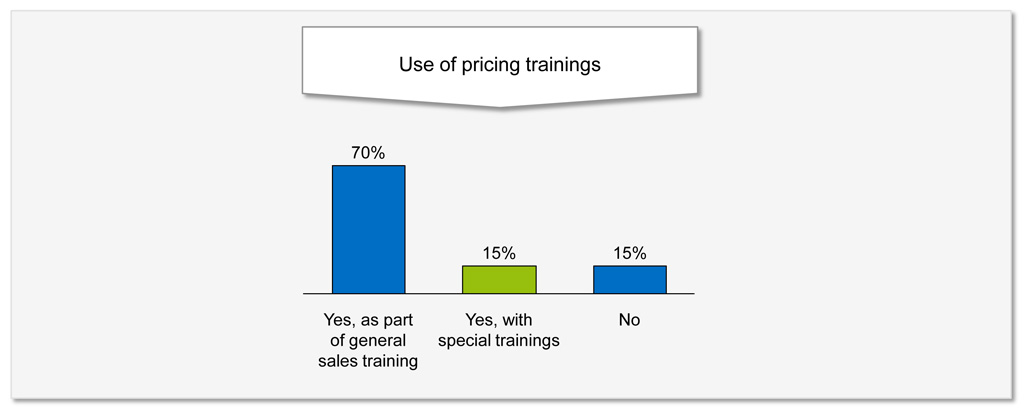

Only 15% with explicit pricing trainings

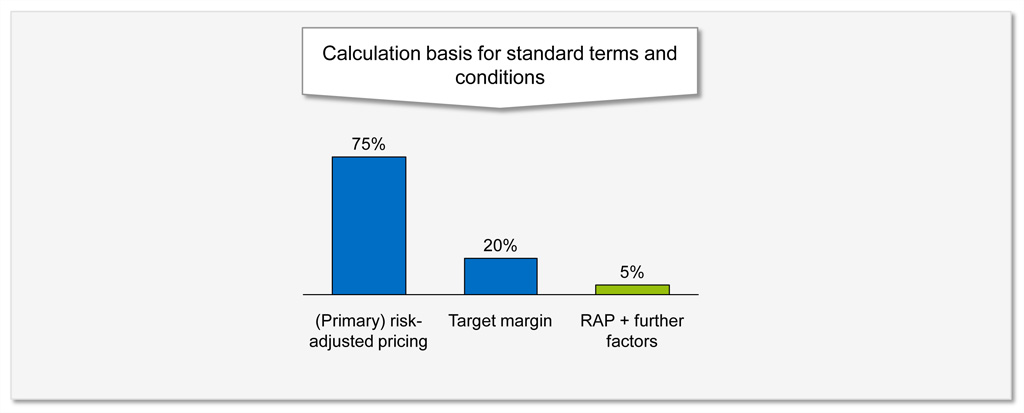

Identified risk factors and negotiating skills of the customer advisor are main drivers of these earnings. Consequently, many institutions rely on the classic methods of risk-adjusted pricing, that can be managed locally, as well as on respective trainings of the sales employees and thus on an indirect impact on financial management. Figure1 provides an overview of the probability distribution in the lending business of German banks.

Figure 1: Probability distribution of identifying standard terms and conditions

Figure 1: Probability distribution of identifying standard terms and conditionsThe status quo underlines the necessity of special attention to the topic of pricing trainings. Only 15% of banks conduct explicit pricing trainings (see figure 2).

Figure 2: Probability distribution of the use of pricing trainings

Figure 2: Probability distribution of the use of pricing trainingsShift of the pricing horizon—Integration of further criteria

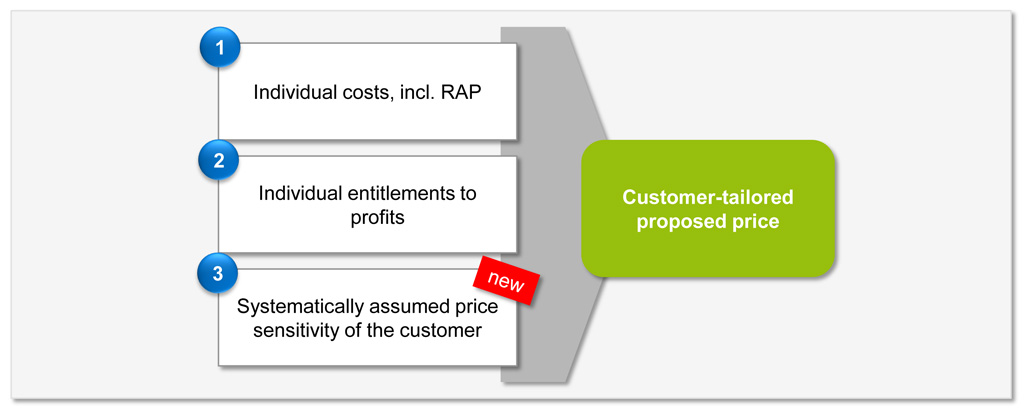

However, apart from common criteria, there are further drivers that can be examined with the help of analyses of internal and external data and (if possible) can be quantified, in order to integrate them into the pricing. For instance, systematically induced price sensitivities of customers can be integrated into pricing for optimization—in addition to individual costs and entitlements to profits—in order to present the respective willingness to pay of the customers. Thus, in addition to the costs, the business-specific price sensitivity of the customer is systematically priced in (see figure 3).

Figure 3: Procedure of identifying a customer-specific proposed price

Figure 3: Procedure of identifying a customer-specific proposed priceBetter pricing through improved data situation

Finding and using further criteria sets high requirements for the availability of respective data and capacities for analyzing and processing them. Examples are the fixed interest period, customer turnover, creditworthiness / risk class, duration of customer retention or respective level of competition within the post code area (if available via external data sources) resulting in about 25 to 30 customer, product or competition-specific features. The extent that these features “explain” a predefined margin can then be examined. This margin is to be adjusted by as many cost components / influencing variables as possible, in order to obtain a “net margin”, where in particular the creditworthiness of the customer and specific product features are priced in. Qualitative criteria, such as the price bargaining power of a customer or the possible cross selling potential are deliberately not integrated in this analysis, as they are left to the discretion and experience of the advisor.

Using a multi-method analysis as success factor

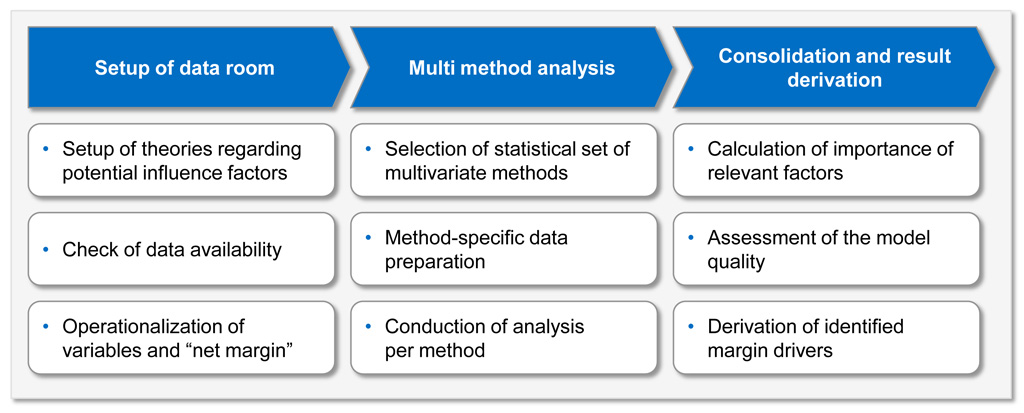

First, a multi-method data analysis is made with the result of a price indication (see figure 4), which takes all available data into consideration. The next step is feedback from sales about the extent that the proposed price is considered to be marketable. This information is methodically integrated with the help of the van-Westendorp’s analysis, which brings together all information online. After all analyses have been completed, the customer advisor can see the price proposal directly in the pre-calculation tool and decides individually, if they will offer this price proposal, will enforce a higher price or will use their preferential terms competence.

Figure 4: Analysis model for identifying margin drivers

Figure 4: Analysis model for identifying margin driversEnsuring long-term success by regular updates

In order to ensure long-term success of the described procedures, an update is to be carried out depending on new business transactions (new deals and/or extensions). Experience has shown that an update is reasonable and necessary after 250 to 300 transactions. This ensures that changes of the general price level on the credit market will be integrated into the price policy of individual banks. We know by experience that the price / margin enforcement will sustainably be improved by at least 15–20 basis points and thus justifies investments in such analyses.