Key Topics

I. State of the banking industry

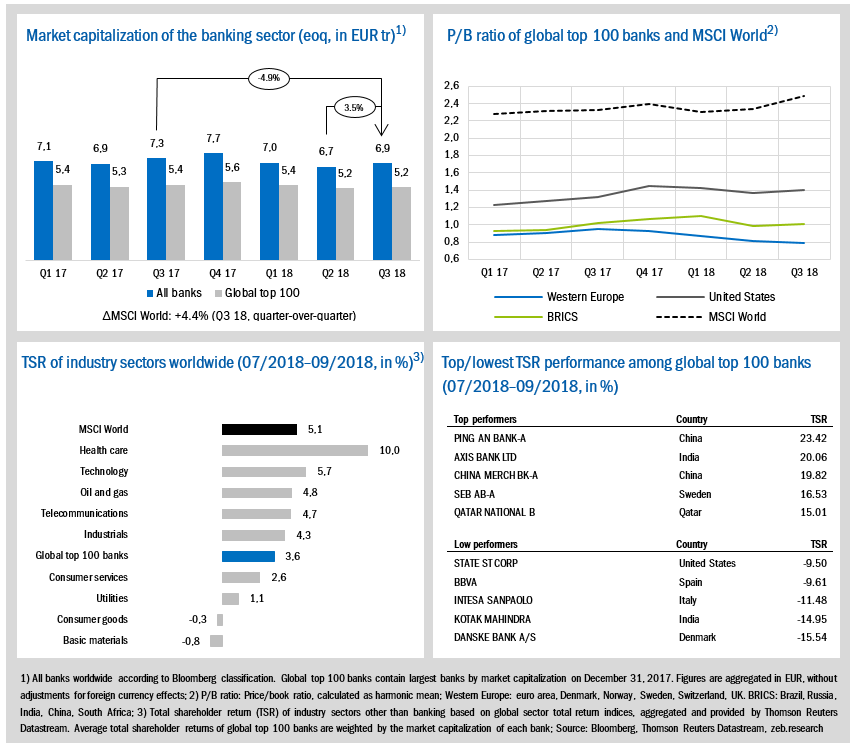

- Market capitalization of global top 100 banks without considerable improvements—with EUR 5.2 trillion remaining on its low Q2 level.

- Average P/B ratios of Western European banks fell below 0.8x in Q3 (-0.16x yoy)—a two-year low. Their TSR performance was also significantly worse (-1.0%) than that of the global top 100 banks (+3.6%).

II. Economic environment and key banking drivers

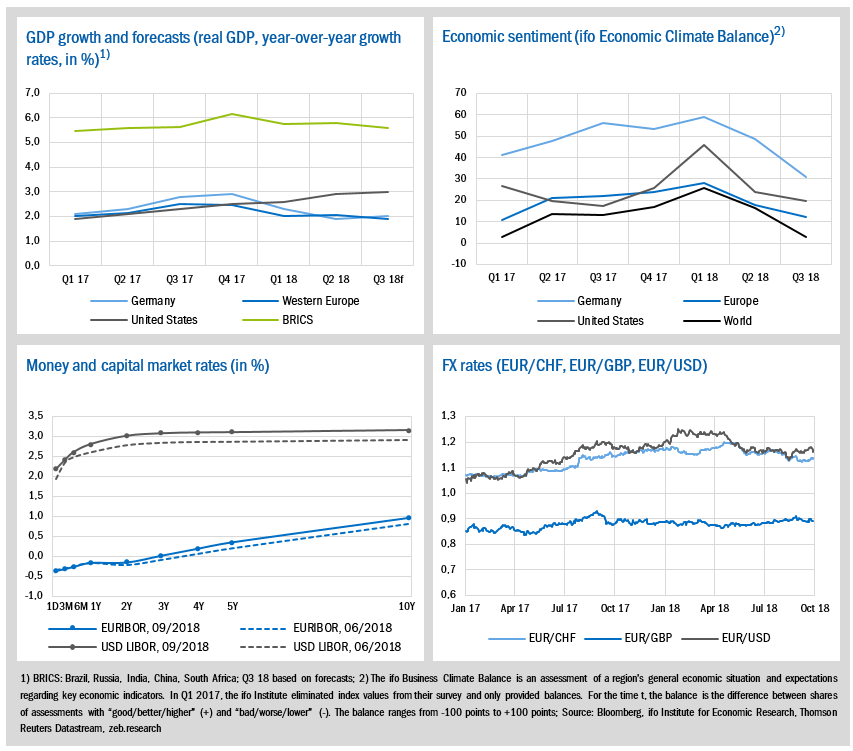

- As expected and communicated before, the U.S. Fed increased interest rates to 2.25% on September 26. In contrast, the ECB did not change its rates, thus leading to a further widening of the U.S. and European yield gap.

- The 1pp GDP growth gap between Western European countries and the U.S. (2% and 3%, respectively) persists—additionally, the economic sentiment deteriorates further.

III. Special topic: Changing structures of major stock market indices—European banks losing ground

- The exclusion of Deutsche Bank from the Euro Stoxx 50 and Commerzbank from the DAX questions the importance of traditional banks.

- Banks’ index weights in the DAX and Euro Stoxx have reduced by around 7.4pp since 2006—analysis shows that this is fundamentally driven.

I. State of the banking industry

In the third quarter of 2018, the global top 100 banks showed no considerable improvements in terms of market capitalization (+1.2% qoq, -3.6% yoy). In contrast, market capitalization of the entire banking industry increased on a quarter-over-quarter basis (+3.5%) but also trailed behind previous year’s values (-4.9%).

- From a regional perspective, average P/B ratios of European banks declined further and fell below 0.8x in Q3 (-0.16x yoy)—a two-year low. P/B ratios of BRICS and U.S. banks’ remained virtually unchanged and stayed around 1.0x (BRICS) and 1.4x (U.S.). Meanwhile, MSCI Worlds’ P/B ratio rose to an eleven-year high of 2.5x (+0.15x qoq).

- TSR of global top 100 banks was positive in Q3 2018 (+3.6%), but fell short in comparison to market performance (MSCI World: +5.1%). Western European banks performed significantly worse with -1.0%.

- BRICS banks outperformed the market with a TSR plus of 6.4%. Again, the top three performers are from China and India. The poor performance of Western European banks is reflected in finding three of them among the TSR low performers.

II. Economic environment and key banking drivers

For the third time this year on September 26, the Fed increased U.S. interest rates by 0.25pp to now 2.25%. The change was communicated well in advance and was thus expected by market participants. Hence, the EUR/USD exchange rate was unaffected but the yield curve was still elevated. Fed’s fourth and final rate increase this year is planned for December.

- Expected GDP growth remained fairly stable across all regions in Q3—the U.S. with almost 3% and Western Europe as well as Germany with around 2%. Correspondingly, the 1pp GDP growth gap between Western European countries and the U.S. persists.

- In Q3, the global economic sentiment continued to deteriorate with Germany exhibiting the sharpest decline of -17.9 balance points—realizing the lowest value since Q3 2016. After a relatively steady increase in all regions until Q1 2018, the sentiment deteriorated in the last two quarters, indicating lower growth rates in the future.

- Once again, the ECB decided to maintain key interest rates at their current low levels and communicated to keep them like this at least throughout the summer of 2019. The monthly purchases of the QE program will be reduced from

EUR 30 billion to EUR 15 billion in Q4 2018 and are expected to end then. While the 1-year EURIBOR rates remained almost unchanged, the 10-year rates reacted with a shift upwards, increasing the spread by +13.7bp. - Exchange rates of the euro against the USD, GBP and the CHF remained relatively stable in Q3. On a quarter-over-quarter basis the euro lost -2.2% against the CHF and -0.5% against the USD while it gained +0.7% against the GBP.

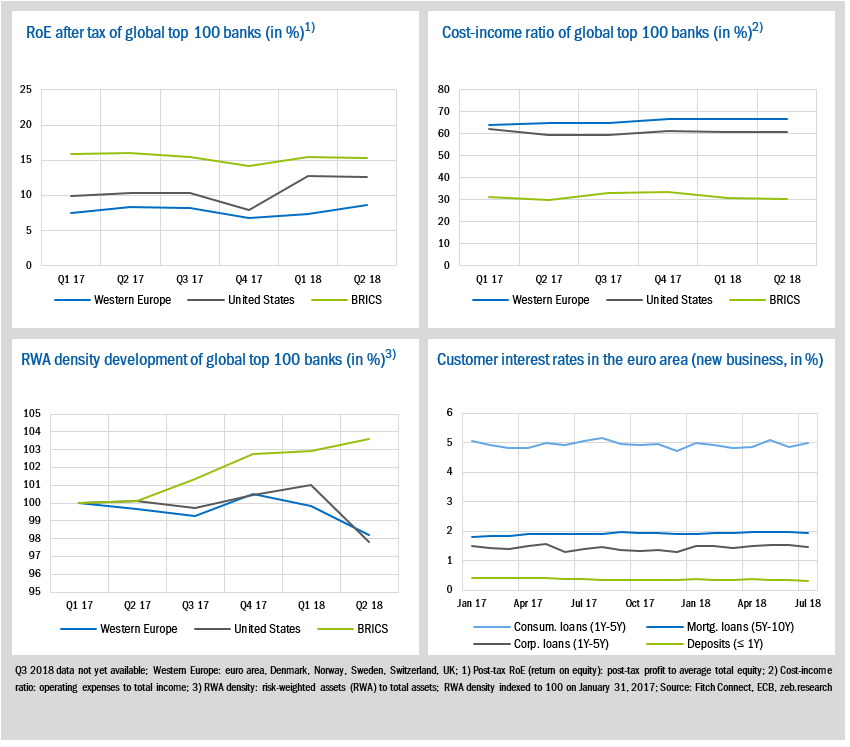

In Q2 2018, U.S. banks were able to replicate their strong average post-tax RoE of 12.7% which they had already achieved in Q1. While BRICS banks’ average post-tax RoE slightly dropped to 15.3% (-0.8pp yoy), European banks were able to increase it to 8.6% (+0.3pp yoy) and thus slightly reduce the gap to the other two regions.

- A closer look at the European banks reveals that their slightly positive development of average post-tax RoE was mainly driven by UK (Q2 18: 7.8%, +1.8pp yoy) and Swedish banks (Q2 18: 14.5%, +2.7pp yoy). The four Swedish banks within the sample leveraged the good results into a solid TSR performance with values above +12%. The five UK banks, in contrast, posted a negative TSR (ranging from -1.6% to -7.9%) as their good profitability figures were overshadowed by recurring BREXIT issues.

- Consumer loan yields in the euro area are back up again at around 5%, whereas mortgage loans, corporate loans and deposits remained at similar levels in comparison to Q1.

III. Special topic

Changing structures of major stock market indices — European banks losing ground

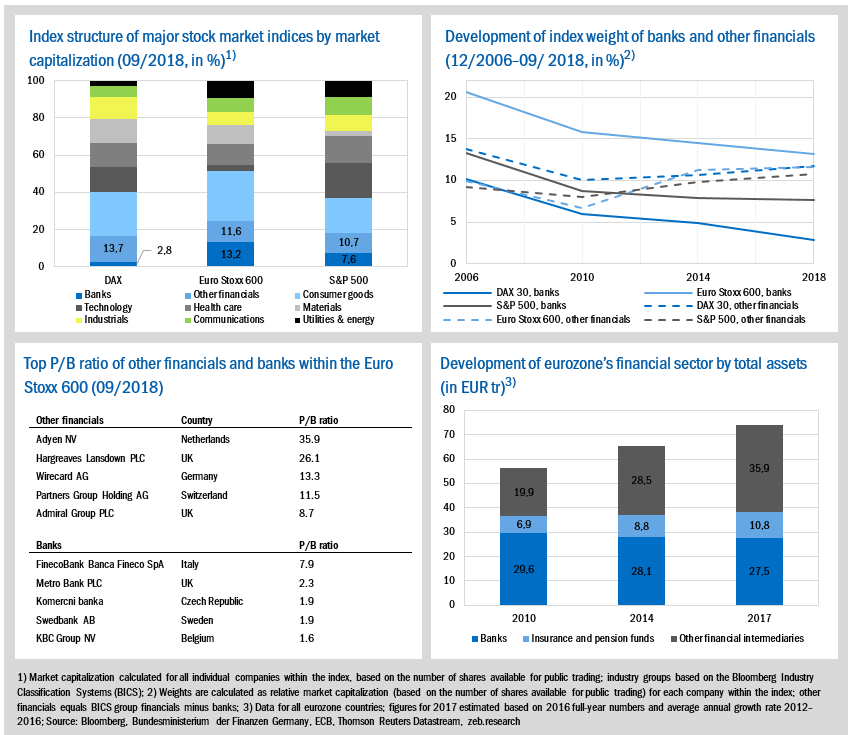

At the beginning of September, Deutsche Bank has been removed from the European Euro Stoxx 50 stock index after a 20-year membership. A few days later, the review of the German DAX 30 led to the exclusion of Commerzbank—a founding member of the index—in favor of the financial services provider Wirecard. For some market participants this is an indication of a decreasing importance of the traditional banking industry and a proceeding disintermediation. Are traditional banks really losing importance or is it just a subjective and regional snapshot?

Based on the analysis of the current structure of the three indices, the banking sector within the Euro Stoxx 600 accounts for 13.2% of the index’s market capitalization. Banks such as HSBC, Royal Bank of Scotland, Barclays and Nordea therefore represent the second largest industry group within this European index. For the S&P 500, the aggregated weight of banks—including JP Morgan, Bank of America or Citigroup—in the entire stock market index accounts for 7.6% while the share of banks of the DAX is just 2.8% (Deutsche Bank and Commerzbank[1]). The total financial services sector—as the sum of banks and other financials—makes up 16.5% (DAX) to 24.8% (Euro Stoxx) of the complete benchmark indices. Other financial institutions are mainly insurance companies, payment service providers but also private equity firms and other financial services providers such as stock exchanges.

The evaluation the historical development of the index weights in the considered indices reveals that banks have lost significance within the three stock market indices over the last 12 years. Compared to the pre-crisis year 2006, banks’ index weights in the DAX and Euro Stoxx reduced by around 7.4pp and banks’ index weights in the S&P reduced by 5.6pp. However, while banks’ weights in the DAX and the Euro Stoxx show a negative trend since 2006, banks within the S&P 500 were able to stabilize their weights and therefore their significance in the U.S. capital market in recent times. On the contrary, despite the sharp drop in line with the financial crisis, index weights of other financial institutions increased again across all indices. For the U.S. as well as the European index, other financial institutions even gained importance with +1.7pp and +1.5pp compared to 2006. Solely for the DAX, the latter were not able to return to the pre-crisis value (-2.0pp).

The diminishing role of traditional banks in Europe can also be determined by analyzing the development of the total market share of the eurozone’s financial sector. In 2010, banks’ total assets accounted for EUR 29.6 trillion, which is around 53% of EUR 56.4 trillion total market assets. Other financial intermediaries such as money market funds, hedge funds, real estate funds, equity funds, venture capital corporations or financial vehicle corporations accounted for 35% of the market, and insurance and pension funds accounted for the remaining 12%. By 2017, the situation had changed radically. Since the financial crisis, banks have been receding within the financial sector whereas the share of the non-bank financial sector has been steadily increasing. Although the market had grown to EUR 74.2 trillion, banks’ market share had dropped back to just 37%, while insurance and pension funds had expanded their share to nearly 15% due to net money inflows and rising valuations. However, the real winners are the other financial intermediaries, such as shadow banks and other non-banks, who now hold almost 50% of the assets in the European financial sector.

To summarize, European banks need to find solutions to the problem of a decreasing capital market valuation, melting market share and proceeding disintermediation. Depending on their management capability, history and legacy as well as skills and strengths, banks have different strategic options. For example, consolidation on a national basis can be a viable option for certain players. Contrary to this, mergers between large European banks still face various obstacles such as differences in legal and regulatory environments, customer behavior and structural aspects. Compared to national mergers and acquisitions, economies of scale and scope are harder to achieve on a European basis. Similarly, banks that are able to afford substantial investments and are prepared to carry potential risks can profit from creating or participating in digital financial ecosystems to foster future growth and a higher capital market valuation. However, this option will also be only successful for a subset of banks. For further insights and discussions regarding these strategic options for the European banking industry see the zeb European Banking Study 2018.