Regulatory requirements imposed by MaRisk

The MaRisk delineate specific stipulations for the treatment of non-performing loans or problem loans, thus providing a key framework for NPL management. Lead responsibility for problem loan management processes and their monitoring must be assumed outside the front office.

The terms NPL (non-performing loans) and NPE (non-performing exposures) are often used interchangeably, but there are significant differences between the two. The term NPL refers exclusively to loans and advances, whereas NPE encompasses all types of non-performing exposures, such as debt securities, for example. Consequently, the scope of NPEs is considerably more expansive than that of NPLs. In MaRisk, the so-called NPL ratio is used to ascertain whether a financial institution must be classified as a high-NPL bank. However, in the context of the reduction targets, possible measures and strategy, reference is made to NPE.

Significance of the NPL ratio

The NPL ratio is a key indicator of an institution’s financial stability and provides insight into the quality of its loan portfolio. The ratio is calculated by dividing the gross book value of non-performing loans by the gross book value of the total loans. Financial institutions are required to monitor the NPL ratio on a regular basis.

In Germany, institutions with an NPL ratio of 5% or more are subject to specific regulatory requirements set out in MaRisk. If this threshold is exceeded on two consecutive reporting dates, the financial institution in question is classified as a ‘high-NPL institution’. These institutions must develop a strategy to reduce such exposures. The objective is to achieve a predetermined level of non-performing exposures within a realistic but ambitious time frame, provided that this is not already consistent with the original business model.

The key steps in developing and implementing this strategy are as follows:

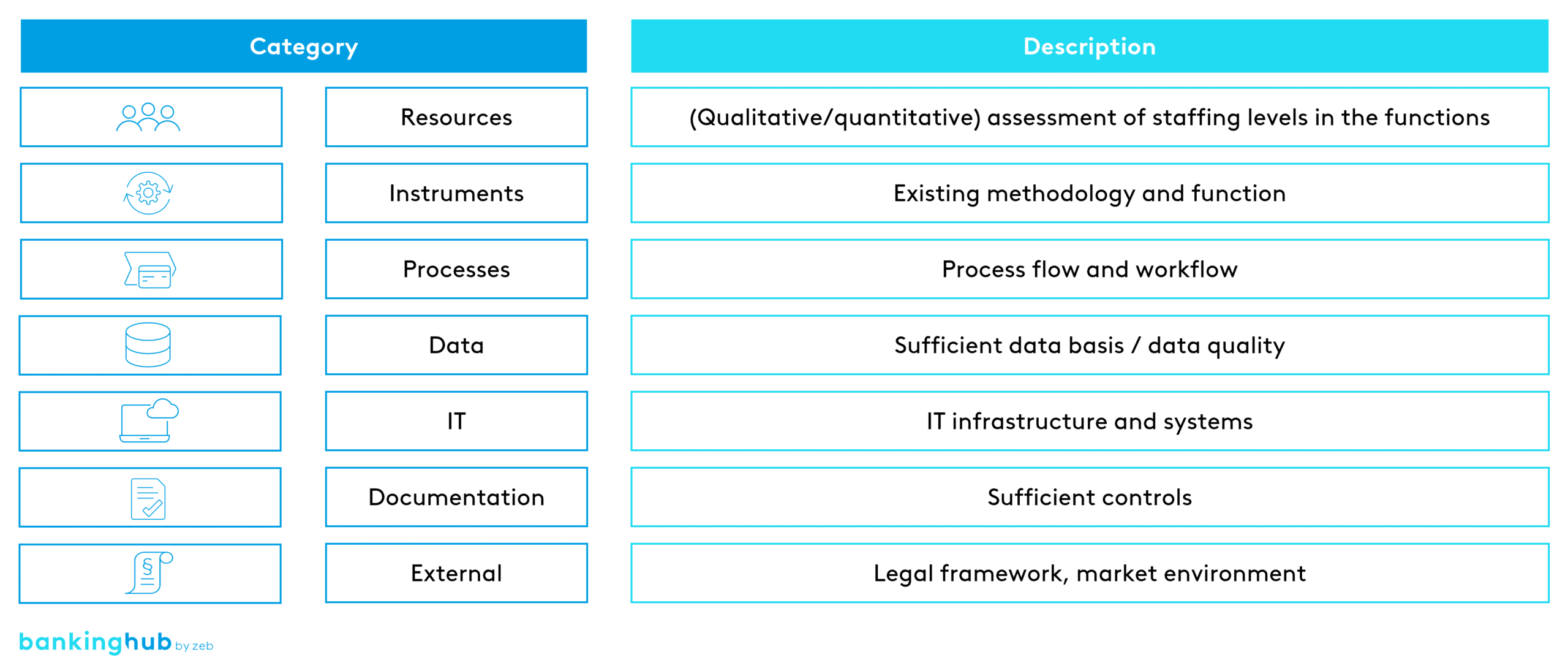

A) Analysis of the business environment and external conditions

- Self-assessment: annual assessment of the current situation, causes of non-performing loans, measures taken to date and operational capacities

- External factors: analysis of the market environment, demand for NPEs, availability of specialized service providers and the regulatory and legal framework

- Capital planning: consideration of the impact of the NPE strategy on capital and integration of suitable measures into capital planning

B) Development of a comprehensive strategy

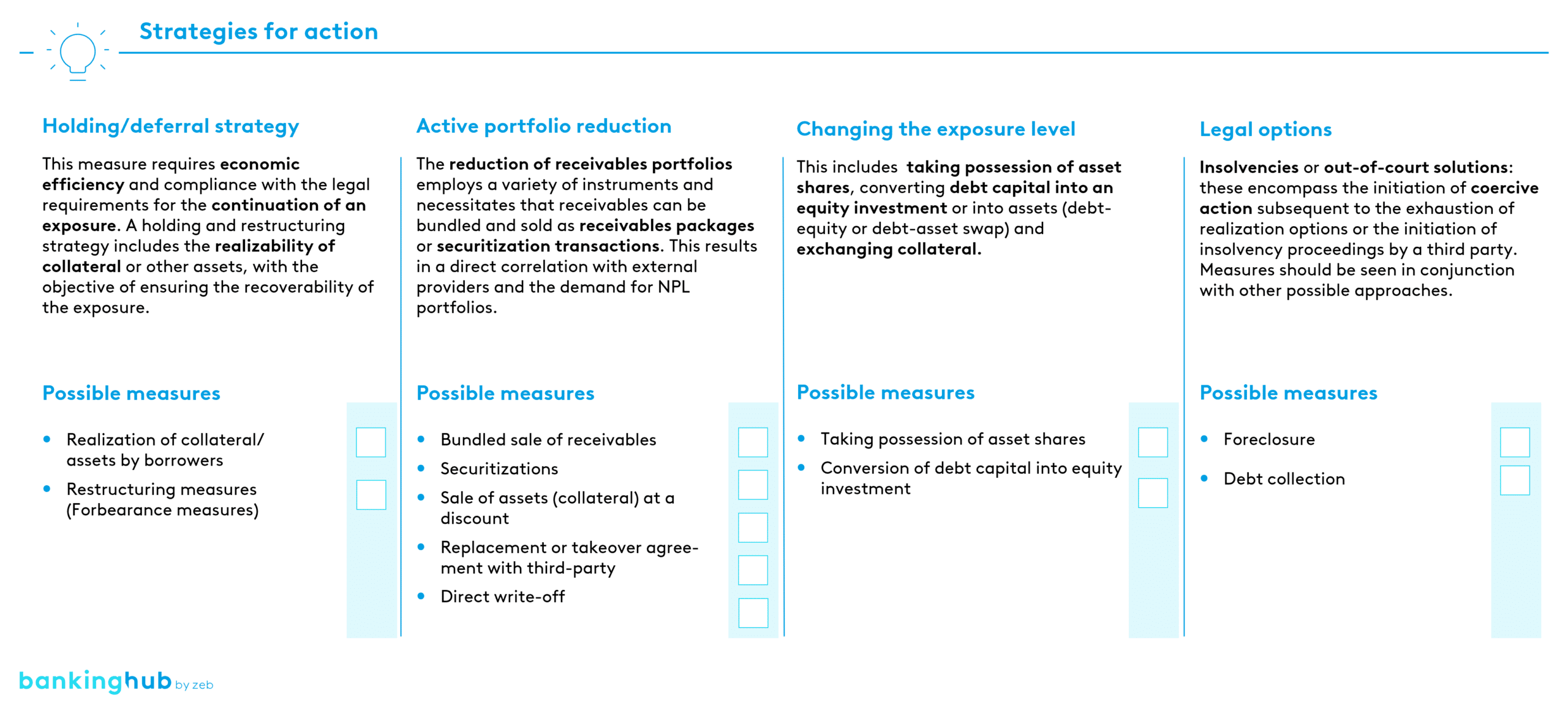

- Strategic options: combination of different approaches such as holding strategies, forbearance options, active portfolio reduction, changes to exposures, bail-out acquisitions and legal measures

- Targets: definition of quantitative NPE targets for short, medium and long-term periods and for main portfolios

C) Implementation and monitoring

- Implementation plan: detailed planning of the operational implementation over a period of 1 to 3 years

- Monitoring: quarterly review of progress based on KPIs, reporting significant deviations to management and taking corrective action

These steps are essential to the development and successful implementation of an effective strategy for reducing non-performing exposures.

Bail-out acquisitions

Bail-out acquisitions are one way to reduce non-performing loans. In such cases, financial institutions purchase the collateral or assets that are securing the loan in question. This allows them to mitigate the losses that would otherwise result from a forced sale at this moment, for instance, by first acquiring the assets themselves and subsequently selling them at a more favorable point in time or holding them permanently as part of their own portfolio.

In light of the current trends on the real estate market, this option may be a prudent course of action for some financial institutions right now. Bail-out acquisitions can have a positive effect on both the balance sheet and the income statement due to the reduction of NPL loans. In addition, financial institutions retain control over the realization process, which allows for more efficient resolution.

However, bail-out acquisitions necessitate sufficient capital and can pose operational challenges in their management, as well as market risks. If a financial institution contemplates carrying out bail-out acquisitions, it must develop a guideline for doing so. High NPL institutions must also comply with additional requirements for the risk control function.

Importance of early risk detection

Effective early risk detection is essential to identify borrowers who may be at a higher risk of default and to recognize potential problem loans in good time. By employing both automated and manual procedures, credit institutions can detect specific irregularities in the credit data that indicate an increased risk of default. This enables the bank to provide timely and comprehensive support to flagged borrowers, thereby avoiding potential defaults.

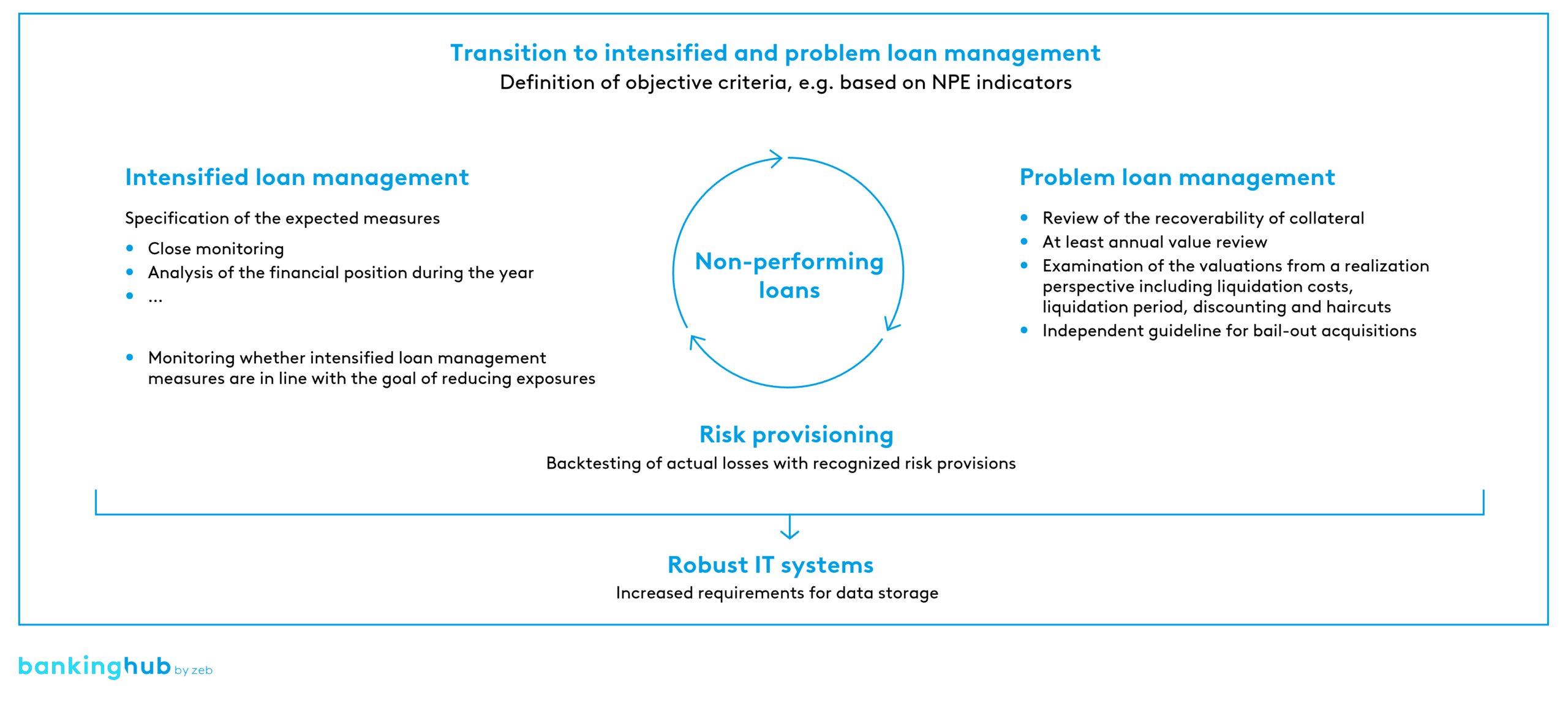

Support for both intensified and problem loan management

Intensified and problem loan management necessitates the application of specialized knowledge and the mobilization of specialized resources. Credit institutions must ensure that they have qualified staff capable of managing complex loan cases. This encompasses both resolution and restructuring processes.

In this context, it is also of the utmost importance that employees are able to conduct crisis discussions and negotiations with borrowers and other parties involved, such as other creditors, insolvency administrators or auditors. This necessitates not only sound specialized knowledge, but also excellent communication and negotiation skills. Good preparation and a structured approach are just as important as empathy and assertiveness.

Furthermore, close collaboration with internal and external experts, coupled with continuous monitoring of the loan portfolios is essential for enabling prompt responses to evolving circumstances. It is also crucial to conduct regular reviews of the collateral securing exposures in problem loan management, ensuring that the underlying parameters are clearly documented in a readily understandable format. For workout loans, the carrying amounts must be determined from a liquidation perspective.

Forbearance

Forbearance refers to measures taken by credit institutions to accommodate borrowers who are unable to service their loans due to financial difficulties. These can include adjusting the terms of the loan, such as lowering the interest rate, extending the term, or temporarily suspending payments.

Effective forbearance measures can help to ensure that loans are not immediately classified as non-performing by giving borrowers time to improve their financial situation. However, these measures must be carefully monitored to ensure that they do not result in a delay in the default of the loan. There are significant regulatory and procedural hurdles.

Conclusion

Managing non-performing loans will assume a pivotal role for many banks in the coming years. Financial institutions can reduce their NPL ratios and thereby secure their financial stability through effective early risk identification procedures, the provision of specialized support in intensified and problem loan management, and the introduction of robust forbearance measures.

Bail-out acquisitions may also be a viable option for high-NPL institutions, which must fulfill specific requirements to meet the challenges of NPL management. The development of an effective strategy to reduce non-performing exposures is imperative and must be implemented consistently. At the same time, financial institutions must address the shortage of skilled staff and the lack of specialized knowledge in order to ensure long-term success.