Earnings potential for Austrians banks

Positioning themselves as strategic partners for retail and corporate customers, developing sustainable financial products and adapting risk management are key approaches to achieving long-term success. The sustainable transformation of the Austrian economy results in an annual investment volume of around EUR 35 billion. These structural changes open up considerable earnings potential for banks in external financing.

Specifically, Austrian banks can expect additional annual income of around EUR 0.7 billion in corporate banking. In retail banking, loans for the renovation, refurbishment and modernization of property above all create additional potential of around EUR 0.1 billion per year in the Austrian market, and the trend is rising. Furthermore, the additional potential in traditional SME business is estimated at around EUR 0.3 billion per year.

How much do European banks need to do in terms of ESG? Download our ESG Implementation Study!

ESG Implementation Study 2024

Europe’s banks under the microscope: between ecological ambition and economic realityzeb’s recent ESG Implementation Study shows that there is still a great need for action among banks in the entire DACH region when it comes to ESG and that the gap in Austrian financial institutions identified by the FMA has not been closed since the analysis was published in January 2023.

Regulatory requirements for Austrian regional banks

While the ECB and national supervisory authorities such as BaFin in Germany already impose binding, specific requirements on both large and regional banks, the proposed approach to sustainability and to the corresponding risks for Austrian financial institutions has so far remained non-binding. The FMA guide for managing sustainability risks[2] which was published in 2020 provides an overview of definitions, requirements and precautions but does not constitute a regulation. However, the current non-binding nature should also become a thing of the past for Austrian banks when the new EBA Guidelines on the management of ESG risks are published, which is expected in the fourth quarter of 2024.

The consultation draft of the guidelines published in January 2024 already shows how specific the requirements for Austrian financial institutions and their risk management will be: ESG risks must be assessed regularly and comprehensively, a sound ESG data basis must be established, and suitable assessment methods must be applied. These risks are to be integrated into the usual processes such as risk appetite, internal control system, ICAAP, and risk reporting to ensure that ESG aspects are effectively taken into account in all areas of risk management.

Carbon accounting and required reporting

Austria aims to be climate-neutral by 2040 at the latest. Corresponding measures are implemented based on an amended Climate Protection Act with binding reduction paths until 2040 and interim targets until 2030 as well as clear responsibilities and schedules.[3] Financial institutions therefore need to define their own paths and manage not just CO2 emissions generated in operations but also their loan portfolios (Scope 3 emissions). The Austrian Green Finance Alliance is an initiative of the Federal Ministry for Climate Action (BMK) which is already supporting financial companies in making their business models climate-friendly. The alliance includes banks, insurance companies, pension funds and other financial institutions that have committed to aligning their financial flows with the goals of the Paris Climate Agreement. However, most Austrian banks have not (yet) committed themselves to this.

It is not only the expectations of their stakeholders that are increasingly forcing financial institutions to face up to precisely this CO2 management and any action plans. The draft EBA Guidelines on the management of ESG risks also focus on the transition to a decarbonized economy and environment. Institutions must clearly demonstrate how they intend to achieve their defined objectives and how aware they are of their exposure to ESG risks.

In addition to the future binding requirements for risk management, the Corporate Sustainability Reporting Directive (CSRD) stipulates carbon accounting for financial institutions. The CSRD follows the European Sustainability Reporting Standards (ESRS), whereby ESRS E1 (“Climate Change”) requires companies to record and report their direct and indirect greenhouse gas emissions, including emissions caused by their financed activities.

The reporting obligation initially applies to companies that were previously within the scope of the Non-Financial Reporting Directive (NFRD). Initial reporting will be required in 2025 for the 2024 financial year. However, from 2026 (for the 2025 financial year), the CSRD will also be extended to “large companies” / credit institutions that meet two of the following three criteria:

- Net turnover of at least EUR 50 million

- Total assets of at least EUR 25 million

- At least 250 employees on average during the financial year

Small and non-complex credit institutions (SNCIs) and captive insurance companies will also have to disclose as of the 2026 reporting year. Non-compliance with the CSRD may result in sanctions.

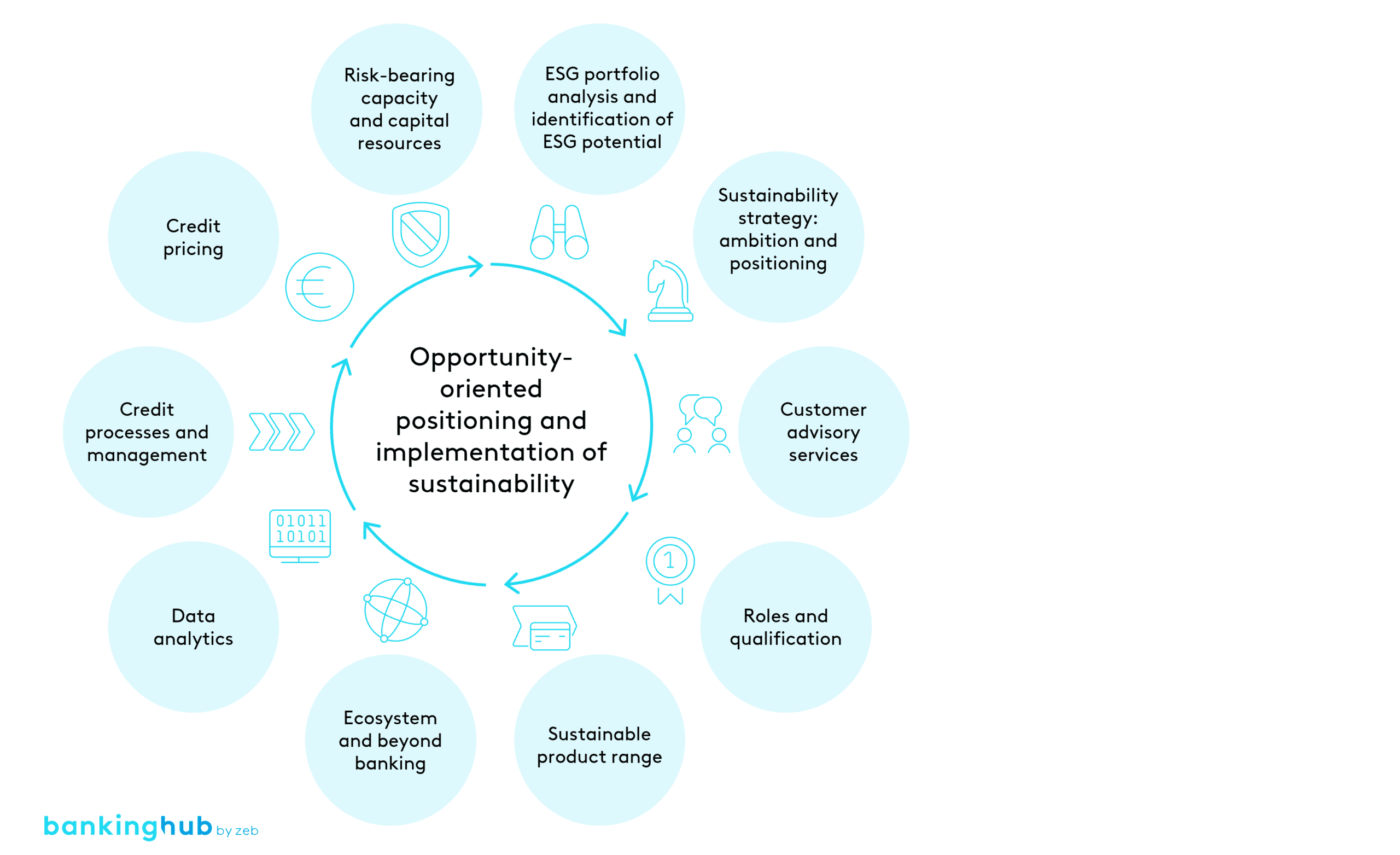

Potential of ESG in retail and corporate banking

The sustainable transformation of the economy opens up considerable earnings potential for banks, especially in retail and corporate banking. Sustainability criteria should be integrated into the business model in an opportunity-oriented manner. Regional banks can develop innovative financial solutions that also have a positive impact on society and the environment. This requires close cooperation with customers to understand their needs and sustainability goals and to offer appropriate products and services. ESG could also become a decisive factor in employer attractiveness, driven in particular by the change in social principles. Talents and skilled workers may increasingly prefer companies that take environmental and social responsibility seriously. This could help banks to position themselves as attractive employers.

ESG-oriented strategies offer considerable growth opportunities in both corporate and retail business. In corporate banking, the focus is on strategic advice and supporting companies in their sustainable transformation. By providing sales staff with targeted training, banks can ensure that ESG issues are competently integrated into customer meetings. This not only enables banks to fulfill regulatory requirements, but also to build strong, lasting customer relationships. A modular approach to advisory services and the use of suitable sales media and tools form the basis for achieving quick wins and exploiting the potential of sustainability as a genuine sales topic.

The retail banking market offers enormous market potential for banks, particularly in the area of energy efficiency upgrades of residential buildings. With the increasing demand for green financial products and government support for energy efficiency measures, banks have the opportunity to expand their product range correspondingly and position themselves as key partners in the sustainable transformation of the real estate sector.

Furthermore, banks can move beyond traditional banking and integrate so-called beyond-banking approaches by creating comprehensive ecosystems. In this context, they could not only provide financing offers, but also help to find energy advisors, manufacturers of heat pumps or providers of photovoltaic systems. By involving such partners, banks offer their customers a holistic service in the areas of refurbishment, modernization and renovation. Doing so not only strengthens customer loyalty but can also open up new sources of income. At the same time, banks position themselves as an integral part of a comprehensive network that effectively supports and promotes the sustainable transformation of real estate.

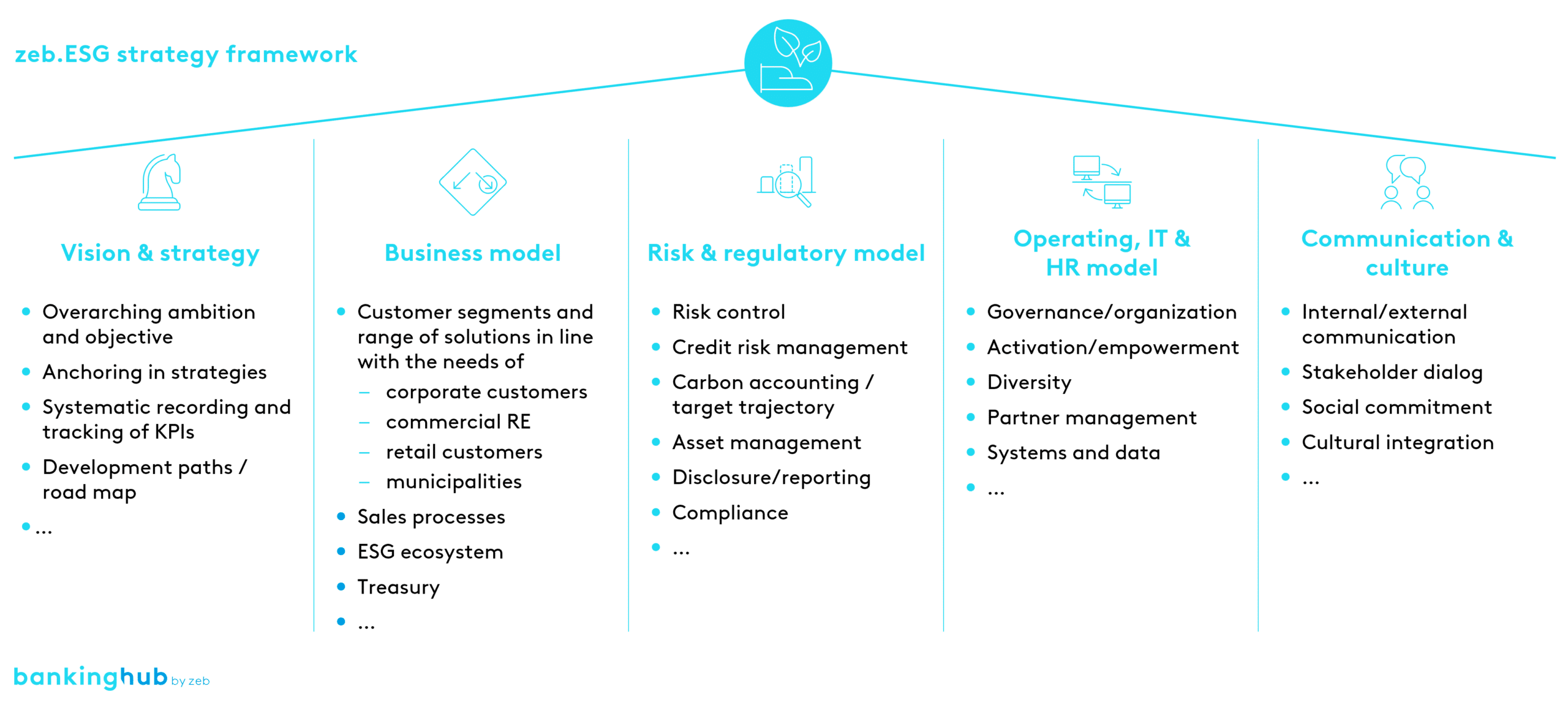

Strategic approach to ESG: a road map towards sustainability

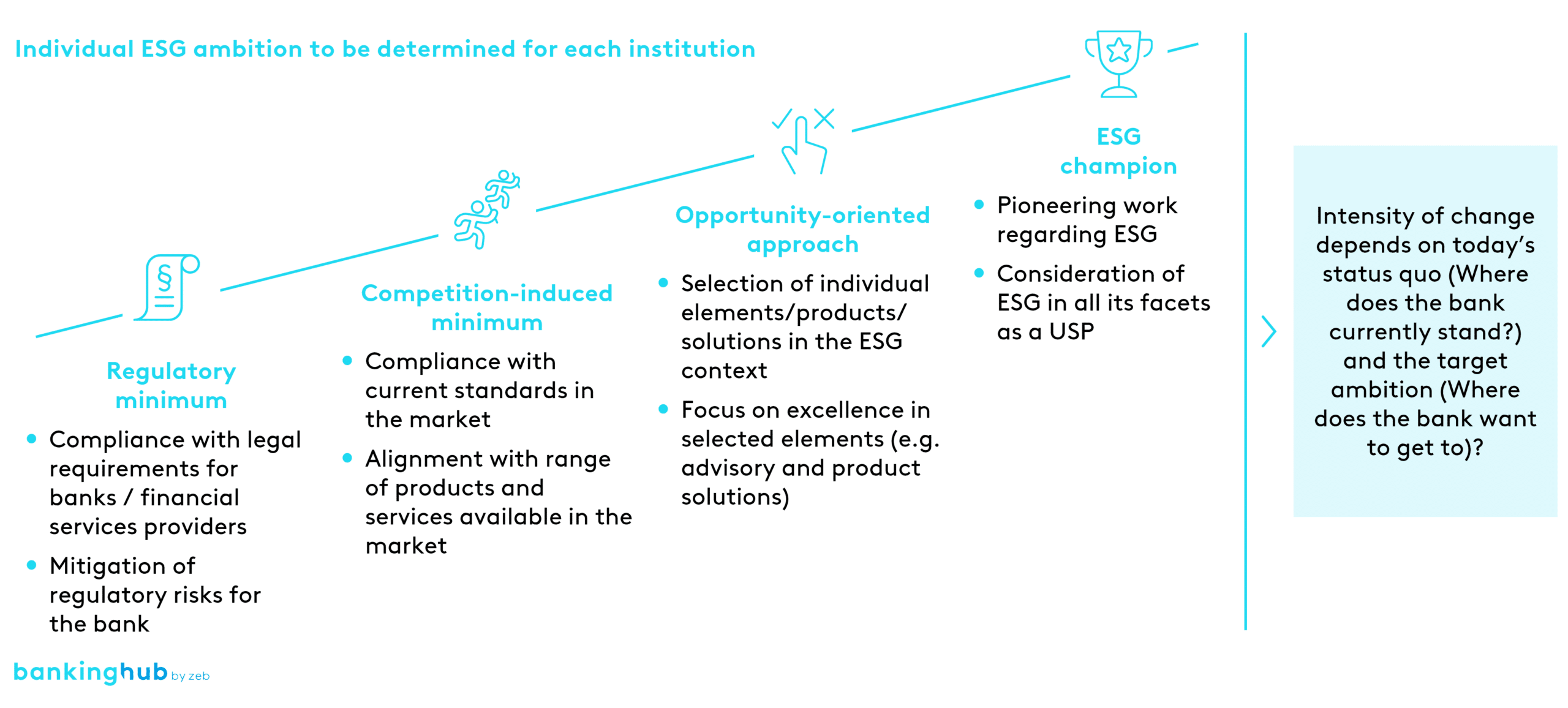

The integration of sustainability into the business strategy is becoming increasingly indispensable for Austrian regional banks, primarily due to the tightening requirements of the regulators. To meet these requirements, a structured approach is essential. First of all, the ESG targets must be defined individually for each financial institution, depending on the level of ambition chosen. A comprehensive inventory of current ESG practices is then carried out to clearly identify the company’s strengths and weaknesses. Based on this, the discrepancy between the current situation and the defined ESG targets is determined. This analysis forms the basis for developing an ESG road map, which serves as a strategic guide. The road map defines which measures are prioritized, how resources are used efficiently and what steps are necessary to achieve the required sustainability goals.

By precisely formulating their ESG ambitions for all business areas, Austria’s regional banks can not only clearly define their goals at company level, but also consistently implement them in each specific area. This strategic focus enables banks to ideally adapt to regulatory requirements and at the same time create long-term value for customers and stakeholders. In doing so, they not only ensure their positioning as highly responsive market players, but also their role as innovative and forward-looking partners that are actively working towards a successful and sustainable future.