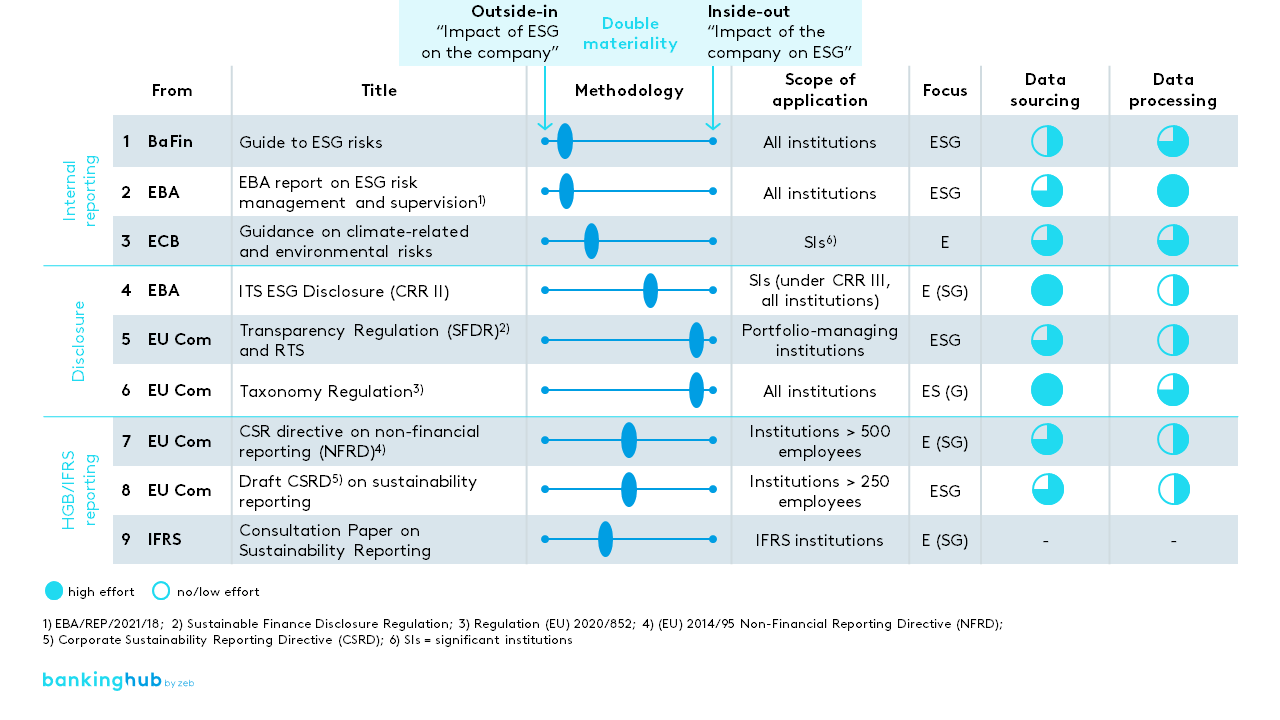

The figure provides an overview of relevant initiatives with an assessment of double materiality. The initiatives are sorted according to the above-mentioned groups “Internal reporting”, “Disclosure” and non-financial “HGB/IFRS reporting”.

In addition, indicative assessments of the effort required for data sourcing and processing both in implementation and in operation are provided.

Reporting initiatives can be categorized accordingly.

- First, initiatives focusing on the reporting of ESG aspects in banking operations (e.g. BaFin Guidance Notice, ECB Guidance and EBA Report) – these essentially take the outside-in perspective.

- Second, disclosure at the institution and product level, the majority of which takes the inside-out perspective and of which the EU Taxonomy is a well-known example. In addition, there are requirements, e.g. from the EU Commission in the context of non-financial HGB/IFRS reporting, which work towards a balanced presentation of both perspectives

Cf. EU Commission (2021) Proposal for Corporate Sustainability Reporting, COM(2021) 189 final, p. 1.