IIRC—A global initiative

Approaches for a new form of business reports date back to the beginning of the 90s. However, only the foundation of the IIRC in August 2010 established a serious organization for a global standard and prevalence. The committee consists of representatives of large audit companies, CEOs and CFOs of large enterprises as well as representatives of the part of investors and analysts. It developed a joint framework concept, which defines guidelines and contents of an integrated report. At the same time, a pilot program was launched in order to test the guidelines in practice.

The motto: Less is more

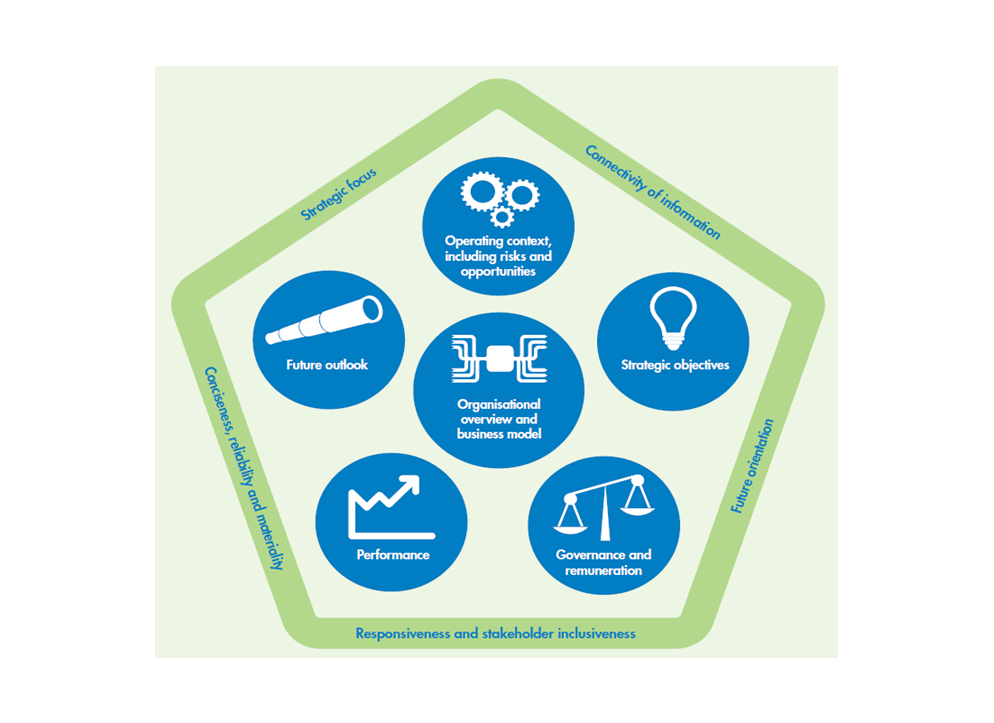

One of the relevant principles in the framework concept is conciseness and significance. Instead of a long list of detailed financial data, the corporate success isn’t measured against few, selected financial and non-financial KPIs. The IIRC recommends a length of approx. 50 pages. The practical connection of information is another maxim of the integrated report. Connectivities are to be explained and the basic processes in the company are to be made understandable. In the end, a holistic corporate image with not only classic report contents but also information from the management and sustainability report should be conveyed to the target group.

Away from the reference to the past to the future success potential

The content-related focus is laid on the capacity of the company to create values. In this regard, not the success data of past periods are to be considered, but rather the factors, that will influence value drivers in future, first and foremost the business model and the corporate strategy. They are particularly decisive in the financial services sector. It becomes ever more difficult to differentiate oneself from the competitors and to offer the customer a realized added value. Non-financial aspects that can be communicated in the integrated report play an increasingly important role. Therefore, governance and the relationship to individual stakeholders and the environment are focused on.

Figure 1: Illustration of report contents and principles (source: IIRC)

Figure 1: Illustration of report contents and principles (source: IIRC)Capital—A new definition of the capital term

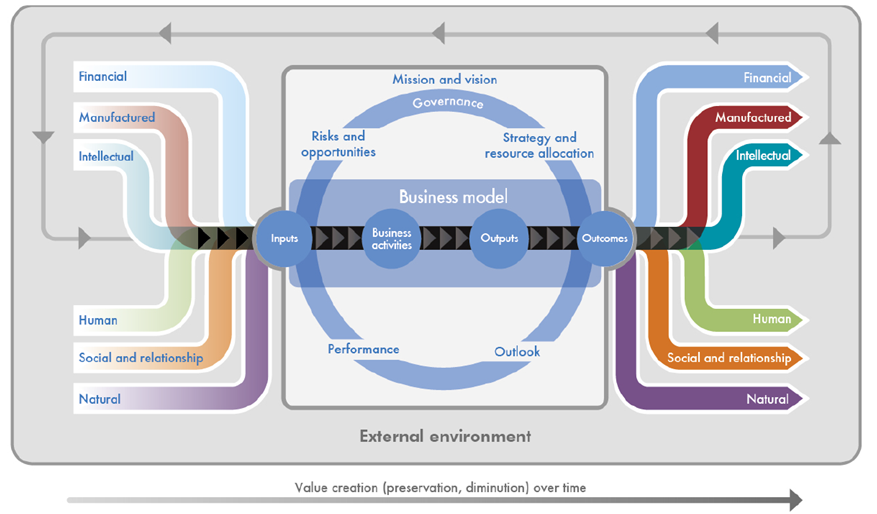

The integrated report differentiates six different forms of corporate capital. The financial, the manufactured, the intellectual, the human, the social and the natural capital. Depending on the activities of the company, these capitals are reduced, increased or transformed. The balance of the capitals corresponds in turn to the value creation of the company. Thus, the fact that the value of a company, and in the end the capacity of creating value, increasingly depends on non-financial aspects is taken into account. Only 20% of the market capitalization of S&P 500 can be explained with the help of the financial and manufactured capital.

Figure 2: Schematic illustration of value creation in the integrated report (source: IIRC)

Figure 2: Schematic illustration of value creation in the integrated report (source: IIRC)How an integrated way of thinking can improve the management

The way to an integrated report doesn’t only concern the reporting area. It rather requires a change within all corporate areas. Diverse information is to be collected locally and recognized via standardized processes. The management significantly benefits from it. New connectivities can be realized and efficiency potentials can be leveraged. An integrated way of thinking often leads to improved results, in decision-making processes as well.

A central information hub for all stakeholders

Of course, the interests of current and potential investors are to be taken into account in reporting the most. But the information need of other stakeholders has been on the increase in the past years. An integrated annual financial statement, in connection with the opportunities of digital technology, can individually react to this need. It serves as a central overview and starting point, from which the user is led to further information, such as sustainability data or financial details. The information need of applicants is to be mentioned in this context. An integrated report is also a measure of employer branding.

The integrated report has already been realized

The IIRC has launched a piloting program simultaneously to the development of a framework concept in order to gather practical experience with integrated reporting. More than 100 companies and 35 investors are part of it, 35% of them belong to the financial services sector. Deutsche Bank, Deutsche Börse and SAP are amongst the six German participants. The feedback is mainly positive, especially the effect of an integrated way of thinking on the corporate culture is praised. Furthermore, the companies that establish an integrated report are considered to be very innovative.

Opportunities for financial institutions

The integrated report offers in particular banks the opportunity to regain trust with the help of changed communication. Vancity—a Canadian cooperative bank with 492,000 members and participants of the piloting program—uses the new reporting form in order to communicate the added value, that the bank creates for society, to members as well as third parties. The introduction of a standardized scoreboard of the business and sustainability report, which is assessed externally and in a transparent way, made this possible. It comprises three target dimensions: “Impact”—the impact on the corporate environment, “confidence”—the strength of the business model and “integrity”—the orientation towards common good. Target values for the following period are defined based on the strategy, which makes success or failure understandable for third parties.

Reporting of the future

Integrated reporting cannot replace the current web of consolidated financial statement, management report and sustainability report on a short-term basis, in particular due to the strict legal requirements. However, the new way of reporting can already communicate innovation capacity and optimize the internal management of decision-making processes. There isn’t any company that will get around this topic on a long run, since legislators are expected to embrace and continue the approaches of the IIRC.