Many banks find their IT support for lending business insufficient at some point. The deficiencies materialize in the functional support of specific products, needs for manual bridging of process steps, miscalculations, or other problems. Faced with such challenges, banks can either initiate upgrades of their existing IT systems or turn to the market for professional IT solutions. Both approaches require much effort, have their advantages and disadvantages, and are advocated by different stakeholders within the organization. We believe that, especially when turning to the market for a professional lending package, banks need to involve a full list of stakeholders and approach the planned change in IT with a broader perspective. For this scenario, we propose a holistic framework which can take you all the way: from the identified need for a change in lending IT support to the definition of the scope for a new solution, taking into account different points of view of various stakeholders within your organization. We also defined points of view of different stakeholders according to their expectations, i.e. their underlying drivers of change.

Who drives the change in lending IT?

In the initial phase of such change initiative it is important to identify and analyze different drivers for the envisaged change. The results of this analysis pave the way towards a decision on the approach to the new IT solution. Only then the solution can be selected and implemented.

In the past, business departments (e.g. Sales, Coverage, Product Management, Sales Support, etc.) drove changes in lending IT. Whether it was about closing the existing functional gaps in their existing IT systems (e.g. manual bridges in process flow, etc.), or addressing the future business needs (e.g. new products launched, sales campaigns, etc.), it was usually a single business domain which would be in the driving seat. The focus on solving particular business needs implied that the solution would address only an isolated issue within the context of the whole organization. Furthermore, the opportunity would not be fully exploited by missing out potential synergies that could be obtained by taking a broader perspective in this matter.

Recently, the increasingly complex environment for banking (such as the regulatory tsunami, extreme cost pressure, new competitors, digitalization etc.) dramatically accelerated the need for changes in IT. The multitude of challenges requires now a more holistic approach which accounts for different interests of stakeholders in the lending process.

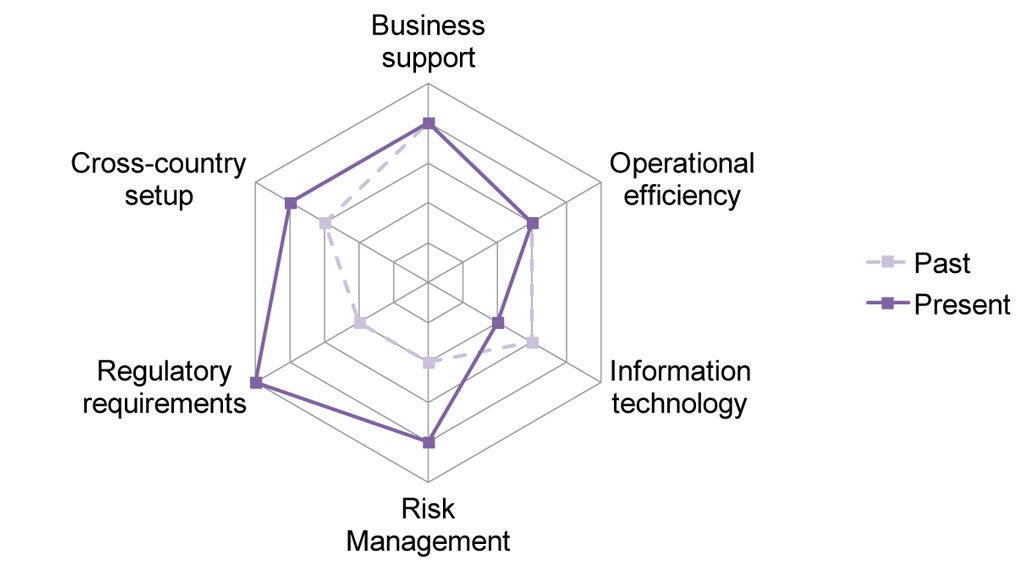

Illustration 1 shows a view on the main drivers for the change in IT support for lending business in banks, mapped according to their past and current impact on IT decisions:

Illustration 1: Main drivers for changes in IT systems supporting lending business

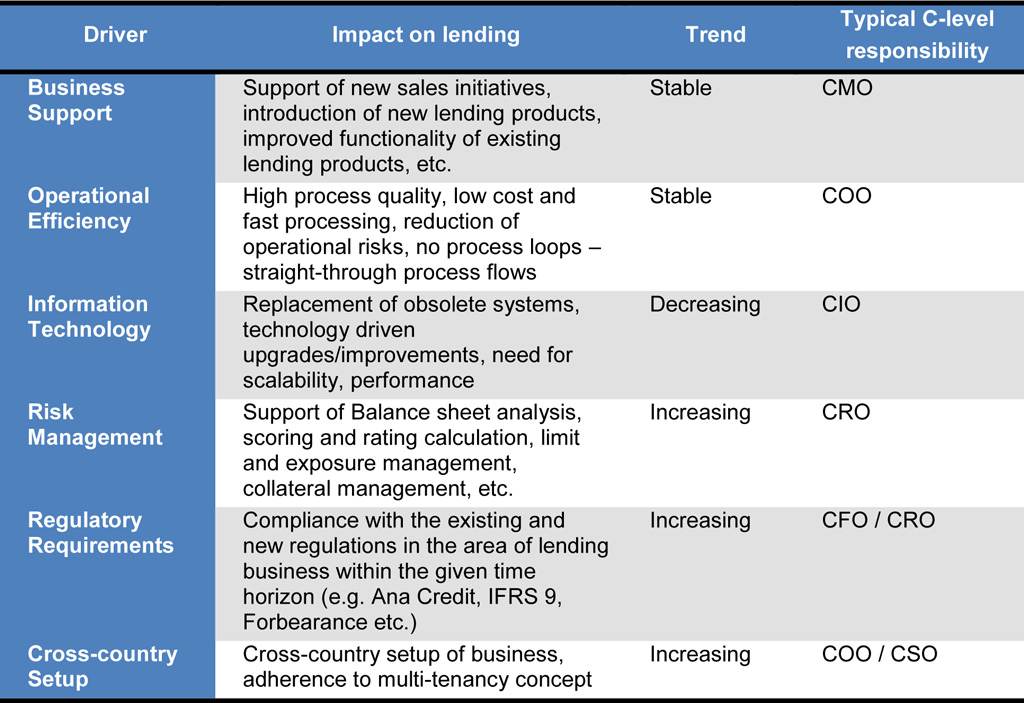

Illustration 1: Main drivers for changes in IT systems supporting lending businessIn illustration 2, a brief description of each of the drivers is provided, as well as the trend for its impact for the final decision, as we perceived it in recent projects. We also added typical responsibility within a bank:

Illustration 2: Driver description

Illustration 2: Driver descriptionIn a nutshell, risk and regulatory aspects become more and more important, even for the selection of a transactional oriented system like lending. Deep functional coverage no longer provides the ultimate argument for the decision of selecting one system over the other.

Does your segment strategy influence the importance of individual drivers?

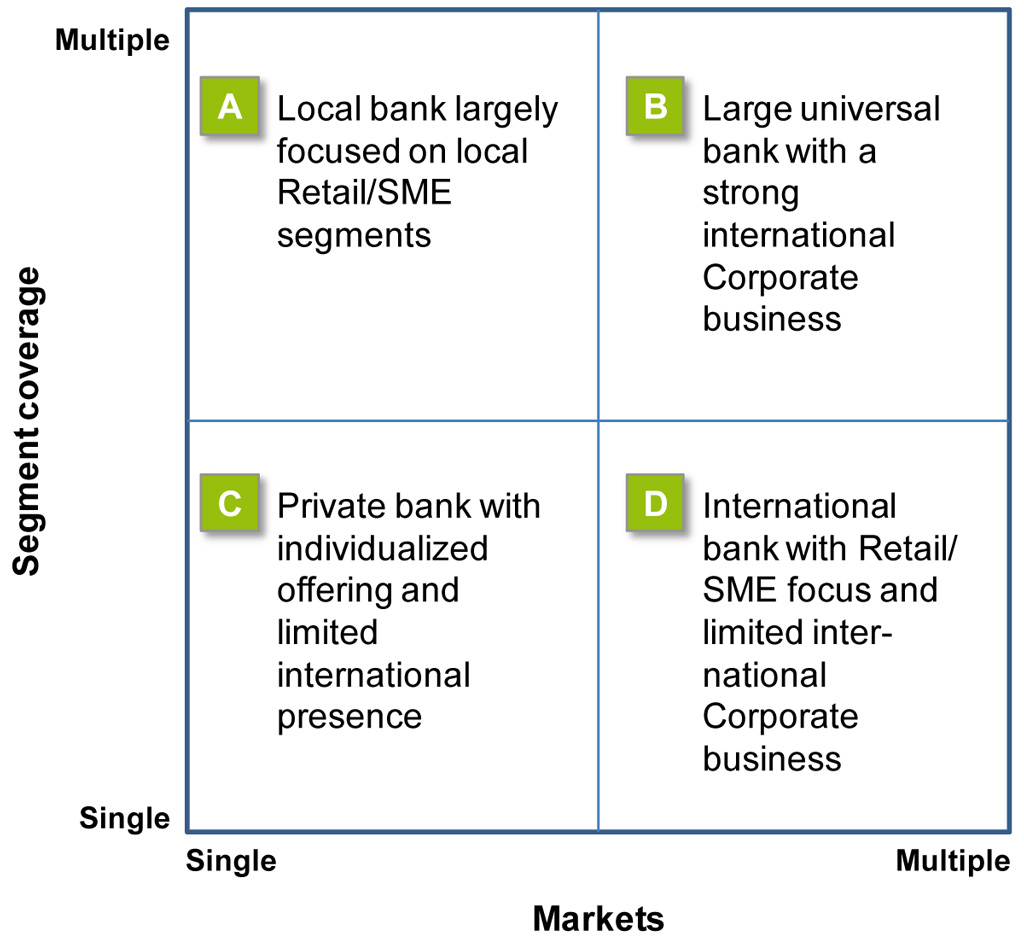

To simply answer this question – yes. But in order to be able to analyze the practical implications of different segment strategies in lending business on the importance of the individual drivers, first we needed to classify the banks into one of the categories based on their segment strategy. For that purpose we introduced four archetypes of banks.

Illustration 3: Bank archetypes

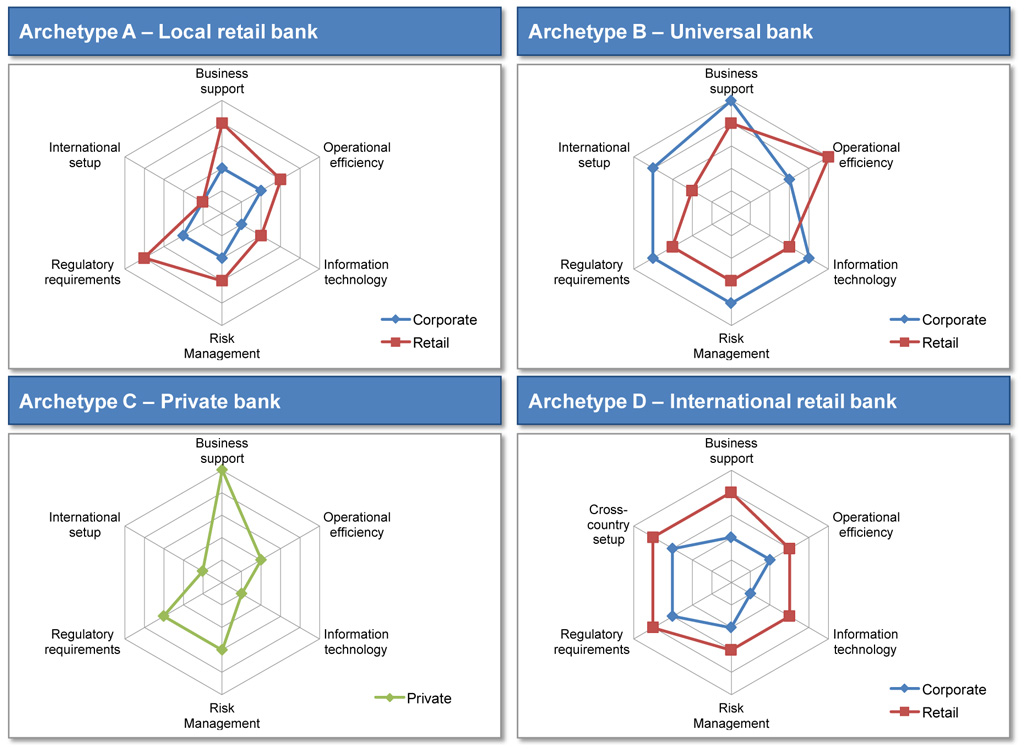

Illustration 3: Bank archetypesBased on these distinct archetypes, we mapped the impact of the main drivers which are different for each archetype of the bank.

Illustration 4: Driver impact by archetype

Illustration 4: Driver impact by archetypeBased on this analysis and the stated difference of the impact of the main drivers based on the segment strategy, we derived concrete recommendations in which direction the changes in IT support should go in order to maximize the benefits on the organizational level. But, before providing such recommendations, we would like to provide a short overview of the market offerings in terms of the lending systems.

What does the market offer?

Due to the high maturity of the IT market for lending business, there is a large number of solutions available on the market to choose from. The variety can present both a chance and a risk, depending on the selection approach. In general, all solutions can be categorized either as ”best of breed” (specialized) or as universal lending solutions. The key question for any purchase is whether to go for the former, typically clearly targeted functional coverage, or the latter, with usually much broader functional coverage. Not surprising, both come with their advantages and disadvantages:

Upgrading your lending IT by implementing a universal package can secure certain benefits over a dedicated “best of breed” specialized solution. These include easier vendor management (during and after implementation) and (very likely) successful integration into the existing IT landscape of the bank. The downside is that universal packages often offer wide but not very deep functional coverage in certain functional areas. In cases when there is a specific need for a deep functional coverage in particular lending areas (e.g. loan or guarantee syndication, project finance, etc.), “best of breed” solutions have the upper hand. The disadvantage, however, is usually the increased complexity and the risk of the implementation project itself (time, cost, vendor management), as well as increased complexity of maintaining the new IT architecture in the long term – resulting in substantially higher IT OPEX costs

The main advantage of “best of breed” solutions is to have the best possible functionality and would typically be favored by business departments. Issues lay in much higher integration complexity, data quality decrease, interrupted process flow, more complex vendor management especially in cases of coordinated software upgrades – all of which are key arguments for the Risk and Regulatory perspectives. Universal lending packages, on the other hand, can provide a fully integrated product set and thereby solve some of the named issues by default. High reliance on a single vendor, weaker functionality in some of the functional areas, lack of easy integration with software outside the vendor’s core product suite and (even) less control over future upgrades are on the flipside of the coin.

Which approach to follow?

Taking into consideration the importance of the individual drivers for each of the archetypes of the banks as well as market situation described in the previous chapter, we propose the following respective approaches:

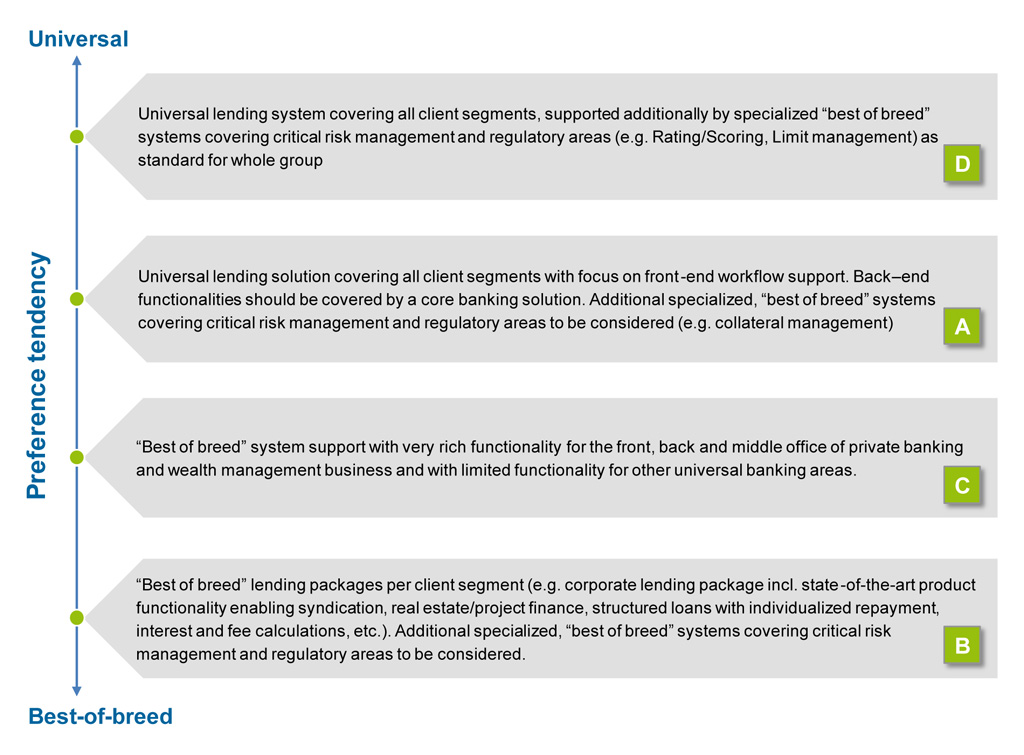

Illustration 5: Proposed approach per archetype

Illustration 5: Proposed approach per archetypeThe growing importance of Risk and Regulatory aspects is considered for all archetypes, especially for “D” due to the large internationalized corporate business, and as such is reflected in the proposed approaches. Still, lending solutions usually cannot provide coverage of Risk and Regulatory requirements on their own and specialized systems per area need to be considered. We propose rolling-out of these critical specialized systems across the group as a standard.

Specific budget/time restrictions and interdependencies with other initiatives need to be taken into account. When the scope of the solution is defined, next is to proceed with a detailed requirements definition, targeted market screening and analysis of available systems on the market along with their selection and finally implementation.

In our follow-up article, we will introduce an approach for selecting end-to-end lending systems. We hope to have quicken your interests, and would be highly grateful if you had interests on that topic, too.