Market developments and challenges in the global asset management industry

Our Asset Management Study, based on key figures of 40 asset managers with a significant footprint in the European market, shows that the European asset management industry is in a phase of profound transformation, driven by regulatory innovations, especially regarding sustainability, technological advance, and changes in the investment behaviour of private clients and institutional investors. These developments are putting traditional business models under increasing pressure and are being exacerbated by shrinking margins and persistently strong competition. The industry is therefore forced to adapt and realign.

After the marked slump in the markets caused by the Covid-19 pandemic and geopolitical tensions, assets under management recovered noticeably. Nevertheless, the situation remains fraught: the consequences of the war in Ukraine are still being felt, the Gaza conflict is creating additional uncertainty, and persistently high inflation is weighing on economic stability. The rise in interest rates in recent years restored the attractiveness of bonds and money market products, while stocks only started to record inflows towards the end of the year. Stagnating or falling interest rates in 2024 are contributing to a continuation of this trend.

In this challenging environment, investor preferences are increasingly shifting towards lower-cost, passively managed strategies, which will put further pressure on the revenue margins of asset managers in the long term. ETF assets have increased considerably over the past few years. Driven by the strong performance of the products, ETFs saw increased net inflows at the end of the year resulting in a global growth of 22% in 2023. Sustainable investments are slowly recovering after a weak 2022, although at less than 10%, their share of total assets remains comparatively low and is heavily concentrated in the European market. Alternative investments, such as infrastructure and private equity/debt, on the other hand, are still on the upswing and achieved significant inflows.

In terms of global market share, the United States still holds half of the world’s assets under management, but the APAC region is becoming increasingly important.

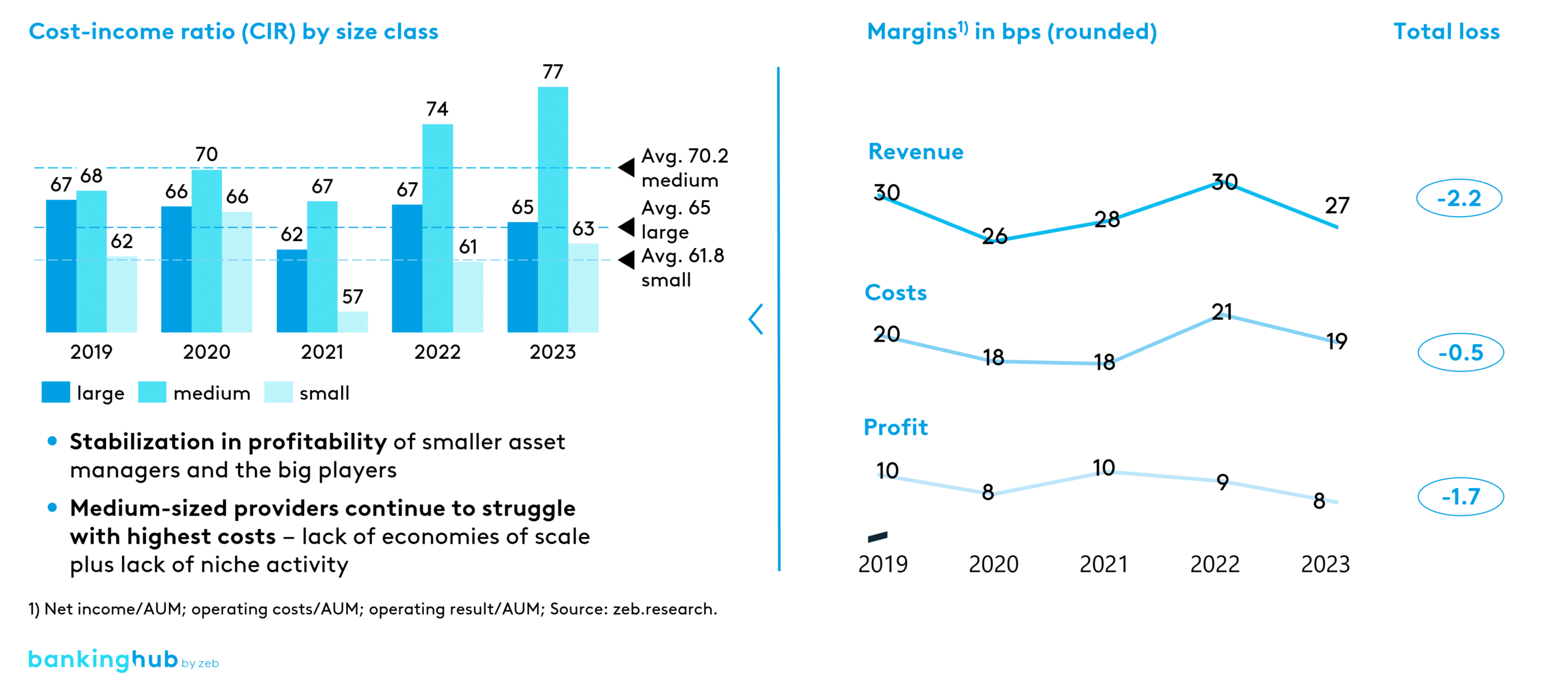

Despite stable revenues and the solid performance of selected asset classes, many market participants have been struggling for several years with rising costs that continue to outstrip income growth. There is a predominantly even development in the various AM categories, but small medium size providers tend to have a less favorable cost-income ratio in 2023 compared to their relatively stable position in 2019. Contrary to the trends of recent years, the current data shows that medium size asset managers in particular saw a considerable increase in their cost-income ratio (CIR) in 2023 despite a (2%) reduction in their costs often achieved through stringent outsourcing. While large providers have been able to keep their CIR largely stable, medium-sized providers continue to struggle with high costs due to a lack of economies of scale and a missing focus in their business models. Profits are declining across the industry, which indicates that pressure is growing due to untapped cost-reduction potential and the tendency to sell low-margin products (see Figure 1).

Our study reveals that the dominance of individual large asset managers observed in recent years is continuing. The winner-takes-all effect is still clear to see: 65% of net new money (NNM) was generated by just five global players, which poses increasing challenges for smaller asset managers and requires proactive measures. Especially the observable consolidation of the industry is contributing to the increased dominance of large asset managers.

Forecasts for the European asset management industry: 5-year simulation

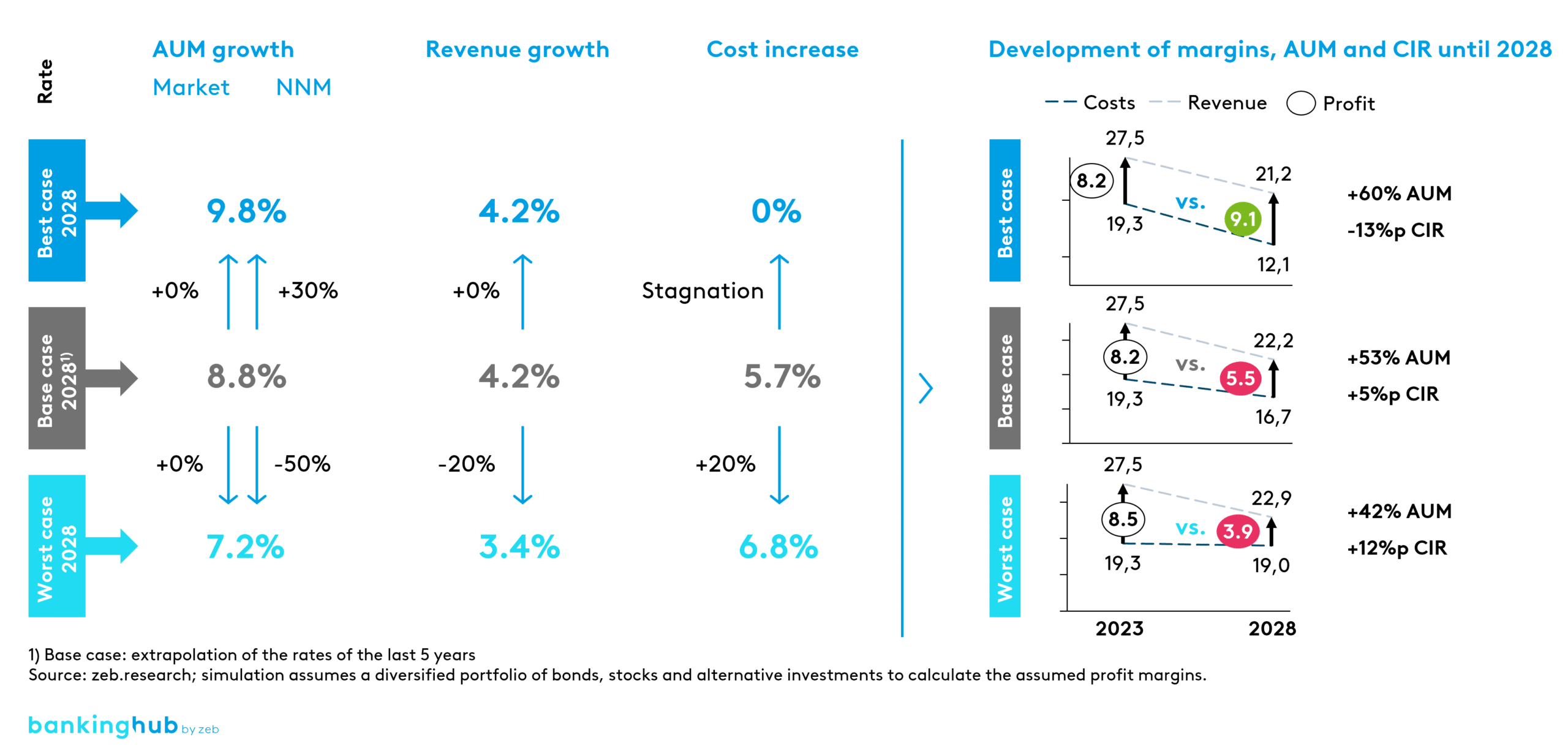

To assess the development of the European asset management industry, we simulated three scenarios and their impact on the key figures of 40 asset managers with a significant footprint in the European market (base-case, worst-case and best-case scenario) up to 2028. The results of the 5-year simulation can be seen in Figure 2.

Despite short-term volatility due to geopolitical uncertainties, the base scenario is considered the most likely over the five-year period. Rising costs for implementing regulatory requirements, investing in digitalization and artificial intelligence, as well as building up expertise and acquiring qualified staff will result in a further deterioration of the profit margin in the short to medium term.

Within this base scenario, the developments predicted vary for the different size classes of providers:

- Small providers will have to contend with sustained cost pressure in the long term, which will further reduce the profit margin to 12.2% by 2028, despite a satisfactory margin of 17.4% in 2023. The simulation shows that earnings power will remain, but will come under strong pressure compared to costs, leading to a decline in profitability.

- Medium-sized providers are particularly vulnerable as they suffer from insufficient economies of scale and low margins. Their profit margin will shrink from 6.9% in 2023 to 4.1% in 2028. In the active management segment, they are facing challenges due to the ongoing decline in fees, which, together with low net inflows, is having a considerable impact on profitability.

- Large providers benefit from their high economies of scale. Their profit margin is solid at 7.8% in 2023 and will decrease only slightly to 6.3% by 2028. Their greater technology affinity and capital strength enable them to remain competitive even in a difficult market environment.

Survey results and recommendations for competitive positioning

The simulation makes it clear that the strategic orientation of many companies is in question and that an adjustment or realignment ought to be considered. Asset managers need to identify the right levers to position their business and operating models for the future.

Based on a survey of industry experts and our extensive project experience, we have identified four key fields of action in our European Asset Management Study 2024.

A) Digitalization including the use of artificial intelligence

Our survey of European asset managers, also part of our study, revealed that 90% of respondents (multiple answers were possible) see digitalization, including the use of artificial intelligence, as the top agenda item for the coming years. However, many organizations lack a comprehensive understanding of the relevant technologies, which is why it is essential to build up know-how as a fundamental prerequisite and knowledge management as a preliminary step.

This lack regarding the status of digitalization of expertise is confirmed by the responses of the asset managers taking part in the survey: over 60% of respondents state that their employer’s level of digitalization could be improved. Important recommendations to boost the level of digitalization include consolidating data pools and increasing data quality, implementing innovative technologies, stabilizing and updating existing systems, and standardizing production processes.

The optimization potential that can be realized through digitalization varies depending on the technology used. From the digitalization of processes and automation to the use of machine learning and generative AI, each technology offers specific advantages, but also requires particular conditions and has its own limitations. Despite the currently strong focus on AI, it is not a one-size-fits-all solution and should be evaluated accordingly.

Success factors for increasing digitalization include a sound management understanding of the opportunities and risks, a fundamental willingness to rethink existing data logics and system landscapes, and a tidy data architecture.

B) Enforcement of cost savings

The second most common field of action on the agenda for 57% of respondents is the enforcement of cost savings. Short and long-term cost savings are necessary for many asset managers due to the persistently high and rising cost base. Depending on the ambition and urgency costs can be reduced in the short term (tactical) or long term (structural).

As already mentioned in field of action A), digitalization is a key component in leveraging long-term cost-reduction potential. However, the effectiveness of such measures is long-term in nature, as the implementation of new technologies and the digitalization of processes go hand in hand with considerable investments and therefore lead to a short-term rise in costs. Short-term savings such as reducing project budgets, staff reductions and cutting marketing and operating expenses can provide temporary relief, but often have only a limited, sometimes counterproductive effect.

Success factors in carrying out cost programs include ensuring a high level of transparency and the implementation of cost controls, targeted investments in technology and processes as well as continuous monitoring and adjustment of cost structures. A holistic approach that includes both short-term and long-term measures can lead to a sustainable reduction in the overall cost base of up to 20%.

C) Expanding the range of alternative asset classes

48% of respondents see the expansion of alternative asset classes as an important field of action for the coming years, as these will continue to gain in importance despite the changed interest rate environment and offer clients better risk diversification in volatile times. The continuing demand for alternative investments enables asset managers to diversify their offering and increase profit margins.

There are a number of success factors for launching alternative equity or debt products (including infrastructure, renewable energy private markets, venture capital). These include such as the choice between internal development and cooperation, and the targeted development of resources and the efficient scaling of processes which requires skilled staff and robust IT systems.

In addition, innovative vehicles such as ELTIF 2.0 can contribute to opening up new target client groups and facilitating access to promising asset classes. By tapping into new markets and building expertise in alternative assets, asset managers can reinforce their competitive position in a highly competitive market and attract new client groups.

D) Addressing new private client groups

The significant growth in the EU retail segment shows the rising interest of young, digitally savvy clients in savings and investment products. To remain competitive, asset managers need to combine traditional sales channels with digital solutions. Establishing a future-proof sales channel requires a flexible and cost-efficient strategy supported by accurate data analysis and high IT security standards.

Besides acquiring providers with comprehensive solutions or partnering to cover specific target groups, building a new target group-specific offering in asset management can be an effective strategy. The different financial needs and preferences of private clients must be reflected in the sales channel. Targeted data analysis can be used to create a seamless, client-centric experience that meets the highest IT security standards and can be flexibly supplemented with additional services.

The large number of fields of action identified shows that there are opportunities to save costs and boost competitiveness. It is essential to consistently transfer these strategies into the implementation phase, ideally from a position of strength at an early stage.

The European asset management industry is facing significant challenges. At the same time, however, there are also numerous opportunities for repositioning, efficiency gains and growth. The ability to adapt flexibly to changing market conditions and client requirements will be crucial in order to survive in an increasingly complex and competitive environment.

We would be happy to support you in this endeavor.