The current impairment model encountered serious criticism in the past, not least in the context of the financial crisis of 2007/2008, the repercussions of which are still noticeable today. In particular, it was criticized that a risk provision only has to be created when a loss is actually incurred, so that investors, analysts and other stakeholders are not informed early enough about the potential credit default risk.

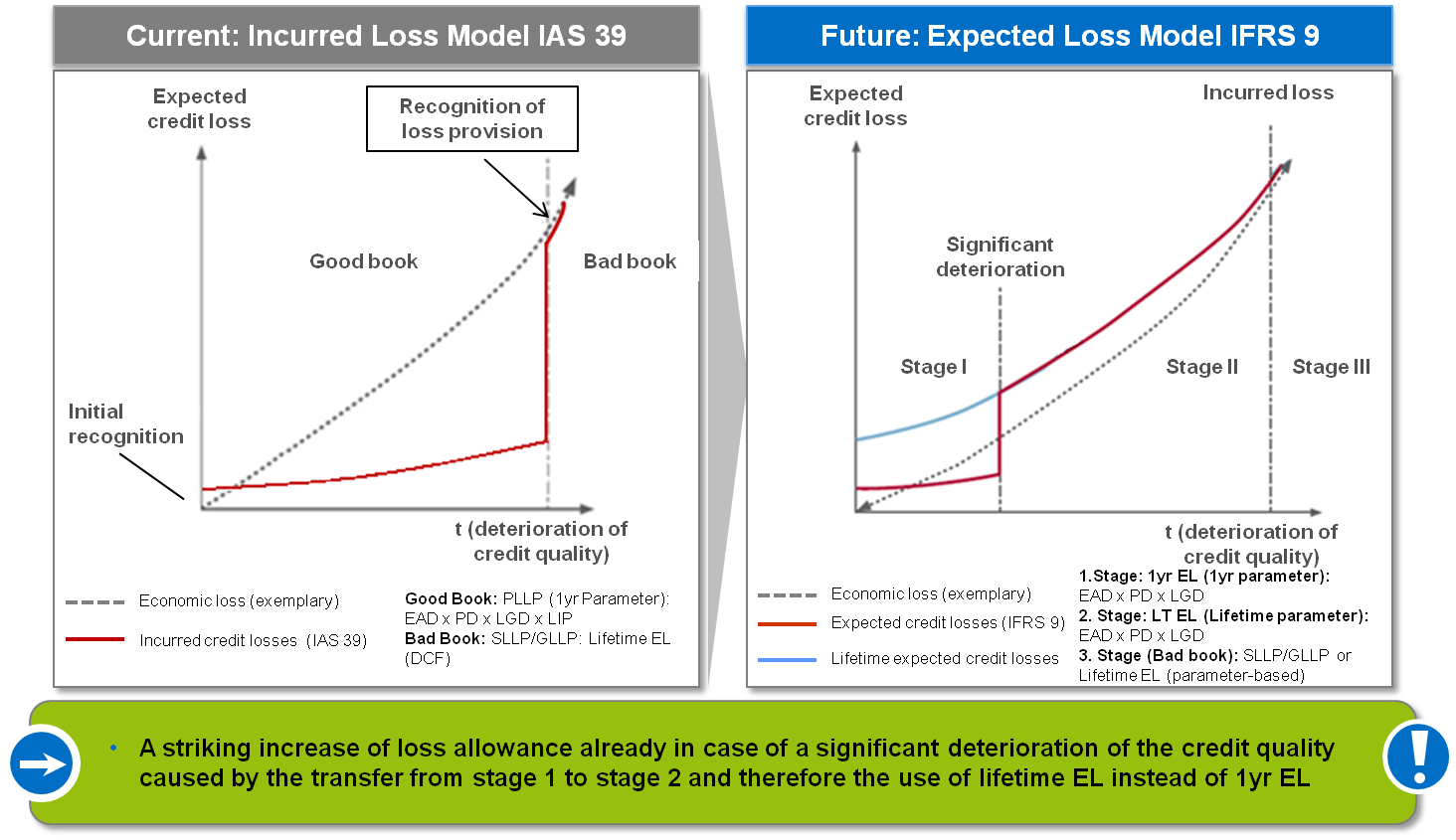

On July 24, the IASB published the new IFRS 9 impairment standard, and set January 1, 2018 as the initial application date. The regulatory framework of IFRS 9 introduces and defines a new impairment model, which aims to achieve a more adequate and timely provision of relevant information for decision-making processes. The model envisages that expected credit losses are no longer left unrecognized until the actual incurrence of a loss. Instead, they are recognized for the entire remaining time to maturity already from the point where a significant deterioration of the credit quality occurs, based on a future-oriented expected credit loss (EL) model (cf. figure 1).

Figure 1: Comparison of the impairment process under the current IAS 39 model and the future IFRS 9 procedure

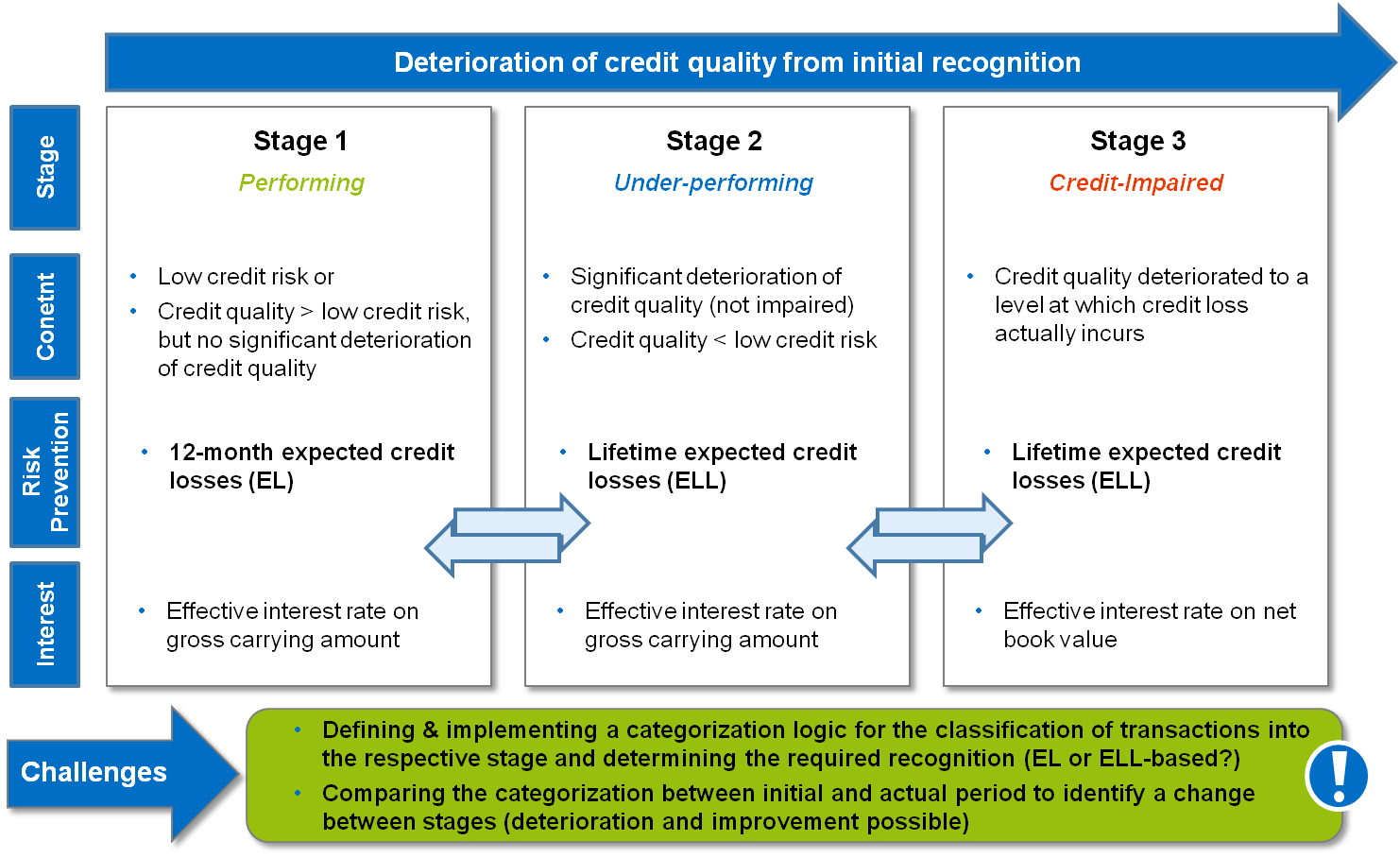

Figure 1: Comparison of the impairment process under the current IAS 39 model and the future IFRS 9 procedureIn the general approach of the IFRS 9 model, financial assets are categorized according to a three-stage model (cf. figure 2): All loans (with the exception of purchased or originated credit-impaired assets) are allocated to stage 1 at initial recognition; the size of the risk provision is determined on the basis of a 12-month EL (LIP factors do not apply anymore). If the credit quality deteriorates significantly after initial recognition and if the loan does not have a low credit risk (e.g. no longer rated with an investment grade rating) anymore, the instrument is transferred to the second stage, with the consequence that risk provision is now based on a lifetime EL (“Expected Lifetime Loss”). Stage 3 contains defaulted receivables, similar to the current IAS 39 procedure.

Figure 2: Overview of impairment levels under IFRS 9

Figure 2: Overview of impairment levels under IFRS 9In practice, the implementation of the expected loss-based model proves to be challenging, amongst others regarding the following aspects:

1. Methodical challenges

- Requirement to define and implement suitable models for an accounting-adequate expected loss and expected lifetime loss calculation for all financial receivables valued at amortized cost, certain receivables which are classified at fair value through OCI, certain loan commitments, certain financial guarantees and certain leasing receivables under IAS 17

- Required determination of appropriate categorization logics, credit quality indicators and threshold values for the three-stage model

- Consideration of plausible, future-oriented information and macro-economic developments for a regulation-compliant recognition of expected credit losses

2. Technical challenges

- Review and follow-up checks of periodic changes of the credit quality for purposes of (re-)allocation within the three-stage logic

- Definition system-related implementation of rights of choice regarding trading and leasing requirements

- Selection and implementation of appropriate technical impairment solutions, taking the cost/benefit ratio and the integration into the existing system environment into account

3. Process-related challenges

- Changing the delivery and reporting processes

- Ensuring that the impairment results can be reconciled to regulatory and other internal credit risk measurement results

- Process-related and organizational harmonization of the areas regulatory, risk, accounting and IT

4. Strategic challenges

- Identification of suitable measures to reduce the size of risk provisions and the P&L volatility

- Handling the expected reduction of the equity ratio due to initial application effects

- Review of the product catalogue and ensuring competitiveness

- Audit assurance for the applied methods or simplifications

- Consistency of methods compared to other areas such as risk or regulatory

For the upcoming implementation of IFRS 9, sufficient preparation is necessary in view of the various methodical, technical, process-related and strategic challenges.

zeb has gathered extensive practical experience with regard to the implementation of impairment solutions all the way from the conceptual design and simulation calculations to the technical implementation by means of standard software.