“Large-scale merger” as a buzzword moves the industry and politics in connection with the consolidation of European banks—especially in comparison to the major players from the USA and China. One of the most prominent topics in 2019 was the failed merger preparation between Deutsche Bank and Commerzbank. The topic dominated the newspapers’ headlines for weeks. The end result, however, was not a new large-scale credit institution in Germany, but the insight that this time again, for a variety of reasons, no joint “merger story” could be told.

Overview—article topics

- Bank mergers in Europe

- European banks in international comparison

- Low market integration as a barrier

- Conclusion—Large-scale mergers of European banks

Bank mergers in Europe

As the decreasing number of European banks between 2007 and 2018[1] from 6,127 to 4,600 (-2.6% p.a.) shows, strategic mergers are nevertheless a frequently used option to counter the development of the market environment[2]. However, consolidation primarily affects smaller institutions. Mergers between large banks are the exception, although the number of mergers is expected to rise.

Well-known examples of large-scale mergers in recent years:[3]

- Banca Intesa and Sanpaolo IMI merge to form Intesa Sanpaolo (2007, second largest Italian bank)

- Acquisition of Dresdner Bank by Commerzbank (2009, fourth largest German bank)

- Merger between DZ Bank and WGZ Bank (2016, second largest German bank)

By jointly optimising established business models, mergers of large banks contribute to the improvement of customer satisfaction, but they can also be triggered by politically bailout deals or the controlled establishment of powerful economic players. The importance of the aforementioned economic factor in particular correlates strongly with the size of banks in a market.

In any case,the focus of this article is not restricted to the German banking market, due to the fact that many large European banks have never really recovered since the financial crisis. They are at risk of becoming less important due to continuing weak earnings and outdated IT infrastructures in the increasing competition with Asian and American banks as well as fintechs, captives etc. In particular, there is the question of whether bank consolidation towards “national champions” or even “EU champions” is necessary to ensure a stable supply of financial services to the economic area.

The German economy with its clear focus on exports needs banks with an international network, access to global capital market structures and highly competitive financial services[4]. In order to finance continuous growth, for example of DAX 30 companies, there is a need for banks whose balance sheet, capitalization and organization allow for a diverse offering and large volumes for derivatives, loans or other transactions at a competitive speed and pricing.

European banks in international comparison

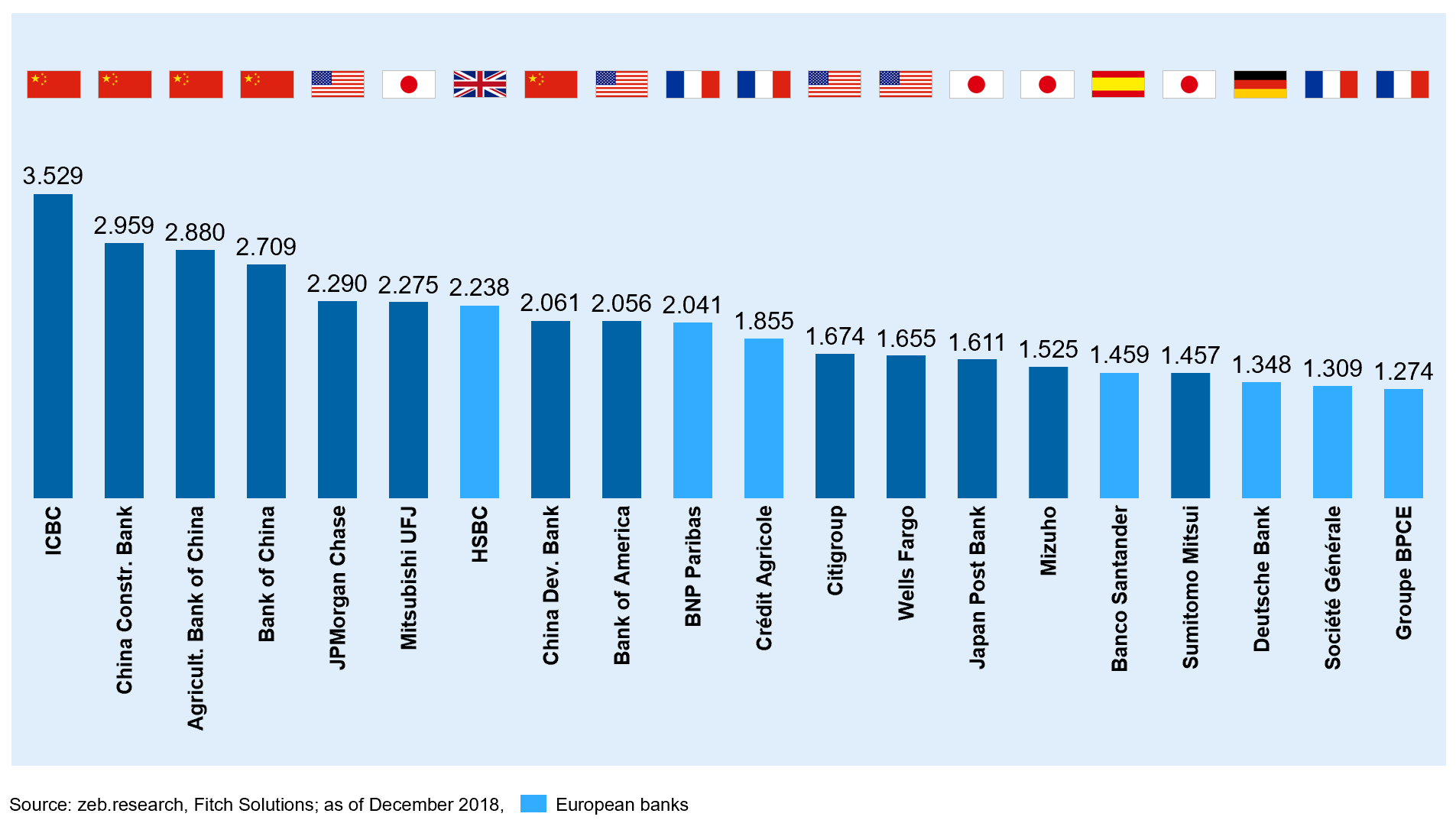

In terms of total assets, Chinese banks are by far the world’s leading banks—four of the five largest banks are based in China. Only seven European banks are among the top 20 banks, of which only two make it into the top 10. Deutsche Bank is the only German representative ranking in 18th place.

Figure 1: Overview of the 20 largest banks worldwide in 2018 (by balance sheet total in EUR bn)

Figure 1: Overview of the 20 largest banks worldwide in 2018 (by balance sheet total in EUR bn)In this comparison, European banks are usually not only smaller but also less profitable. Chinese banks and large US institutions in particular are generating returns on equity above 10%, while European institutions are still at a much lower level. Almost ten years after the financial crisis they have averaged 7.2% in 2018[5]. Large German banks are comparatively small and not very profitable.

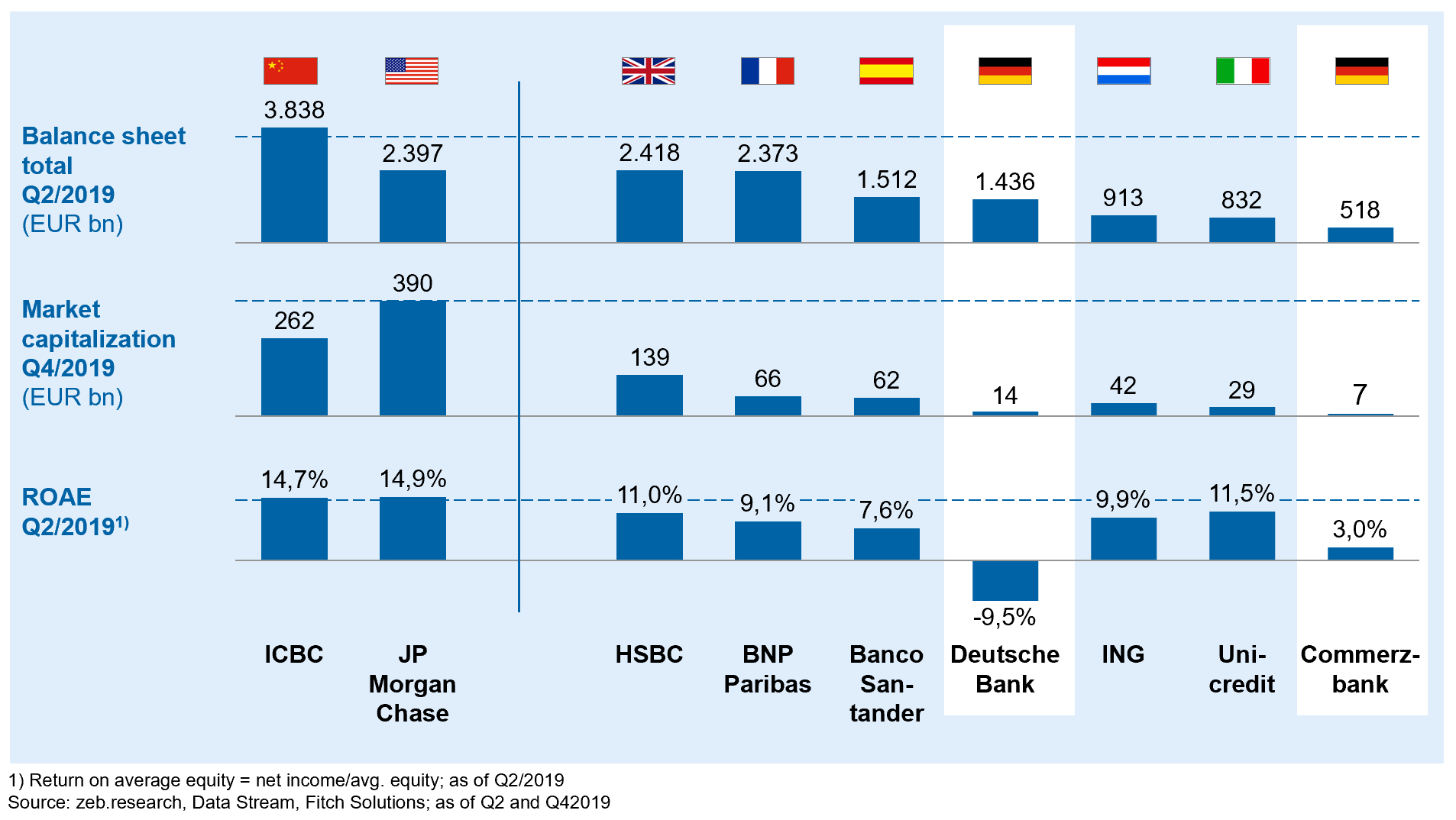

Figure 2: Profitability of selected large banks with total assets of over EUR 400 m in 2018

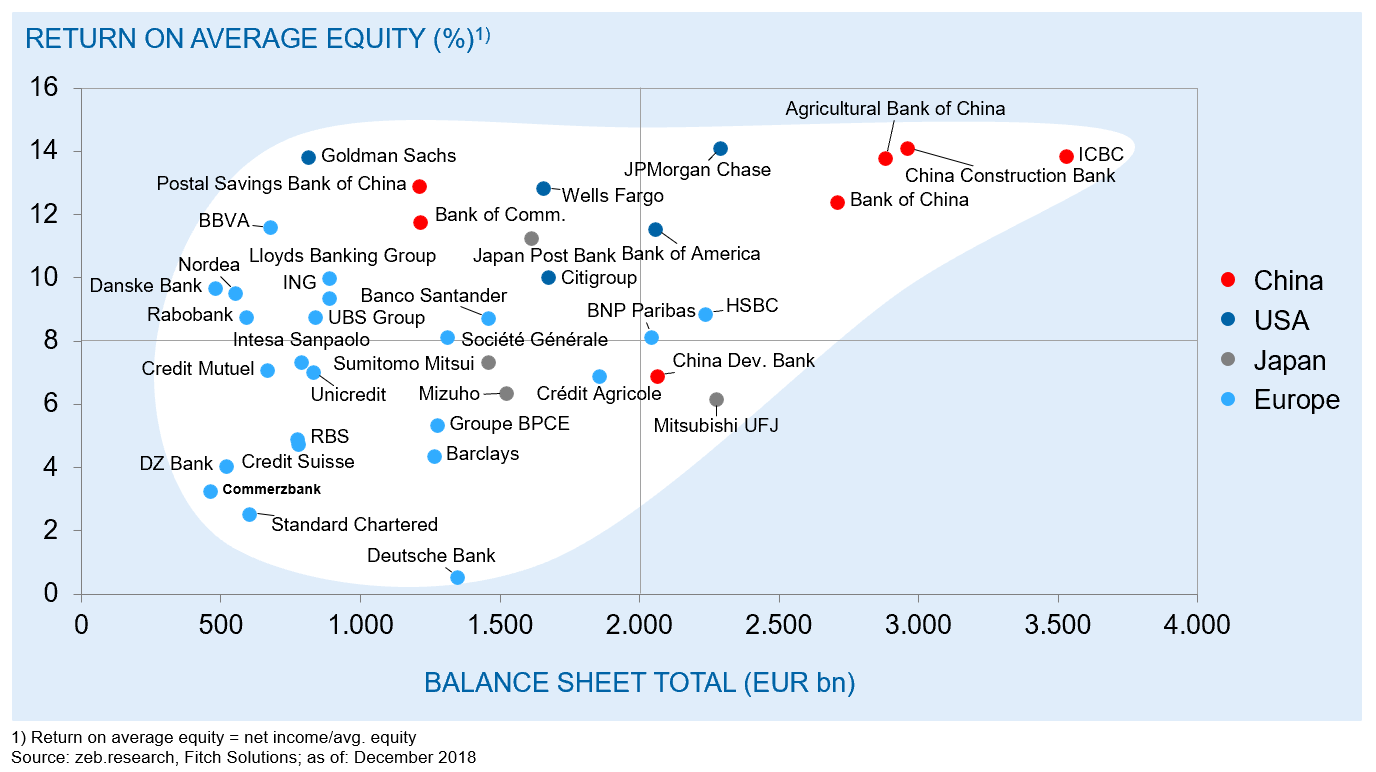

Figure 2: Profitability of selected large banks with total assets of over EUR 400 m in 2018Looking at individual banks, the differences between Europe, China and the USA become even more tangible. The market capitalization and return on average equity of European banks are significantly below those of selected institutions from China and the USA—with large German banks at the bottom of the league.

Figure 3: Selected banks in comparison

Figure 3: Selected banks in comparisonWhile China states the largest banks, US institutions are characterized by high profitability. The size of Chinese institutions is also due to the strong economic growth and state involvement. Large US banks have undergone a wave of consolidation following the financial crisis and have gained economic strength in the end.[6] Considering the comparison, a stronger consolidation of the market could also be expected in Europe.

Low market integration as a barrier

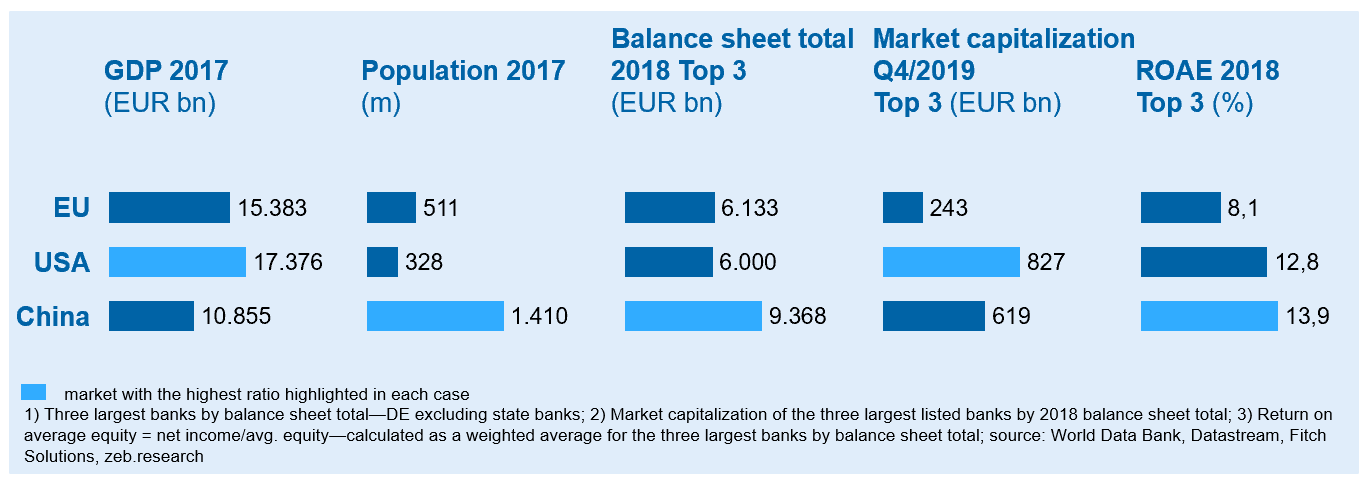

Market integration allows banks to operate freely within the entire market without legal or technical barriers and thus has a direct positive impact on production costs. As an economic area, the EU is roughly on a comparable level with the USA and China.[7] However, the European banking market differs significantly regarding the integration of financial services.

The USA offer a highly integrated domestic market with almost 330 million inhabitants and the strongest economy in the world. CChina also represents an integrated market. The currently second-largest economy, with a population of around 1.4 billion, still is exhibiting huge potential. In the EU, some 510 million inhabitants are spread across 28 individual countries with major economic, linguistic, cultural and also legal differences.

Figure 4: Banking markets in comparison

Figure 4: Banking markets in comparisonIn contrast to the almost completely free exchange of goods and most services within the EU, financial services are often regulated separately by region. Although all large European banks are subject to ECB and EBA supervision, national regulations—especially at product level or with regard to data or consumer protection—remain significantly different. Passporting[8] does not completely remove these barriers, although it does make it easier for banks to open branches in other EU countries or provide their services across borders.

Products and processes can only be standardized to a limited extent. Even liquidity and capital surpluses in individual countries can only be used to a limited extent in order to provide bank customers at group level with capital in a flexible and cost-effective manner where it is needed.

If a bank conducts cross-European business with a larger volume of business in individual countries, it usually maintains full-service banks as subsidiaries.[9] This limits synergies through cross-border business expansion and reduces the efficiencies on a European level. A large bank in the USA or China, on the other hand, can reach a significantly larger number of customers without being split into several companies and duplicating individual functions.

Some banks are attempting to leverage cross-border synergies in business operations, at least at technical level. One possibility is to have a unified IT platform, such as those Banco Santander or ING operate for their European companies. Such efforts can still be significantly ramped up. Nevertheless, our project experience shows that in these cases the different requirements of the individual countries can also generate considerable additional effort.

There is no unanimous opinion at political level on cross-European bank mergers as a solution. The ECB, the German Banking Association and individual representatives of the financial sector repeatedly call for the establishment of cross-European banks. On the other hand, Felix Hufeld, President at BaFin, for example, warned against cross-border bank mergers. The formation of “European champions” is not in the interest of BaFin.[10] Nevertheless, he sees a trend towards consolidation, but would like to leave its assessment to the market.[11]

Conclusion—Large-scale mergers of European banks

Banks around the world face a variety of challenges. At the same time, European banks in particular are in a significantly more challenging position than banks in the USA or China. A major reason for this, apart from extremely low interest rates, is the lack of genuine market integration. In addition to the often still existing bank-specific legacies, it makes significant synergies in cross-European mergers more difficult.

In Europe, large German banks in particular must significantly improve their competitiveness at almost all levels in order to be part of the leading players again. Mergers can also be an effective (strategic) option to overcome internal problems that have not yet been solved as part of a thorough new beginning. However, this requires a clear integration strategy that is designed and implemented from the customer to the IT.

In addition, the individual national states have a political preference for their own large banks with international significance—this was also evident in the public discussion about Deutsche Bank and Commerzbank and possible acquisitions of Commerzbank by foreign competitors.

In our view, three key factors are therefore essential for cross-border mergers of large banks:

- Further integration of the European banking market, through greater harmonization of prudential regulation, strengthening of the capital markets union and the creation of truly uniform rules on consumer and data protection

- Reduction of political skepticism as well as focus on individual states towards a sincere European economic policy—especially as a counterweight to the USA and Asian markets, such as China

- Effectively master individual legacy-challenges of each large bank and enhancing sharpening of the respective strategic profiles as a basis for viable equity story of a merger with regard to customers, employees, owners and supervisory authorities

If all the aforementioned factors are addressed in more effectively way, we expect an increasing number of large-scale bank mergers in Europe. This could lead to the rise of cross-European banks to new “global champions”—in any case, this would be an appropriate reflection of the importance of the European economic area.

[1] Cf. credit institution statistics of the ECB

[2] These include increasing regulatory requirements, historically low interest rates, ongoing digitalization and new competitors (e.g. fintechs)

[3] Market positions by 2018 balance sheet total

[4] British HSBC or American Citigroup, for example, offer such a service to global companies

[5] Cf. zeb European Banking Study 2018

[6] For example, acquisition of Bear Stearns and Washington Mutual by JPMorgan Chase in 2008, Merrill Lynch by Bank of America in 2009

[7] Although China is currently lagging behind in terms of its gross domestic product, it has significantly more inhabitants and is currently growing much faster

[8] Passporting basically allows banks to conduct cross-European business without a separate license in the respective country, after an EU-wide license has been granted by the supervisory authorities in the domestic market

[9] Example: Banco Santander (Spain) with its German subsidiary Santander Consumer Bank

[10] Cf. Handelsblatt (2019): President at BaFin warns against cross-border bank mergers, May 24, 2019

[11] Cf. Wirtschaftswoche (2020): BaFin sees “undiminished” trend towards consolidation among banks