State of the banking industry

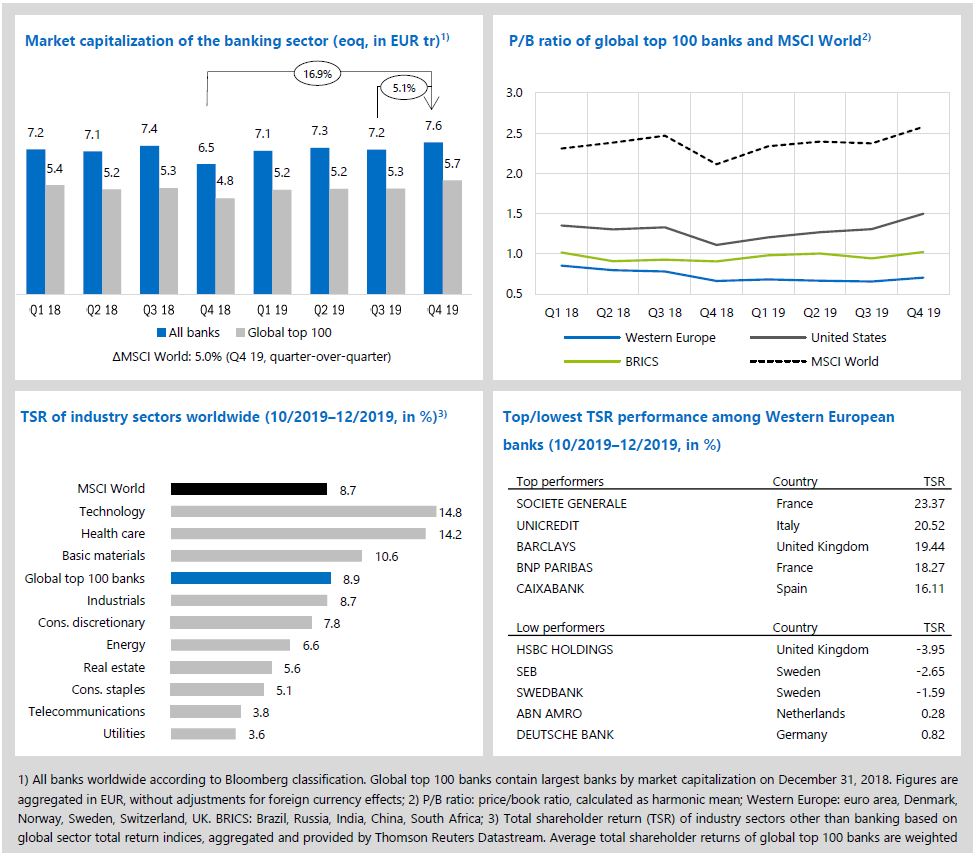

- Global top 100 banks outperformed the also very well performing global market in Q4 2019—market cap improved by +7.8% qoq and the TSR by +8.9% qoq.

- P/B ratios improved across all regions, with U.S. banks seeing the highest increase (+0.19x) and finishing Q4 with a ratio of 1.50x. Western European banks ended their downward trend and improved to 0.71x (+0.05x).

Against the backdrop of a global economic downturn, uncertainty and geopolitical tensions, global stock markets had another strong quarter in Q4 2019 (MSCI World market capitalization +5.0% qoq, total shareholder return +8.7% qoq). The global banking industry performed even better, ending 2019 with the highest market capitalization since the financial crisis 2008—all banks’ market cap inclined by +5.1% and the largest 100 banks saw an increase of +7.8% to EUR 5.7 tr. Global top 100 banks’ total shareholder return (TSR) stood at +8.9%—even outperforming the MSCI World and most other industry sectors.

- Market capitalization of global top 100 banks clearly improved and “outperformed” the global market making up some of the lost ground from the last three quarters of stagnating values.

- For 2019, overall average TSR on top 100 banks stood strong at +23.8% yoy—but still lacking behind MSCI World: +28.4% yoy.

- Average P/B ratios clearly improved across all regional clusters. P/B ratios of U.S. banks reached a new high at 1.50x (+0.19x in Q4) and BRICS banks are once again above the important hurdle of 1.00x with 1.02x (+0.08x in Q4). Western European banks improved as well to 0.71x at the end of 2019 (+0.05x in Q4).

- French SocGen had the best TSR performance among Western European banks—significant progress in the overhaul of their balance sheet was well perceived by capital markets. HSBC topped the low performers with a negative TSR of -3.95%—presented Q3 net profits were way below analysts’ expectations and communication regarding significant impairments and restructuring charges that will pressure subsequent results was assessed critically by capital markets.

Economic environment and key banking drivers

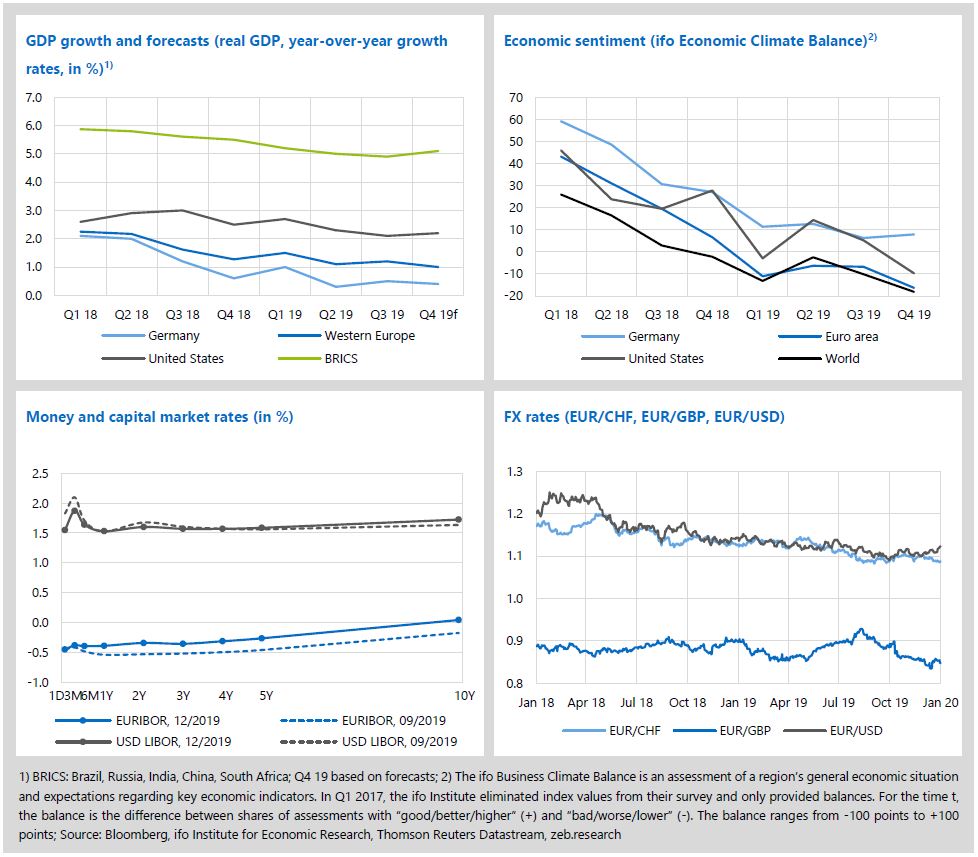

- In Q4 2019, ongoing geopolitical tensions and global uncertainty continued to suppress economic growth and caused a deterioration of the economic sentiment across all regions.

- The U.S. Federal Reserve responded with the third reduction of the federal funds rate this year to 1.50–1.75% on October 30.

- Fundamental key performance indicators of global banks are not withstanding the downturn anymore as banks’ profitability dropped across all regions.

The economic environment banks are operating in remained difficult in Q4 2019. Economic growth is slowing further in Germany and Western Europe, while the U.S. and BRICS are seeing minor improvements against particularly low growth figures in Q3 2019. These developments are in line with a deterioration of the economic sentiment in the World, the U.S. and euro area. The U.S. Federal Reserve responded with the third reduction of the federal funds rate this year, announcing that this will likely be the last rate decrease for a longer period as long as no material reassessment is required. The ECB kept its deposit facility rate at -0.50%. Capital market yields slighlty recovered in the euro area with a minor shift upwards—U.S. market yields remained basically flat.

- The overall assessment of the current economic climate is now clearly negative in the World (-18.1), euro area (-16.3) as well as the U.S. (-9.7) which saw the largest drop with -14.9 balance points in Q4 2019.

- Despite minor improvements of the yield curves in Q4 2019, the situation today is still significantly more challenging than one year ago. At the end of December 2019, the yield curve in the euro area is significantly lower and flatter than one year ago, with the 1Y rate at -0.39% (Q4 2018: -0.25%) and the 10Y rate at 0.04% (Q3 2019: 0.76%). The current U.S. yield curve remained as flat as at the end of 2018 but shifted downwards by around 100bp during 2019.

- Increased certainty around Brexit boosted the GBP against the euro in Q4 2019—EUR/GBP dropped by -4.2% qoq to 0.85. Regarding the USD the EUR managed to gain 3.0% qoq and stood at 1.12 at the end of 2019. EUR/CHF ended its downward trend and remained basically on the same level as at the end of Q3 2019.

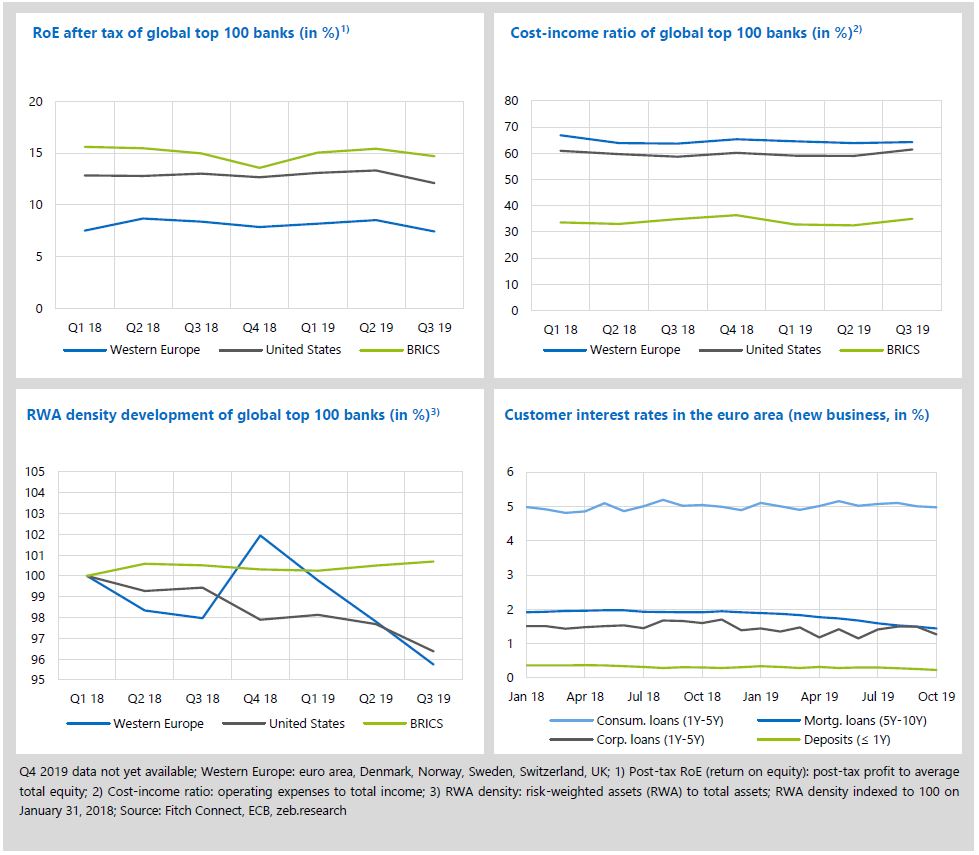

Fundamental banking KPIs were able to withstand the negative economic environment over the first six months of 2019 but finally started to decline in Q3. As a result of the ongoing economic deterioration and a slumping global investment banking with strongly declining deal volumes and earnings, banks’ profitability dropped across all regions. US banks achieved the worst result in the last two years and in Europe, after some improvements in the past, banking profits declined once again.

- With regard to profitability, US banks achieved a two-year low post-tax RoE of 12.1% in Q3 2019 (after 13.3% in Q2 2019 and 13.0% in Q3 2018). In Europe, the profits dropped again significantly leading to a post-tax RoE of just 7.4%. Based on current analyst forecasts, European banks’ post-tax RoE for the full year 2019 will be around 6-7% indicating a further drop of banking results in the fourth quarter.

- In Europe, the relatively moderate increase of the average cost-income ratio (compared to the large RoE drop) from 63.9% to 64.3% indicates that the lower results are driven by both, operative and non-operative effects. Looking at individual results, especially some of the larger players (in terms of total assets) like Barclays, Lloyds, Nordea or Deutsche Bank achieved lower Q3 results due to declining banking earnings (e.g. in the investment banking and corporate business) but also some special individual factors like write-offs and restructuring costs.

- The flattening of the European yield curve during the first months of 2019 is also further reflected in the development of euro area customer rates. Especially, the average interest rate for mortgage loans (5Y-10Y—which was more or less fixed at 2% over the last 3.5 years—decreased further in Q3 2019 and is now down to just 1.44% (-47bp yoy).

Special topic: Climate change and its impacts on banking

Initial thoughts

- Whether through a disruptive transition process or devastating physical impacts, climate change will have a huge effect on the global economy and banks.

- For banks, the biggest short-term challenge will be the ability to measure, simulate, assess and disclose climate change-related risks.

- More importantly, however, climate change affects customer demands and triggers significant funding needs, providing business opportunities for pro-active banks with a clear strategy

Looking back at the decade that ended only a few days ago, with all its turns, twists and turmoil, there is one meta topic that was dominating the political, social and economic discussions: climate change. In fact, the current question is not if the climate is already changing or if it will change further in the future, the real question is literally, how severe the climate change will be. Against this background, what will be the impact or consequences on banks and the required actions for this industry?

Average global temperature has increased by around 0.8° celsius since 1880—with two-thirds of the warming having occurred since 1975. Projections of future global emission pathways show that a temperature increase of around 2.0° celsius (relative to 1861–1880) until 2100 is almost inevitable. The required level of change of the world-wide economy to stay even below this 2.0° celsius requires significant technological breakthroughs, changes in social behavior and policies and would come with extreme transitional disruptions across nearly all industries. In a “business-as-usual” scenario, without any substantial actions by humankind, however, increases of 4.0-6.0° celsius are also possible. This would then lead to severe physical impacts on the environment, including more regular and extreme weather events as well as long-term shifts in climate patterns, again with far-reaching implications to the economy.

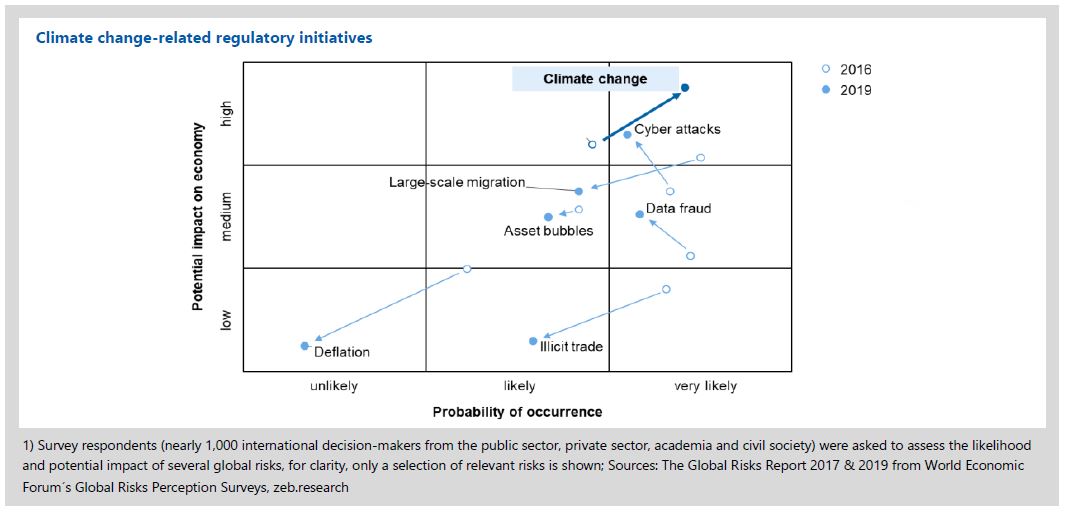

No matter which emission pathway will finally be realized, the impacts and risks related to climate change and its mitigation are enormous. This is also acknowledged by the results of the World Economic Forum’s Global Risks Perception Surveys, defining climate change as the number one threat in terms of both, impact and likelihood. Already in 2016, they show that climate change was perceived as an issue with a high-impact potential. The assessed likelihood of climate change as a real threat, however, has increased significantly in the last three years and is now ahead of other highly relevant risks suchs as “cyber attacks”, “data fraud” and “large-scale migration” (see the figure below).

For the banking sector, climate change entails a wide range of challenges. Physical and transitional risks impact banks directly and, even more importantly, indirectly via transmission channels as well as through propagating second round effects from the economy to banks and vice versa. In the end, all typical bank risks (credit, market and operational) will be impacted in some way by climate change-related risks. Banks should therefore be able to assess these risks to manage them properly. The distinctive features of risks related to climate change, however, pose a significant challenge in this regard. While there is certainty about some occurrence of climate change-related risks in the long run, exact outcomes and timings are unknown. Additionally, the risks are far-reaching in scope and magnitude, non-linear, correlated and irreversible.

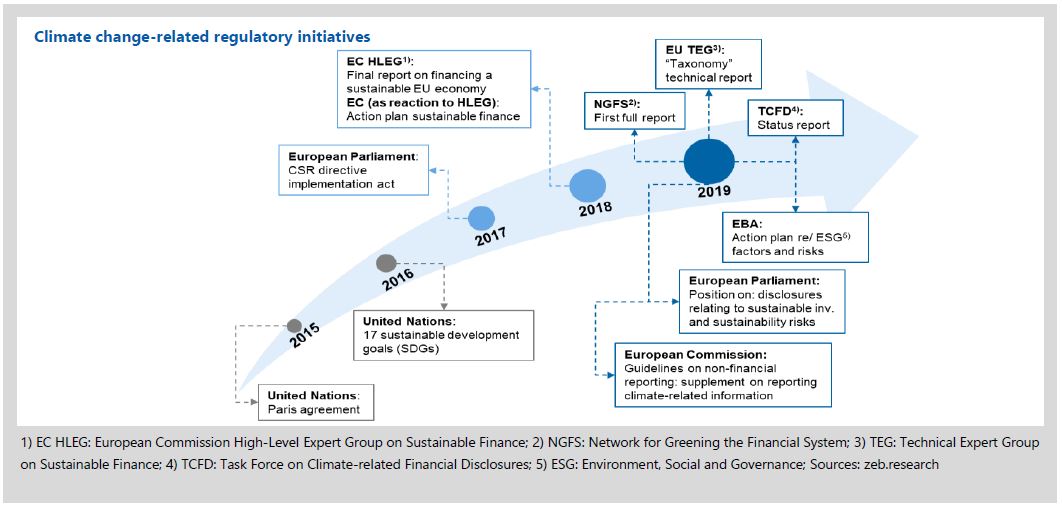

Another challenge is created by regulators and policy makers that significantly heightend their interest regarding the effects climate change has on the banking sector. 2019 demonstrated a new level of focus by regulators, with many different and increasingly specific initatives launched (see the figure below). Their plans to introduce new regulatory reporting requirements, stress tests and potentially even new capital requirements point towards significant additional regulatory costs for banks in the future. From a regulatory point of view, the current focus of banks should be to identify, measure and evaluate climate change-related risks and to include these risks into business and risk strategies. In a next step, quantitative evaluations of risks through scenario analyses and stress tests will probably be expected and executed by regulators.

All in all, the far-reaching impacts of climate change-related risks combined with the increased interest of regulators and high likelihood of future reporting, stress test and potentially even capital requirements, highlight the new fields of action for banks. Given the essential importance of the underlying topic, the fundamental question from our perspective is not “if” but rather “when” banks will have to measure, simulate and disclose climate change-related risks and its impacts on their business model, loan portfolio or performance indicators in the future. Banks have to address these issues rather soon.

Currently, the public discussions about climate change and the role of banks in it, are very much focused on these short-term “must haves”. However, from our perspective, climate change has a very important additional dimension: the possible opportunities for the banking business as such. There will be (and in some parts it is already observable) climate change-driven, fundamental changes of private and corporate customers demands and also significant funding needs of the economy to avert a global emission pathway that would lead to devastating physical impacts. Yes, this leads to new risks (especially for banks that are not adjusting adequately) but more importantly, this offers new business opportunities for institutions that develop and execute a clear strategy regarding their position on climate change-related topics. The identification of industries and markets that require the most comprehensive transition as well as a clear picture regarding the own capability within this transition can provide pro-active banks with an important competitive edge. Business opportunities include not only new loans or bonds to finance the transition of the economy but affect all other business areas from savings, asset management, treasury to the capital market and M&A business. E.g. first analyses estimate that the EU economy would need EUR 175–290 bn p.a. to reach carbon neutrality until 2020.

Together with our clients, we are engaged in a broad number of projects and activities on this topic. We offer information sessions and design thinking workshops about the relevance and impacts of climate change on an institution resulting in first checklists and heatmaps. Moreover, we develop methods and concepts for risk measurement, reporting and regulatory disclosure. Last but not least, many discussions are centered around business opportunities with regards to climate change—be it investment-related or driven by funding/ financing needs. Our experts are more than happy to exchange views and experiences on this (or related topics). They are available at marketflash@zeb.de.

Stay tuned to our upcoming European Banking Study 2020 and European Insurance Study 2020 that will provide further insights.