Why is sustainability relevant in corporate banking?

The importance of sustainability in corporate banking has increased significantly. ESG (Environmental, Social, Governance) is no longer just a trend, but an integral part of the business strategy of many companies, including numerous banks.

Banks are faced with the challenge of positioning themselves in this dynamic environment and at the same time leveraging the opportunities associated with sustainable financing products. In this context, developing specific (ecologically and socially) sustainable lending products and an overarching financing framework that clearly defines them is a key lever.

Building the foundations: crafting a resilient financing framework for sustainable solutions

A sound financing framework forms the basis for banks to clearly structure their green lending products and ESG-oriented activities in that it ensures that the developed products are sustainable, transparent and comprehensible. Several key aspects need to be considered:

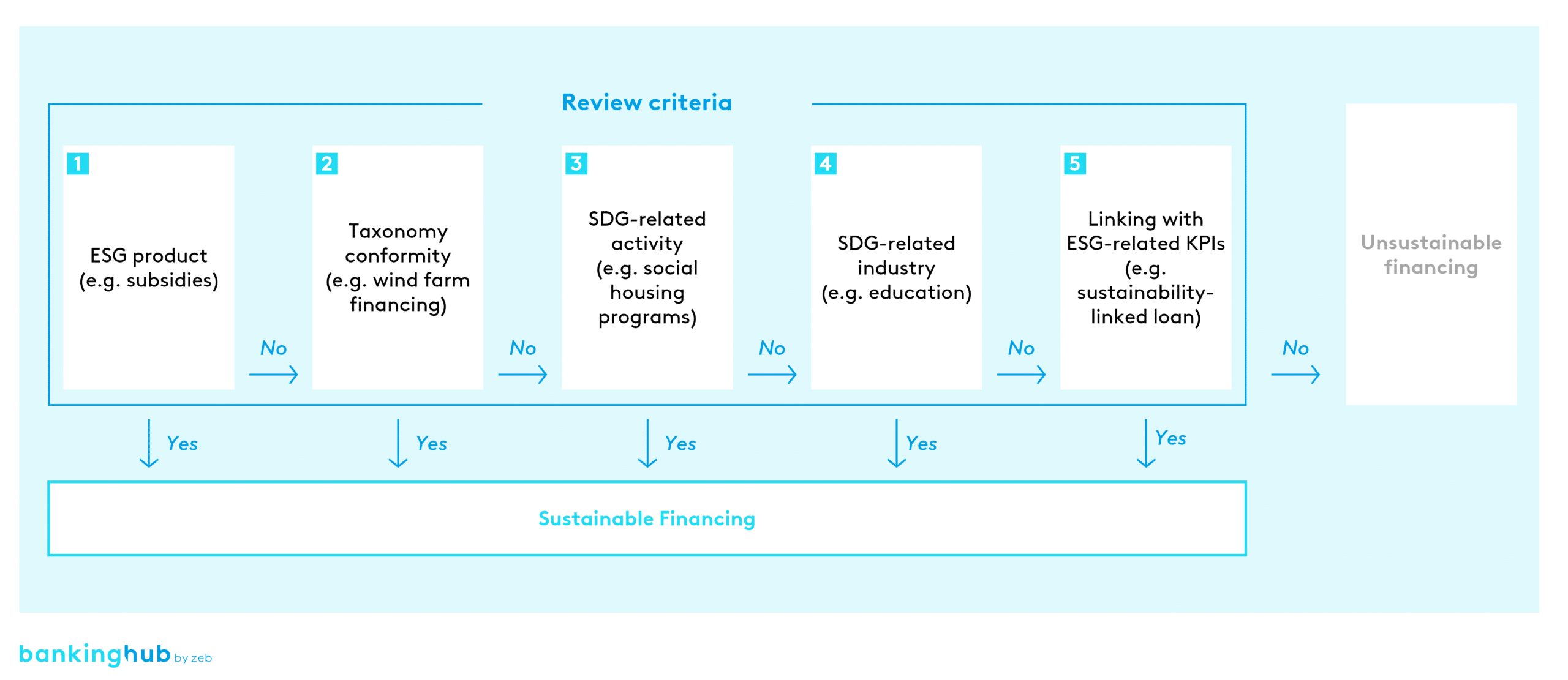

- Defining criteria: the framework must define clear, transparent criteria according to which projects are classified as “green”. These criteria should be based on international standards such as the Green Loan Principles, the Sustainability-Linked Loan Principles or the EU Taxonomy.

- Monitoring and review: compliance with the defined ESG criteria must be continuously monitored. With digital platforms and technologies, banks can optimize their monitoring processes and efficiently review the environmental and social impact of the projects they finance.

- Reporting: transparent reporting on the use of funds and the results achieved is essential for gaining the trust of investors and customers. Regular sustainability reports provide them with information on the ecological and social effects of the financed projects and strengthen the bank’s credibility.

In order to ensure that the criteria and processes developed in the framework are marketable and to refute any greenwashing accusations, transparent criteria and processes must be defined. First of all, the criteria for classifying financing as “green” or “sustainable” should be transparent and based on internationally recognized standards such as those of the Loan Market Association, the Green Loan Principles, and the Sustainability-Linked Loan Principles. This ensures that only financing of projects with real added value for the environment and/or society is promoted.

In addition, it is important for banks to strengthen their own credibility through external validation. Independent second-party opinions (SPOs), for example from rating agencies, can corroborate the marketability and robustness of a framework, thereby increasing the confidence of customers and investors. This creates an additional level of security and prevents false promises of sustainability.

In the long term, the framework should not remain static. Being sustainable is a dynamic process that requires continuous adaptation. Through regular reviews and transparent reporting on the progress made, banks can flexibly adapt their strategy and meet the constantly changing regulatory requirements. Transparent and honest communication with customers and stakeholders is crucial for gaining trust and avoiding accusations of greenwashing.

Green loans to convince: how to design sustainable financing solutions

Green lending products are an opportunity for banks to position themselves as innovative partners for their corporate clients. Two main product categories have shown particular promise:

Green/Social loans: these loans are earmarked for financing specific environmental projects such as renewable energies or sustainable water management, or social projects such as educational facilities. This type of financing is attractive for companies as it supports their ESG strategies and at the same time makes them eligible for institutional investors with a focus on sustainability.

Sustainability-linked loans: the terms of this type of loan are linked to the achievement of certain ESG targets. If the borrowers meet the previously defined sustainability criteria, their interest rates improve. This motivates companies to actively pursue their ESG goals and creates financial incentives for sustainable business practices.

Developing such customized products helps banks stand out against their competitors and tap into new client groups looking for sustainable financing options.

It is of key importance that the design of these products has a clear focus on the respective bank’s business model, customer structure and typical business. Many of today’s green or social credit solutions originate from corporate banking and require highly complex processes and data. Tailor-made solutions that are pragmatic where they need to be are essential for both German SMEs and the banking industry, which is dominated by banks with a regional focus.

Sustainability as a business opportunity: how green financing solutions ensure your success

Green lending products offer banks numerous advantages:

- Developing new customer segments: more and more enterprises, especially SMEs, are integrating sustainability into their business models.[1] Banks that offer these companies green lending products in a targeted manner can not only expand their customer base, but also strengthen their bond with existing customers.

- Securing competitive advantages: the market for green financing is growing steadily.[2] Banks that focus on sustainable products at an early stage position themselves as pioneers and benefit from growing interest in ESG-compliant financial solutions.

- Risk and return perspective: many sustainable projects offer more stable returns, as companies with an ESG focus are more resilient to economic fluctuations. This reduces the credit risk and at the same time improves the bank’s refinancing options, as ESG-oriented products attract institutional investors.[3]

ESG advice and green lending products: one step closer to a comprehensive solution

In recent years, an increasing number of banks have been adding ESG advisory services to their service portfolios. These services constitute the first step towards a comprehensive ESG strategy, but without suitable lending products, the offering remains incomplete. Customers who use sustainability-related advisory services also expect their bank to offer them appropriate options for green financing.

So it’s only logical for banks that offer ESG-related advisory services to also offer ESG-related lending products. Banks that offer both advisory and product solutions are more credible and can synergistically dovetail them. This results in deeper customer loyalty and a clear market positioning as a sustainable partner.

How much do European banks need to do in terms of ESG? Download our ESG Implementation Study!

ESG Implementation Study 2024

Europe’s banks under the microscope: between ecological ambition and economic realitySuccess factors for implementing green lending products

The successful implementation of green financing solutions requires a substantial examination of the relevant frameworks and standards, such as the EU Taxonomy, the Green Loan Principles and the Sustainability-Linked Loan Principles. After developing a sharpened understanding of the various types of green lending products, banks have to decide which sustainable financing solutions they would like to introduce themselves and how they want to structure them.

Another key success factor is the implementation and ongoing optimization of an efficient review process that enables the banks’ sales staff to quickly and easily assess green lending products in terms of their suitability for the banks’ portfolios. This process must be properly integrated into the respective bank’s existing IT infrastructure.

The targeted qualification of sales staff is of central importance for the successful establishment of green lending products in sales. Against this backdrop, bank employees should not only receive technical training on sustainability and green financing solutions, but also practical sales training that enables them to make potential-oriented decisions when it comes to green lending products.