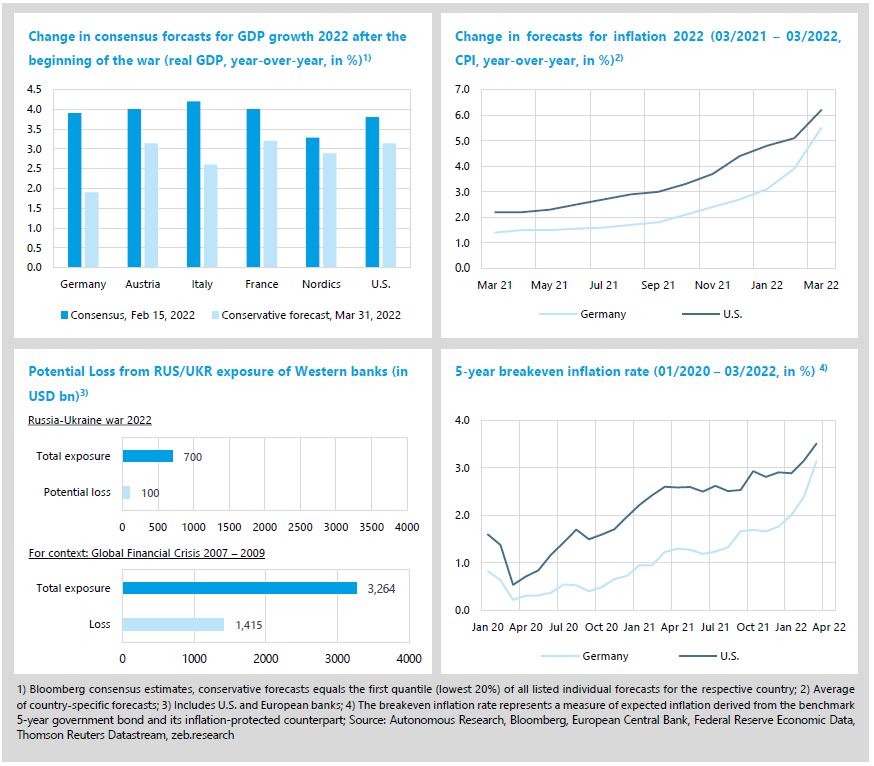

- What do the war and sanctions mean for economic growth, inflation as well as interest rates and thus for the European banking industry?

- The overall effects for the European banking sector seem to be manageable but banks can become the profiteers of the turning point for interest rates.

With the beginning of the Russia-Ukraine war at the end of February, the positive expectations for economic development at the beginning of the year were bitterly disappointed. Even if the outlook is very unclear, a hopeful Goldilocks scenario of strong economic growth and rising interest rates seems to have receded into the far distance. But what macroeconomic developments can we expect now? And what does this mean for banks’ market capitalization and P&L? In this chapter, we want to shed light on the consequences of the war and sanctions on growth, inflation as well as interest rates and thus on the European banking industry.

Western countries have responded to Russia’s invasion of Ukraine with coordinated and extensive economic and financial sanctions. Several measures were adopted especially in the areas of finance, energy, technology, transport and economy. For instance, in addition to the exclusion of Russian banks from the SWIFT system, the ban on transactions by the Russian Central Bank and far-reaching restrictions on access to foreign exchange reserves in the EU, export bans are imposed and EU airspace is closed to all Russian aircrafts. However, the economic consequences are not limited to Russia, but have also led in Western countries to energy, commodity and supply chain bottlenecks, significantly affecting trade volumes and accelerating the inflation process.

The resulting economic turmoil will very likely lead to, at least, a temporary slowdown in global growth. According to current consensus forecasts, economic growth will be tempered this year and next. European countries, and Germany in particular, will be hit hardest. However, losses in GDP development have so far been limited, and on a yearly basis an economic downturn remains manageable even with conservative forecasts. For instance, mid of February 2022, German GDP growth for the full year 2022 was expected to reach 3.9% YoY. As a result of the war, the forecast has been revised downwards and in a conservative scenario, German GDP growth is expected to reduce by -2.0%p but remain positive at 1.9%< (as of March 31, 2022). By comparison, the conservative estimates for the U.S. growth 2022 is still 3.1% YoY (-0.7%p vs. consensus).

Accordingly, a recession is not to be expected for the time being, but from 2024 the probability of stagflation increases remarkably. Unfortunately, further economic slumps cannot be ruled out in the event of a crisis escalating, for example in the money and capital markets or in energy supply. Moreover, the Russia-Ukraine war highlighted the economic vulnerability through dependence and ushers new strategic geopolitics. Besides the near-term impacts, the current conflict could accelerate a decoupling and a reduction in economic dependence on the Russian-Chinese bloc and poses new economic challenges for the Western economies.

Inflation, however, will speed up. While inflation forecasts have already been adjusted continuously by analysts since mid-September 2021, they have jumped again since the beginning of the war – and even the ECB also had to revise its forecast significantly upward. After inflation consensus forecasts for the full year 2022 was raised from 1.8% YoY end of Q3 21 to 2.7% YoY end of Q4 21, the forecasts were once again corrected upwards to 5.5% YoY end of Q1 22. And a further increase is quite possible, as the war is still driving second-round effects. Furthermore, a look into the future by no means promises an end to overall higher inflation rates. The fall of 2021 already marked the beginning of a new inflation regime as the “three Ds” (deglobalization, decarbonization, demographics) will be fueling inflation in the medium and long term.[1]

What direct and indirect effects can be expected on the banking sector? First of all, similar to other industry sectors, banks’ exposure to Ukraine and Russia implies possible direct losses. European banks with a high RUS/UKR exposure have already been punished by the capital market, like Unicredit, Société Générale or Raiffeisen Bank International (see chapter 1). Although, individual European banks can be hit hard and suffer significant P&L impacts, these effects appear to be bearable for the banking industry as a whole – even in a “walking away” scenario. Based on a high-level sense check of Autonomous Research, the potential trouble exposure of Western banks (i.e. direct Russian exposures and commodity-linked assets) amounts to USD ~700 bn, which could lead to a possible loss of just USD ~100 bn as more than 80% of the exposure comes from less risky commodity derivatives and lines to large commodity traders.[2]

The looming economic downturn will also have a further impact on banks’ overall business. Besides a decreasing loan demand, banks will again have to deal with higher loan loss provisions, as individual sectors (especially energy-intensive ones) have been heavily burdened by the sanctions and leaping energy prices. However, loan loss provisions are currently at a very low level and there should be still reserves on the balance sheets from the COVID-19 crisis, thus this challenge is not expected to be too significant.

Finally, despite a persistent inflation, the subdued economic growth perspective along with and still high and increasing debt levels of countries may lead to a delayed turnaround in interest rates. A look at the development of capital market interest rates gives still cause for hope though. Inflation expectations have increased continuously since September 2020 and rose sharply again towards the end of the first quarter 2022. By the end of March, the fundamental indicator of long-term inflation expectation (i.e. 5-year breakeven inflation rate) in the U.S. as well as Germany reached values above 3.0%. As the current development of capital market rates already shows (see Chapter 2), the rising inflation expectations strengthen the trend of a higher yield environment even in the current crisis period. The banking sector will be able to profit from this interest rate turnaround. For European banks, a 100 bp parallel interest rate hike means an average profit increase of over 20%. Nevertheless, there are also signs of a flattening of the yield curves. Especially in the U.S., the curve is already slightly inverted, which analysts regard as a strong indicator of a possible recession scenario.

Overall, the turning point for interest rates seems to be reached and the war is not going to stop it. Banks can become the profiteers of this development. Although, there is still a high degree of uncertainty, the economy is expected to remain robust for the time being. Provided there will be no severe recession, except for individual institutions, the war effects for European banks will remain relatively modest but an improving yield environment could bring tailwinds for tackling the remaining challenges of the sector.