How does the German bancassurance market compare with the European market?

Bancassurance is a globally growing business model where banks act as a sales channel for insurance products. The global market was estimated at USD 1.4 trillion in 2023 and is expected to grow to USD 2.1 trillion by 2030. The bancassurance model has become particularly well established in Europe.

However, in Germany, the bancassurance market lags behind with a total volume of around EUR 23.5 billion in gross premium income in 2023. In particular, rising interest rates and the subsequent slowdown in new life insurance business have resulted in annual growth of only 1% in recent years.

For more information on market developments and trends, see our article “The German bancassurance market: underestimated potential with growing challenges”:

Despite the current market situation, some retail banks generate significant commission income via the bancassurance channel. However, when comparing an average Sparkasse or Volksbank with the leading institutions, the zeb.Retail Banking Study reveals that in many instances there is potential to double commission income from bancassurance.

The key to this lies in systematically increasing customer share of wallet. Successful banks have recognized this opportunity and established close partnerships with their insurance partners, integrating the insurance business deeply into the bank’s internal processes and IT structures.

What are the most important success factors for bancassurance cooperations?

Cooperation between banks and insurance companies is not a sure-fire success. The bancassurance market is primarily dominated by large and established partnerships. Against this background, the question remains: how do some banks manage to steadily expand their success with their business model, while others face ever greater challenges? What makes these bancassurance cooperations successful ?

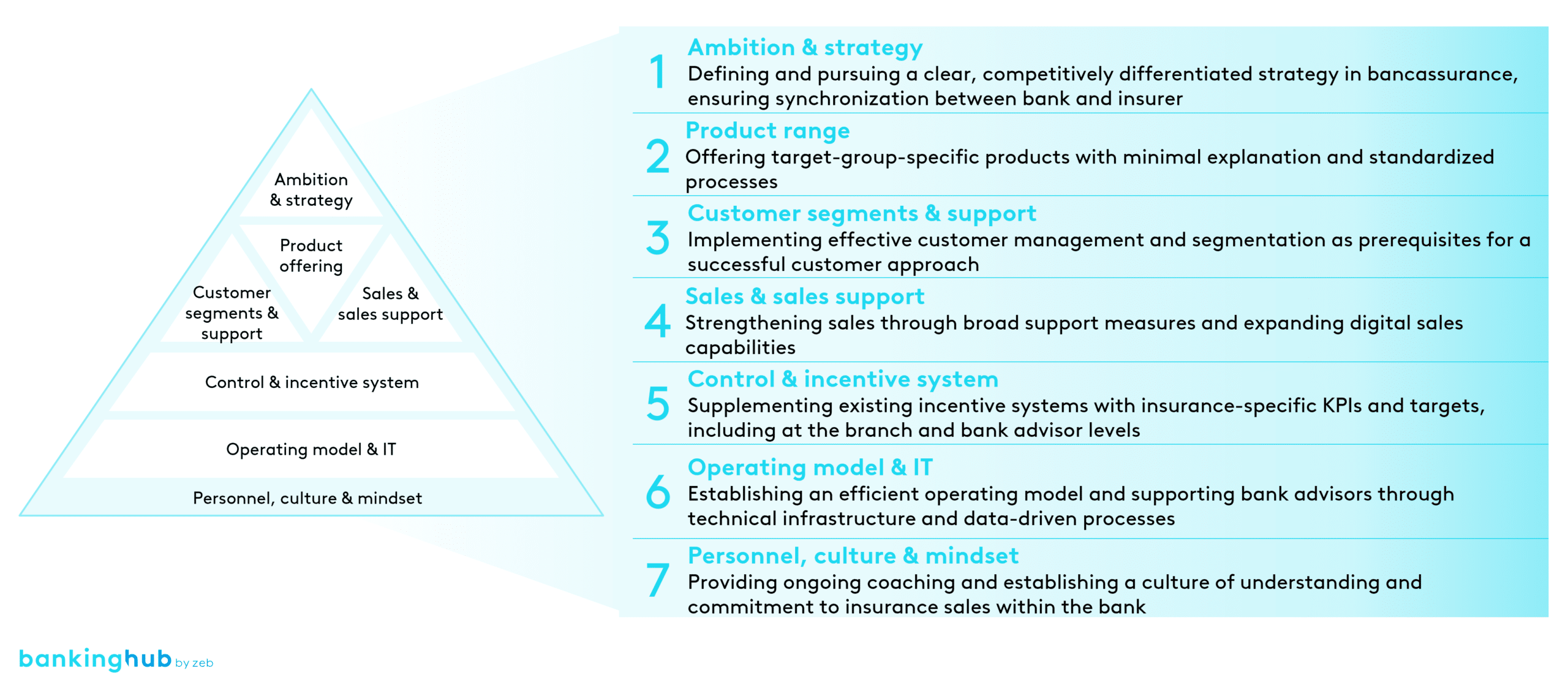

Our analysis of European bancassurance cooperations identified seven key success factors.

The aspects of product range, sales & sales support and operating model & IT proved to be of particular import. Below, we therefore examine the three most relevant success factors and present selected best-practice approaches for implementation.

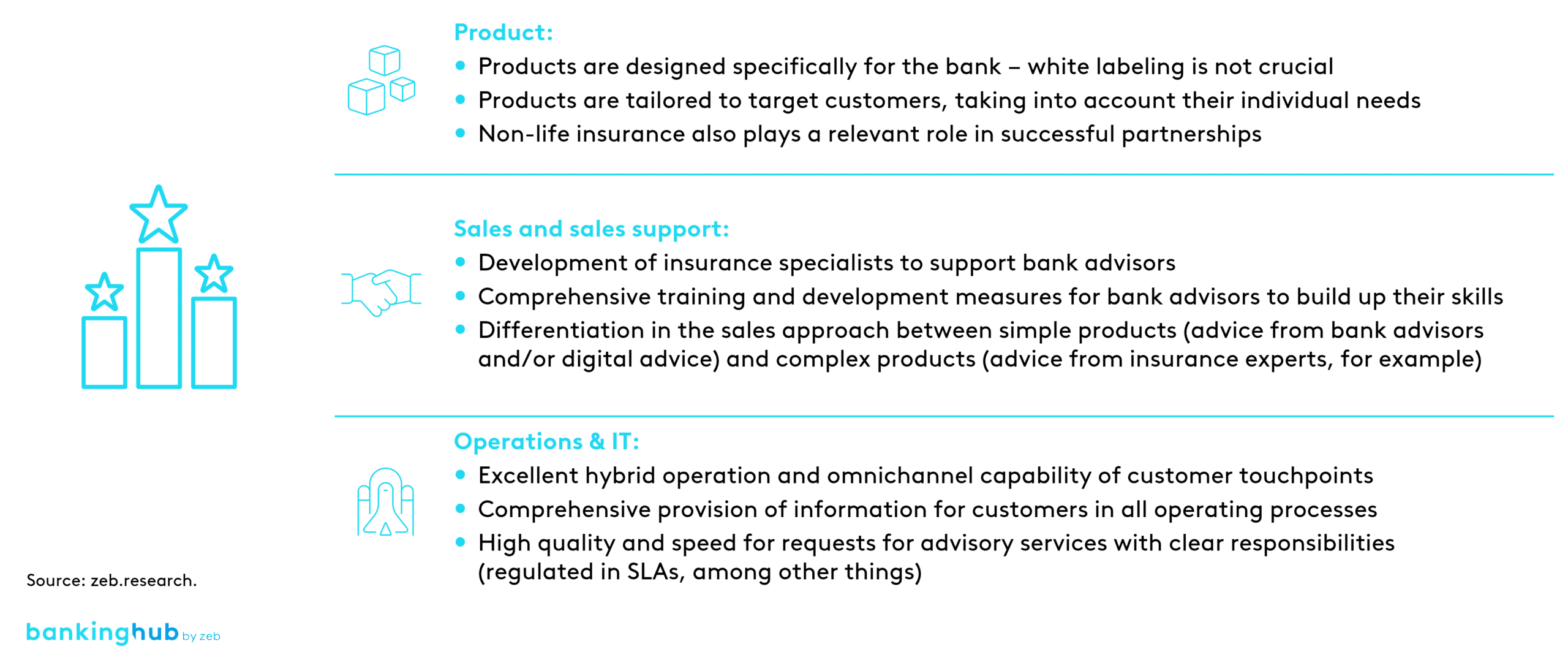

Product range as a success factor

A promising product offering targets specific groups and includes comprehensible products that both bank advisors and customers can easily understand. In the retail banking market in particular, there is a demand for flexible, modular products that cater to individual needs. Successful life insurance products, for example, often incorporate capital market components that meet customers’ sustainability requirements. Additionally, it is crucial to balance price and performance, especially for price-sensitive target groups. The option to purchase and manage these products digitally has become standard. These products should be designed for conclusion via the bank website, online banking, or mobile banking apps, allowing customers to manage them independently.

A best-practice example is a French bancassurance group that provides bank-specific insurance solutions such as residual debt and leasing installment insurance. Similarly, a Spanish banking group meets customer expectations with modular non-life insurance policies. For instance, it offers travel insurance that can be activated via an app and billed on a pro-rata basis depending on usage.

Sales & sales support as a success factor

Another key to the success of bancassurance cooperations is a clear and targeted focus on bancassurance sales with effective sales support. Sales funnel analyses can provide valuable insights into the challenges faced by customers and advisors. The expansion of digital communication and advisory channels is also a decisive factor. Digital and hybrid solutions can significantly boost sales success, particularly for simple products. For more complex products, however, the skills and qualifications of the sales force are crucial, requiring appropriate sales tools and targeted training in sales techniques. For more complex products or special customer needs, bringing in insurance specialists has proven effective. These experts support the bank’s employees and develop customized solutions.

A large Italian bank deploys insurance specialists for specific regions and markets. These specialists collaborate with bank advisors on-site to develop solutions for customers, thereby improving service quality. This institution also offers comprehensive training and further education programs. Branch employees are generally trained as advisors for comprehensive financial planning – including health, work, cars, homes and pets – as well as specialists for business customers.

Operating model & IT as a success factor

Successful bancassurance partnerships rely on an efficient operating model and a high-performance IT infrastructure. These elements form the foundation for a comprehensive range of services, high quality and good accessibility, which are crucial for customer satisfaction and loyalty. Flexibility is key to adapting to changing market conditions and customer preferences. Data analytics can help identify customer-specific needs and support bank advisors in targeted product advertising. Insurance topics should therefore be integrated into the institutions’ advisory software. A high level of automation, such as through self-service solutions, relieves the burden on employees and enables the quick and digital provision of information. Clear responsibilities and service level agreements between the bank and the insurer are the prerequisites for high process quality and speed.

One example of a successful implementation is the omnichannel platform of a German banking group. This IT infrastructure integrates all sales channels and is built on a consolidated database and modular architecture. It enables seamless communication between customers and bank employees without media discontinuity. External partners and applications can be flexibly connected via programming interfaces. Automated processes ensure greater efficiency and enable centralized, data-driven customer management. The omnichannel platform facilitates the insurance business by integrating insurance products into banking processes and enabling the respective banks to offer their customers individual and comprehensive solutions across all channels.

What are the key findings from the European bancassurance cooperations?

The best-practice approaches mentioned above indicate why successful bancassurance cooperations perform better than the competition.

Below we summarize the most important findings and approaches of the three success factors mentioned above from the European market.

Successful bancassurance cooperations are characterized by seamless integration of insurance sales into bank processes. Clearly defined common goals with the insurance partners are essential. Successful products meet customers’ exact needs and are easy to understand for both customers and bank advisors.

The institutions also successfully implement this consistent customer orientation in sales. Customers benefit from digital communication and acquisition options, combined with the targeted advisory expertise of bank advisors. However, these factors can only be successfully implemented if banks and insurance partners focus seriously on this business area.

What role will bancassurance play for banks in the coming years?

Bancassurance has established itself as one of the leading sales channels in Europe, particularly in the sale of life insurance. In contrast, the German market still has some catching up to do. Nevertheless, some banks manage to generate substantial commission income through this channel, while others fall short of their expectations.

Our analyses have identified a balanced product portfolio, comprehensive sales support and an efficient IT infrastructure as key success factors. Digital and hybrid sales models, along with a personalized, data-driven customer approach, are becoming increasingly crucial for success.

In view of current market developments, one thing is clear: only banks that focus on the bancassurance business area and are able to seamlessly integrate insurance sales into their processes will be able to compete in the long term.