The need for a professionalized real estate asset management approach in banks

In the current stagnant European macro-economic scenario, most banks have seen their volumes of defaulted loans grow exponentially as bank customers have experienced increasing difficulties in paying off their debts.

The impact of higher volumes of non-performing loans on the balance sheets of banks is particularly dire in regions with difficult real estate market conditions, such as Southern and Eastern Europe (e.g. Italy, Greece, Balkans)[House Price Index, Eurostat, 2014], or in regions facing the aftermath of real estate bubbles (e.g. Spain, Ireland). During real estate bubbles the number of real estate construction sites sharply increases and the price of real estate properties soars, fueled not only by an increasing demand for properties but also by the speculation that demand itself will stay strong and that real estate prices will continue to grow. With increasing real estate market prices, the volume of real estate project finance operations and mortgage loans granted by banks rapidly grows, driving up the capital reserves that banks need to set aside to cover potential future loan defaults. When it becomes clear that real estate forecasts are not as positive as expected and market demand starts to decrease, real estate prices plunge and in case debtors default on their loans, banks face increasing capital requirements through these defaulted loans and will eventually need to write-off part of the exposure. In case of real estate bubbles, these effects are even more significant due to the losses on the market value of the real estate collateral.

Needless to say that in the last years, as the overall European economic conditions worsened, the regulatory pressure on banking organizations has at the same time increased, in particular on the accuracy of the methodologies used by banks for the accounting and reporting of collaterals, as demonstrated by the recent asset quality review run by the European Central Bank [“Aggregate Report On The Comprehensive Assessment”, European Central Bank, 2014].

This scenario of tougher economic conditions and stricter monitoring from regulatory watchdogs has urged a growing number of banks to reassess the operating model they use to manage their portfolio of distressed real estate assets (i.e. the pool of real estate assets the bank has booked as collateral for its non-performing loans). The goal is to identify the areas (e.g. functions, policies, decision-making bodies, etc.) where a more competent real estate management approach should be applied.

This need has become particularly relevant for medium and large banking groups, with a significant portfolio of distressed real estate assets spread over multiple countries and subsidiaries. As real estate management is typically a non core business for financial institutions, banking groups tend in fact to lack the competences (e.g. in evaluating real estate asset quality, in forecasting real estate markets outlook, etc.) and the organizational structures (e.g. dedicated internal divisions, policies and procedures, etc.) required to steer a coordinated real estate collateral management strategy within the group.

Target strategies for distressed real estate assets

From zeb perspective, strategies to be applied to the portfolio of distressed real estate asset depend on the quality attributes of each individual real estate property (e.g. real estate segment, status and condition of construction, use of building and vacancy rate, etc.) and on the real estate market development potential or, in other words, the expected development of market prices for the particular real estate segment (e.g. commercial building, hotel, agricultural land, etc.) in a given country.

To this end, zeb has designed and developed a comprehensive set of decision criteria in the form of a scorecard logic matrix, used to assess the portfolio of distressed real estate assets. Similar to scorecards designed to assess loan applications from clients, zeb real estate asset selection model weighs up different individual real estate and market attributes according to pre-defined weightings and scorings, preliminarily aligned with the bank during a setup phase.

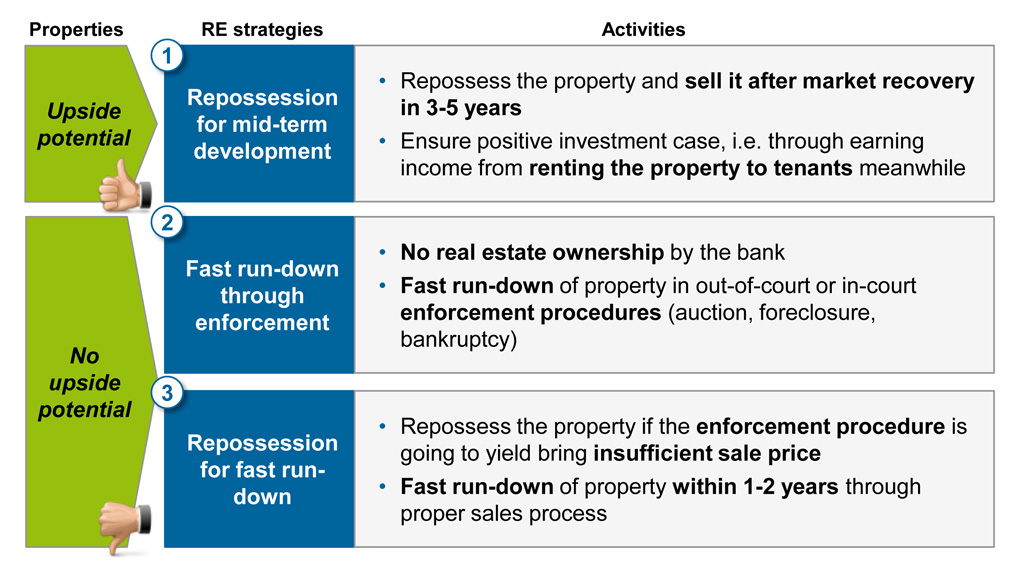

Properties of high asset quality (e.g. finished property in excellent condition and high rental yield) and with a promising market outlook (i.e. expected market price increase for the particular real estate segment in a given country) are considered as properties with upside potential, thus suggested to be repossessed by the bank from the defaulted client, actively managed (e.g. earn rental income from current/prospect tenants, maintain/develop the property, etc.) and sold after a potential market recovery in the medium term (e.g. 3 to 5 years) (cf. figure 1: strategy 1). Given the extent of the distressed real estate portfolio, the bank might in fact consider the opportunity to directly manage and develop a number of high quality real estate assets (especially in case of increasing market prices). However, an in-depth investment case (including DCF analysis) should be conducted for such properties in order to confirm a potential positive cash flow for the bank (i.e. positive sum of initial investment for repossession, incomes and expenditures during the bank’s tenure, final selling price, etc.). Also, considering the non-core banking nature of such strategy, a preliminary alignment with the regulator on investment strategies and capital requirements is considered to be crucial. In particular, the bank should not miss to inform the regulator that this strategy is only valid for a restricted period (3 to 5 years) and only for properties with high quality, for which a future sale to external investors at an increased market value is considered very likely and is indeed the mid-term goal.

Lacking specialized real estate asset management skills and a structured approach to identify properties with upside potential, most banks still tend to pursue a fast run-down strategy for their real estate collaterals (cf. figure 1: strategy 2). This strategy implies the sale of real estate collateral through in-court or out-of-court enforcement proceedings with the aim for the bank to at least partially recover the losses on defaulted loans. This also means to accept a significant lower selling price, since this strategy attracts bargain hunters trying to buy real estate properties below their market value. Ideally, this approach should only be considered in case of properties without upside potential (e.g. properties in bad condition, with high vacancy rate, etc.), properties still in early construction phase or properties with negative real estate market outlook (in the given real estate segment / country) in order to limit the losses on the value of the collateral. Finally, this strategy might also be applied if the exposure for a particular loan is significantly lower than the collateral market value and can then be covered by the price achieved in the enforcement procedures.

As a third option, in case the bank would assess that the enforcement of the property would generate an insufficient selling price, the bank might consider to repossess a property without upside potential with the sole goal to sell it within a short time (e.g. 1 to 2 years) at a price higher than the current enforcement value (cf. figure 1: strategy 3). In no case the bank should anyhow embark in large-scale investments for the development of this property during the period of tenure, as no positive market outlook is forecasted for the specific real estate segment/market. The main advantage of this third strategy compared to the fast run-down approach is that the bank would have sufficient time to initiate and conduct a proper sale process to sell the property at the current market value.

Figure 1: Target strategies for distressed real estate assets

Figure 1: Target strategies for distressed real estate assetsBooking and servicing of real estate collaterals: target real estate management organization

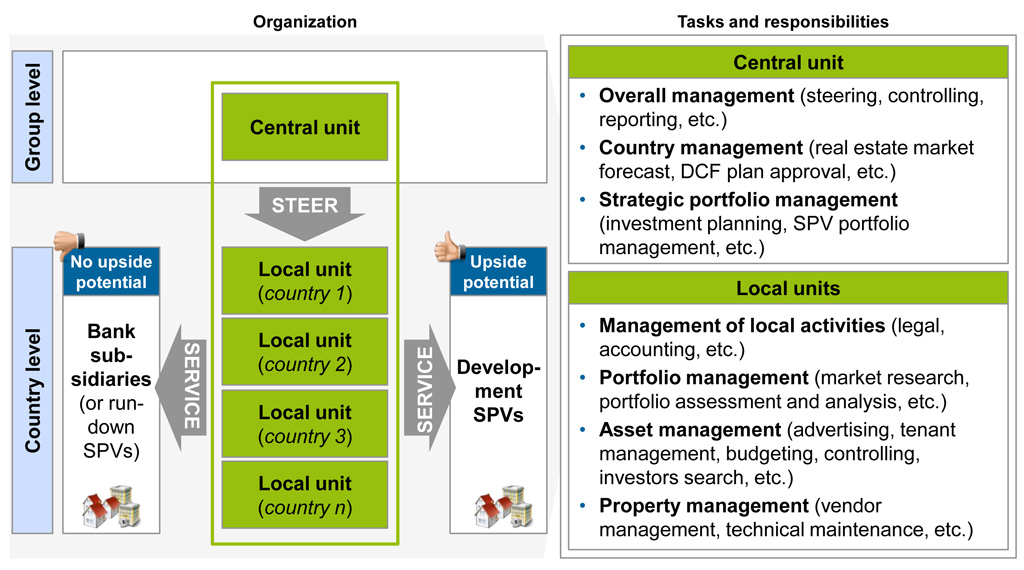

In order to enable a dedicated management of distressed real estate properties, real estate collaterals with upside potential are suggested to be transferred to the books of newly founded entities (development SPVs). These legal entities have an approved separate line of funding and are used to repossess the properties from defaulted clients and then sell them to external investors in the medium term. The number of so-called development SPVs and the composition of their portfolio of upside potential properties should be tailored in a way to meet the requirements of potential investors, based on their preferences for future equity deals. Investors typically adhere to one of the following categories: (i) institutional investors (e.g. pension funds, state funds, real estate investment funds), interested in single properties or small portfolios with cash flows from rental income in a long term perspective; (ii) financial investors (e.g. private equity or hedge funds) interested in large portfolio deals with strong risk / return preference and short / medium-term perspective or (iii) strategic investors (e.g. real estate developers, hotel chains, etc.) with real estate management as their core business and interested in the development of single properties.

Real estate without upside potential should instead continue to be booked on the books of the local bank subsidiary where the defaulted loan had originated or alternatively on the books of newly founded run-down SPVs.

Development SPVs and, if founded, run-down SPVs are established with the sole intention to be the legal vehicle for the transfer and disposal of properties, meaning that they should not bear a dedicated staffing pool and they should be closed as soon as their portfolio of distressed real estate assets has been sold. According to zeb approach, a fully-fledged real estate management organization (cf. figure 2), with a clear separation of tasks and responsibilities across functions and a specialized line of staffing, should in fact be designed within the existing bank organization, to ensure a strong governance over distressed real estate management strategies and processes.

Based on best practices observed during past project experiences, an effective real estate asset management organization should consist of a central unit established at group level and of local servicing units established in the individual countries with a significant portfolio of distressed real estate assets. The main responsibility of the central unit is to steer the entire real estate collateral management organization (e.g. approve investment budget, define strategies, supervise local units, etc.) and to report to the management board of the banking group. Local units are instead responsible for the operational management of the portfolios of distressed real estate assets, applying comprehensive know-how and an established network in the local market. Local units provide indeed the most typical real estate management services such as portfolio management (e.g. property valuation, portfolio analysis, real estate asset selection, etc.) and, in case of properties already repossessed, property management (e.g. vendor management, property maintenance, etc.) and asset management (e.g. tenant management, investor search, etc.).

Figure 2: Target real estate asset management organization

Figure 2: Target real estate asset management organizationConclusions: the contribution of an effective real estate asset management organization to the bank business results

Endangered by difficult market outlooks, with volatile real estate market prices and increasing ratios of non-performing loans, banks could benefit from the setup of a specialized organization dedicated to the management of distressed real estate assets. Besides bringing in a more transparent and effective approach to deal with distressed real estate assets (e.g. for real estate valuation, real estate management, real estate exit strategy definition, etc.), such an organization could also help to improve the business and financial results of the bank. On the one hand by supporting all kinds of distressed real estate management strategies, a well functioning internal real estate asset management organization could contribute to a consistent reduction of non-performing loans. On the other hand, depending on the specific composition of the portfolio of distressed real estate assets (e.g. high share of upside potential properties), real estate management strategies could even generate an additional profit line for the bank, based on the rental income from repossessed properties and on the successful future sale of properties at a mark-up price. It goes without saying that these strategies should represent a secondary business model for the bank and that a specific share of entrepreneurial risk should always be considered as the development of real estate markets heavily depends on the overall economic outlook of the respective countries.