What is staking?

Decentralized Finance (DeFi) staking services involve actively participating in transaction validation within a Proof-of-Stake (PoS) distributed ledger technology (DLT) network. Participants deposit their digital assets with a validator, earning periodic rewards in return for their contribution to validating transactions.

Staking represents an advanced DeFi service, often provided by crypto-asset service providers (CASPs) when there is an offering for the custody of digital assets, such as cryptocurrencies, crypto securities and security tokens. The primary goal of staking services is to generate additional income for both investors and CASPs. In principle, it is possible to stake digital assets like Ether, which operate on a PoS consensus mechanism within the DLT network.

What are the different forms of staking?

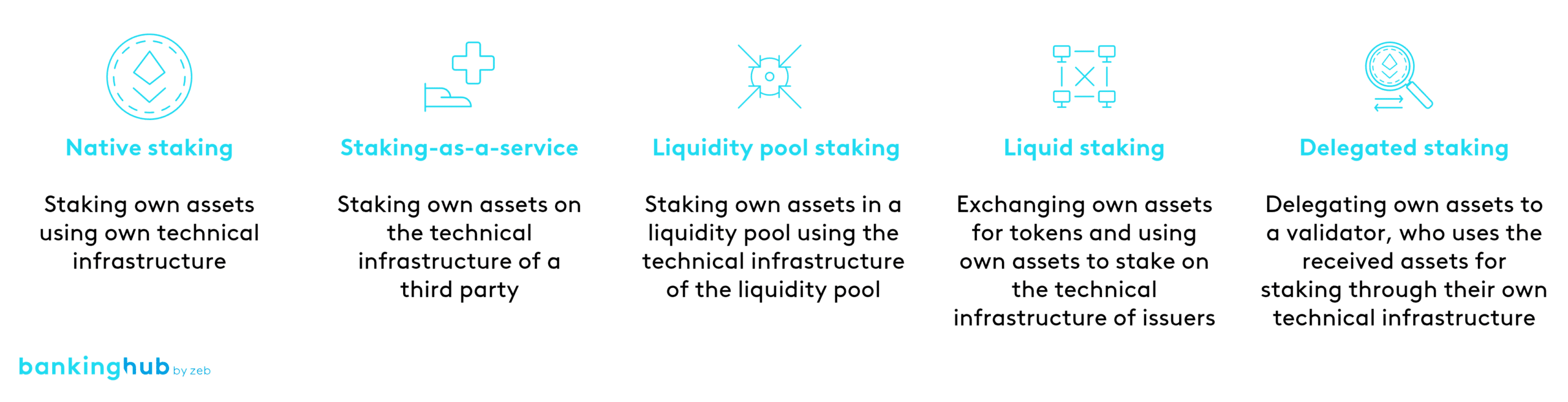

The forms of staking listed in Figure 1 can be specified as follows:

- Native staking: Holders of digital assets operate their own node and use their digital assets directly to validate transactions and receive rewards.

- Staking-as-a-service: Holders of digital assets use the technical solution of a staking-as-a-service provider. This provider handles the operational processing, including receiving rewards, and the operation of blockchain nodes, including setting up and maintaining the nodes.

- Liquidity pool staking: Holders contribute their digital assets to a liquidity pool. The digital assets contained in the liquidity pool are used for staking, and the rewards are distributed to the token holders proportionally.

- Liquid staking: In this case, holders provide their digital assets to a liquid staking platform and receive a token, such as staked Ether (stETH), in return. These tokens represent the value of the staked digital asset and can be traded on various exchanges. Staking rewards are distributed to the token holders.

- Delegated staking: Holders delegate their digital assets to a validator. The validator uses these assets to validate transactions with their own node. After receiving the rewards from the validation of transactions, the validator initiates the allocation of the rewards to the holders.

How does delegated staking work?

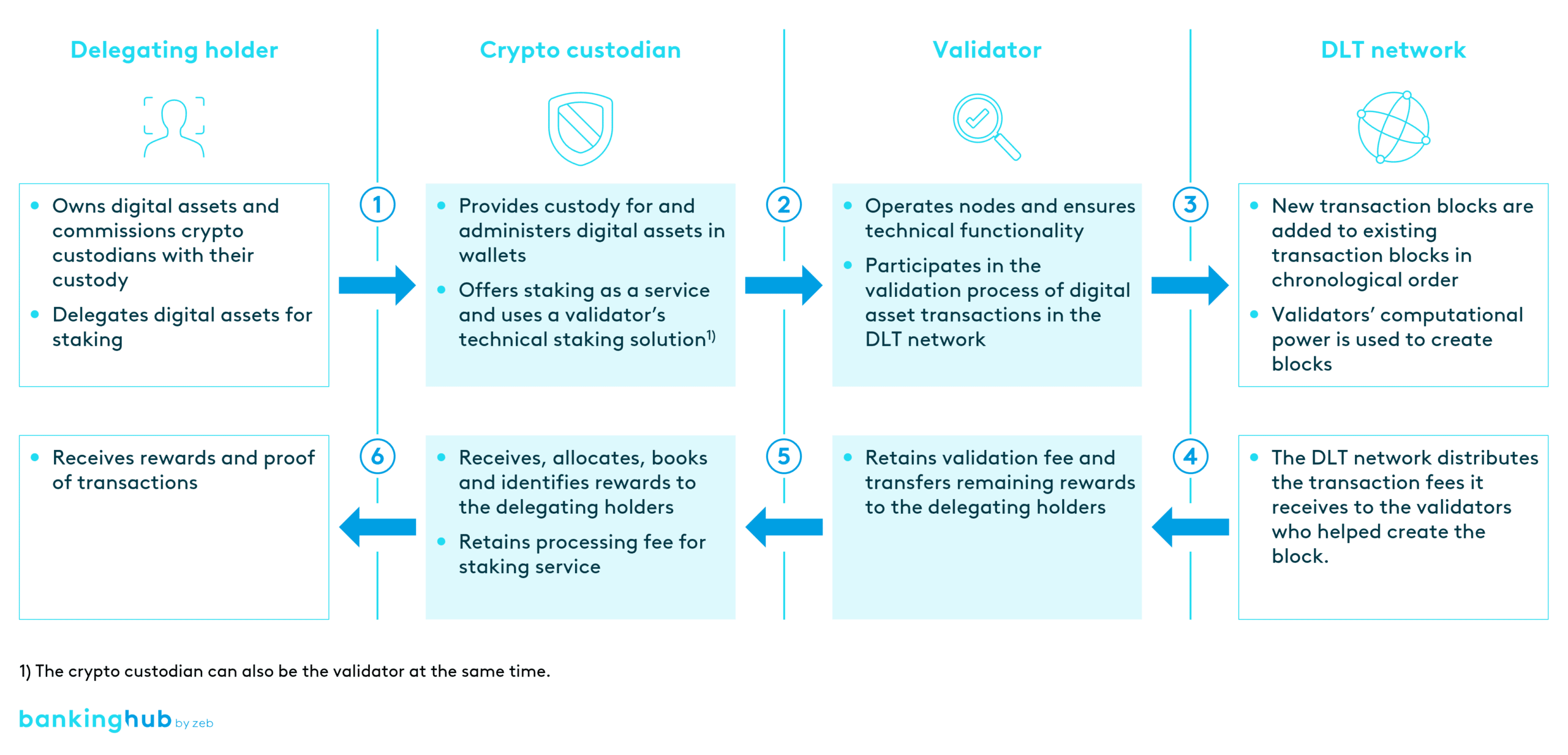

This article takes a closer look at the form of delegated staking, as this can be provided by licensed crypto custodians as a staking service for both private and institutional investors and can already be observed in the market.

Delegated staking generally requires a delegating holder of digital assets, a crypto custodian, a validator including a node, and a DLT network with a PoS consensus mechanism.

Staking mechanisms vary between different DLT networks, but in general can be listed as follows:

In order to use staking services, investors must have staking-enabled digital assets in their wallet. The number and digital assets to be staked are selected by the investor and delegated to a validator. There is no transfer between wallets.

The digital assets remain in the delegating holder’s wallet and are blocked or reserved. Locking/reservation means that immediate sale of the digital assets is not possible. However, the delegating holder can “undelegate” the locked or reserved digital assets at any time. This removes the lock/reservation.

The digital assets delegated to the validator are used to validate locks in the DLT network. The validator uses the assets to operate as many nodes as possible, thus increasing the chances of being selected by the DLT network as the creator of a transaction block. Typically, a minimum amount of digital assets is required to operate a node.

In a DLT network, the probability of validating or creating a transaction block is influenced by the number of nodes in operation and thus implicitly by the amount of digital assets.

Transactions are validated and new blocks are created at the validator nodes. Upon successful validation or creation, the validator receives a portion of the validated digital assets from the DLT network as a kind of “fee” for its service (the so-called block reward). The majority of the digital assets received are passed on to the delegating holders.

Typically, the rewards are distributed to the delegating holders at regular intervals (usually daily or weekly). The amount of the payout varies and depends on various factors, such as network usage or the number of blocks successfully validated.

What are the commencement and termination periods for staking activities?

It is often not possible to start or end staking activities immediately. DLT networks often require certain warm-up and cool-down periods during which digital assets intended or used for staking are locked and do not generate staking rewards.

The length of these periods depends on the underlying DLT network, but the following periods are often observed:

- Warm-up periods: After a user releases their digital assets for the staking process, there may be a delay before those digital assets are used to validate transactions.

- Lock-in periods: Staking protocols may require a minimum holding period for digital assets provided for staking. This period can range from a few days to several months, depending on the network.

- Cool-down periods: When a participant decides to stop staking (unstake), there is often a cool-down period during which the digital assets are still tied up.

What are the regulatory requirements for staking activities?

The regulatory environment for staking activities is still in its infancy but is developing very dynamically. In the EU, staking regulations can be observed implicitly through the Markets in Crypto-Assets Regulation (MiCAR) and explicitly through the EU Directive on Administrative Cooperation (DAC 8).

Staking services are not explicitly mentioned in MiCAR or in German national legislation. Nevertheless, indirect regulatory requirements for staking services may arise from MiCAR, in particular from Art. 75 “Providing custody and administration of crypto-assets on behalf of clients”.

According to MiCAR, the delegation of rights to a client’s crypto assets (e.g. Ether) required for staking may fall under the execution of orders for crypto-assets. Accordingly, licensing pursuant to MiCAR Art. 75 Para. 1 Cl. 1 may be required for delegated staking with crypto assets of clients.

In addition, MiCAR defines an entitlement of clients in relation to crypto assets resulting from a position in crypto assets of the client pursuant to Art. 75 Para. 4 Cl. 3. The positions resulting from staking must be entered in the client’s portfolio in accordance with MiCAR Art. 75 Para. 4 Cl. 2, and the corresponding transactions must be reported.

The BaFin guidance note on crypto-asset services under MiCAR contains a special provision on the regulation of stakes. Crypto custodians or wallet providers must verify whether they provide the crypto asset transfer service in accordance with MiCAR as part of staking activities in which transfers are received through smart contracts.

The fact that staking is generally considered to be a separate service is evidenced by its explicit description as a service in DAC 8, which also extends the scope of the EU legislation to include new tax reporting obligations for crypto assets. The extension of reporting obligations is intended to give both the tax authorities and the regulatory authorities insight into profits and income from crypto activities such as staking, and to deepen cooperation between the EU member states.

There are still unanswered questions regarding the regulation of staking activities. Accordingly, market participants expect that stricter regulatory initiatives and legislation in the areas of consumer protection as well as transparency and security requirements will provide more clarity on staking as a financial service in the foreseeable future.

What are the implications of staking for the financial industry?

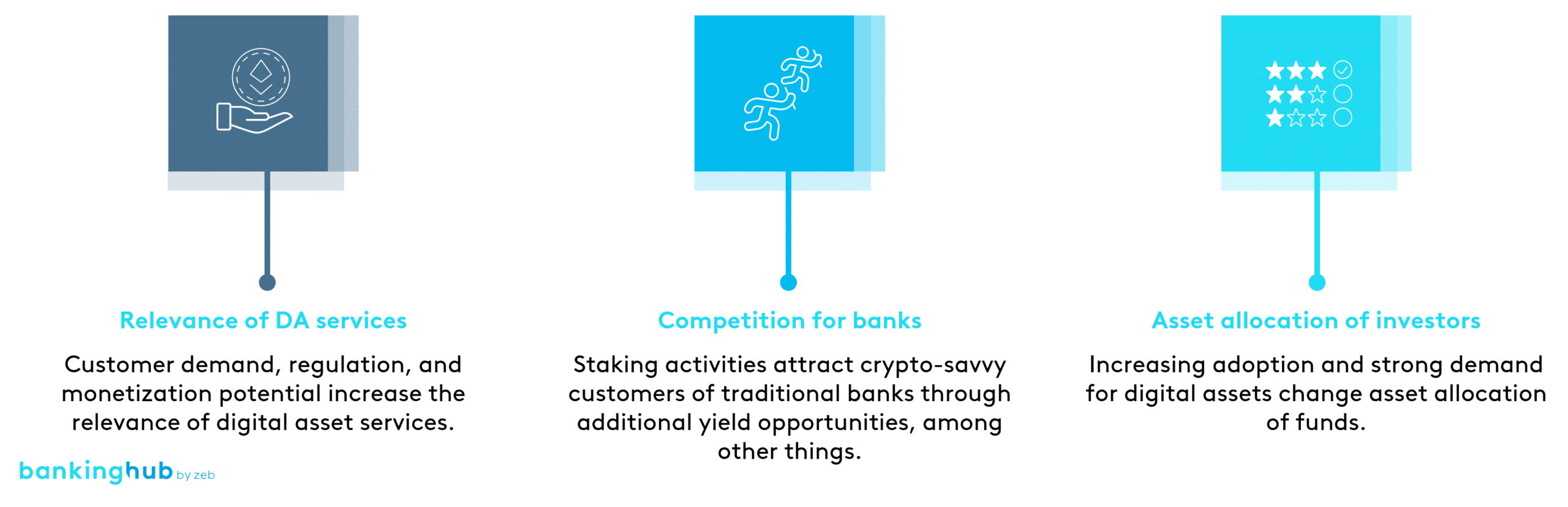

Staking has far-reaching implications for the financial industry in Germany, impacting various aspects of the value chain as well as the use and acceptance of digital assets such as cryptocurrencies. It enables both investors and CASPs to generate additional income. Staking has the following implications for the financial industry:

- Relevance of digital asset services: Staking is an advanced digital asset service. Accordingly, the provision of staking activities requires that basic services such as custody, asset transfer, and trading of digital assets be established beforehand. In addition, the ability to stake leads to increased demand for digital assets on the part of customers and increased monetization potential for financial institutions offering these services, thereby further increasing the relevance of digital asset services.

- Competition for banks: The growing ability of investors to use staking services from CASPs increases the pressure on traditional financial institutions. The risk of losing existing customers to neobanks and fintech companies offering staking services is particularly relevant for customers with a high level of crypto affinity. In addition to the preference of crypto-savvy bank customers for a one-stop-shop solution, the monetization of digital assets through staking rewards is leading to a transfer of capital from bank deposits to crypto investments.

- Changed asset allocation: Additional and relatively predictable returns from staking activities incentivize investors to allocate a higher proportion of their capital to digital assets. As a result, the future asset allocation of both institutional and private investors may increasingly shift towards digital assets. Accordingly, there is a growing demand for opportunities to trade, provide custody for, and stake digital assets instead of traditional assets and banking products.

What next steps should financial institutions take with regard to staking?

The growing importance of staking raises the question of how financial institutions can best position themselves in this area. According to zeb, the best approach is to address the issue early and actively build up expertise.

The following steps should be taken:

- Market, customer and competitive analysis: assessing the market size and growth potential of staking services and conducting customer and competitor analyses

- Scenario evaluation: creating scenarios for the future development of staking and assessing the expected probabilities of these scenarios

- Analysis of the impact on the business model: analyzing how the developed scenarios will affect the existing business model across the entire value chain

- Prioritization of areas for action: deriving and prioritizing potential areas for action based on the analysis of the impact on the business model

- Derivation of a positioning: developing a fundamental position on the topic of staking based on the scenarios and analyses and establishing this position in key decision-making bodies