When is an investment classified as taxonomy-aligned?

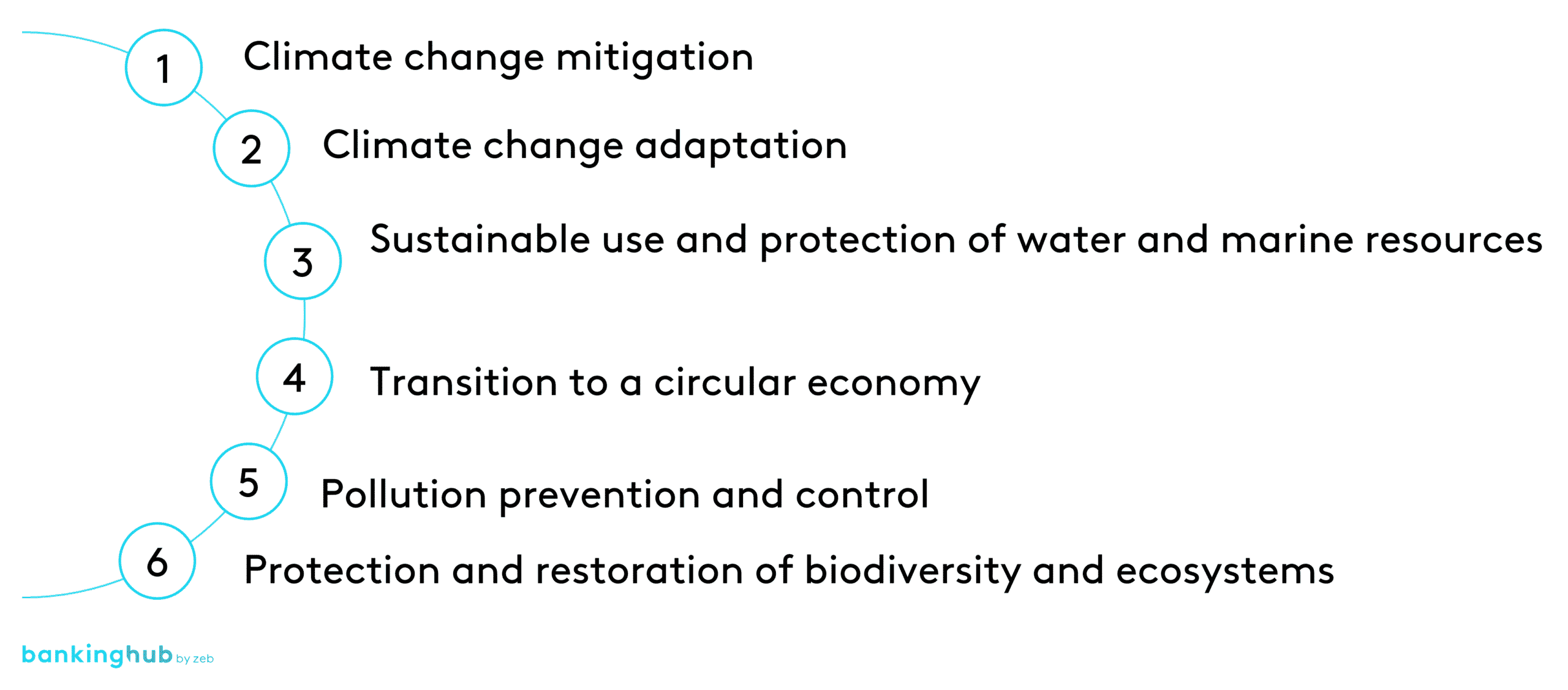

In order for an investment to be classified as taxonomy-aligned, it must have a positive impact on an environmental objective (cf. Figure 1) and at the same time not harm any other environmental objective. A minimum level of social protection defined in the Taxonomy Regulation[2] must also be observed.

The EU has drawn up a catalog of technical screening criteria that can be used to determine whether or not investments are sustainable in this sense[3]. So far, however, these are only available for the first two of a total of six environmental objectives.

Thus, the review is initially limited to assessing the fulfillment of the first two climate-related environmental objectives. Currently, the EU taxonomy is mainly relevant in the context of non-financial reporting and bank disclosures. Article 8 of the Taxonomy Regulation and the Delegated Act (EU) 2021/2178 define the content, presentation and disclosure of taxonomy-related non-financial statements. Financial undertakings must make the first mandatory disclosures as early as the 2021 fiscal year. Sustainability-related capital requirements or specific minimum ratios have not yet been provided for.

The business of automotive banks against the background of the EU taxonomy

The business of automotive banks mainly comprises sales financing for motor vehicles produced in the Group and dealer financing. The financing portfolio includes traditional loan agreements and final installment financing as well as leasing transactions.

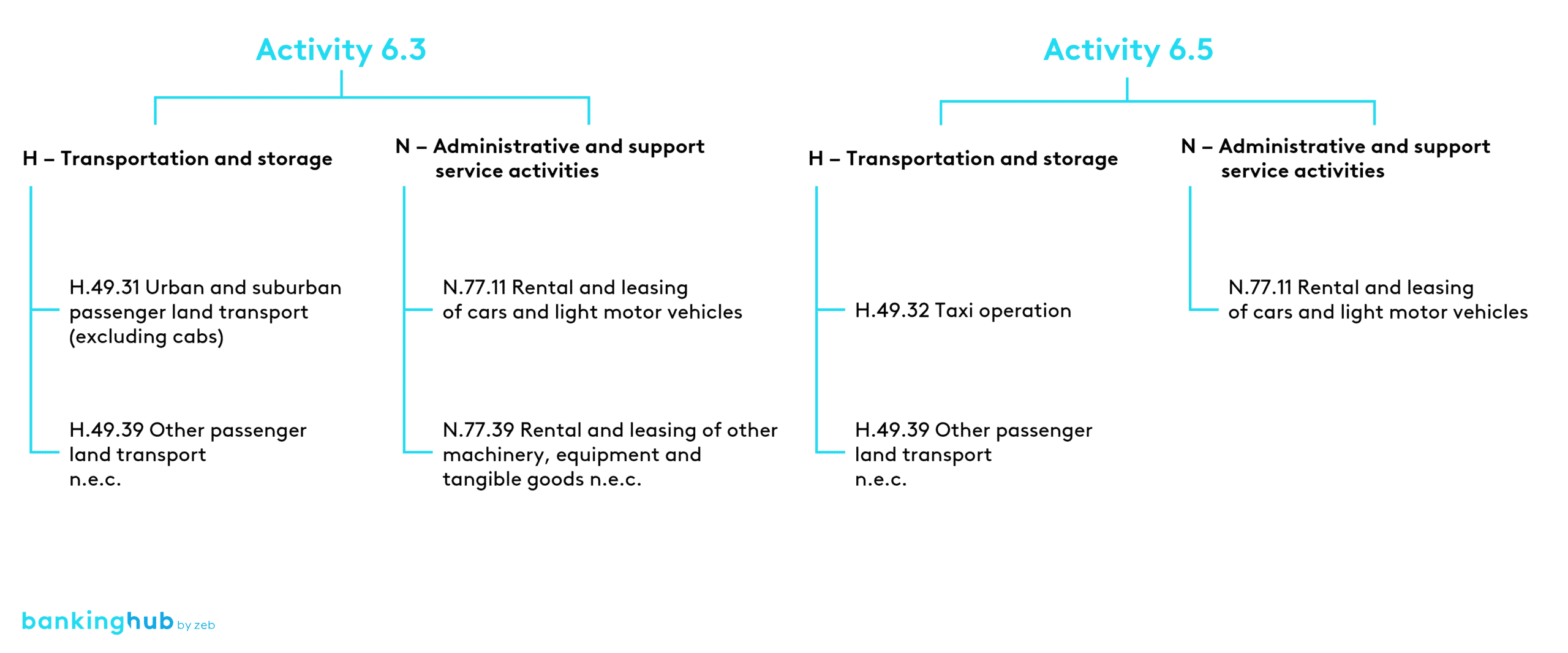

Meanwhile, the EU taxonomy already reflects the aforementioned activities of automotive banks. The focus of the taxonomy so far has tended to be on energy-intensive activities or on economic activities with “green” potential. The former include both the transport sector in general and the business of financing and leasing motor vehicles in particular. In this context, Activities 6.3 “Urban and suburban transport, road passenger transport” and 6.5 “Transport by motorbikes, passenger cars and commercial vehicles” are of particular importance for automotive banks, as they are closely linked to their core business.

Activity 6.3 describes the “Purchase, financing, leasing, rental and operation of urban and suburban transport vehicles for passengers and road passenger transport.” Activity 6.5 is described in the taxonomy as follows: “Purchase, financing, leasing and operation of vehicles designated as category M1, N1 […] or L (2- and 3-wheel vehicles and quadricycles).”

Figure 2 assigns the activities described in the taxonomy to the related economic sectors based on the NACE codes along with the respective description.

Taxonomy reporting at automotive banks

The conduct of lending and leasing business is subject to licensing within the meaning of the German Banking Act (Kreditwesengesetz – KWG). While operating leasing, which is similar to renting, can in principle also be provided without a KWG license, finance leasing business requires at least a license as a financial services institution. If, however, the company also conducts automotive lending, it needs a license as a credit institution. In this context, the automotive banks, which are usually integrated into a non-financial group, have the option of either reporting on a consolidated basis within the group or publishing a stand-alone report.

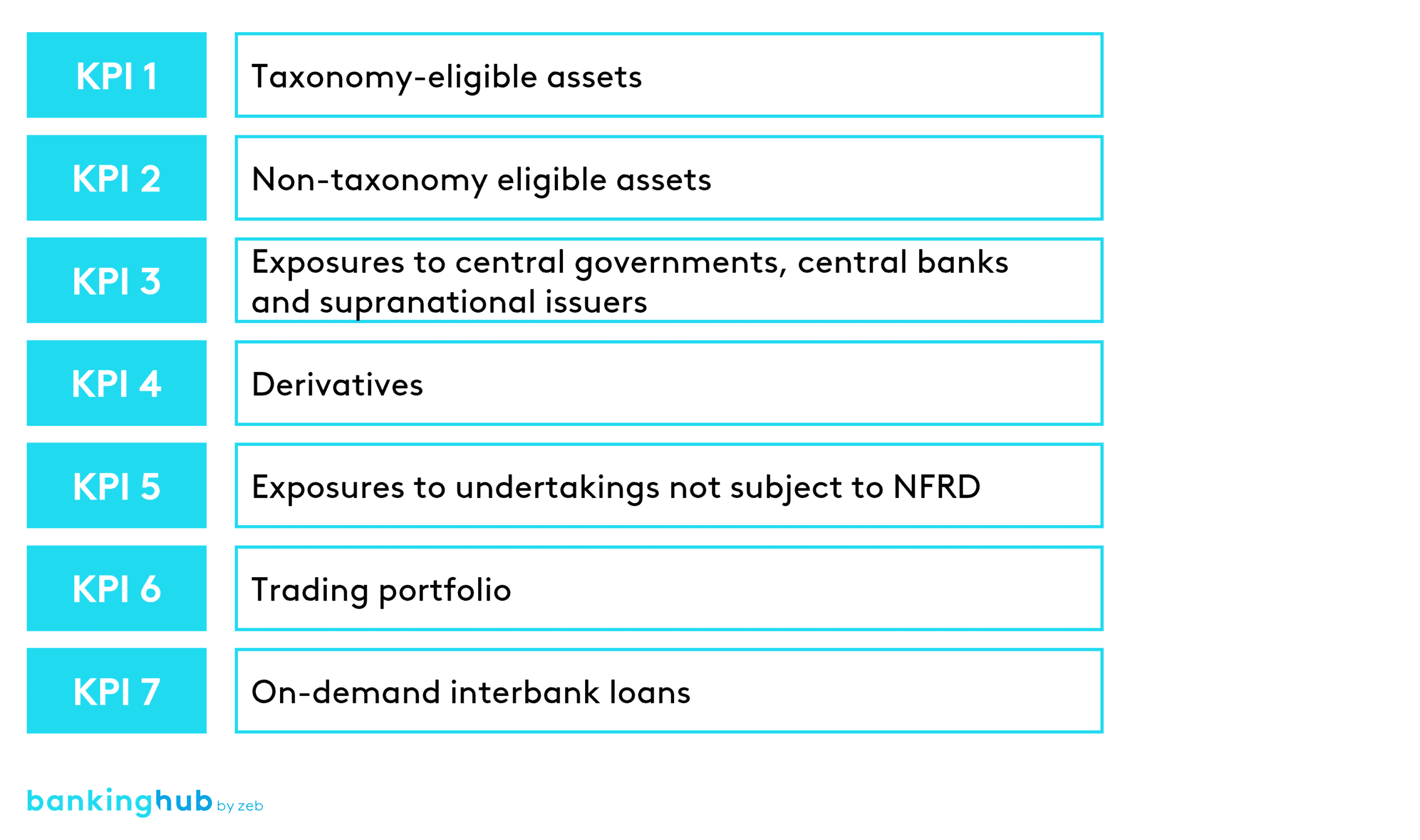

Currently, the bank is only required to report seven quantitative KPIs in the event of a stand-alone publication in accordance with Art. 8 of the EU Taxonomy Regulation. The first two KPIs provide an overview of the share of (non) taxonomy-eligible assets. In this context, retail exposures of automotive banks are included in the taxonomy-eligible assets if they underlie a taxonomy-eligible transaction.

In corporate business, only those taxonomy-eligible exposures are included for the time being that exist towards non-financial reporting entities in accordance with the NFRD [4]. Correspondingly, the second KPI includes all non-taxonomy eligible transactions.

The KPIs three to seven provide more detailed information on the share of positions classified as non-taxonomy-eligible, including the share of exposures towards non-NFRD undertakings. For calculating this fifth KPI, it is necessary to have detailed information of all counterparties of the corporate client portfolio. In particular, information is required on the number of employees, total assets, turnover, country of domicile and status as a “public interest entity”. Transactions in non-EEA countries are not taken into account.

In addition to the quantitative information, the EU taxonomy also requires qualitative information, which on the one hand describes the origin and on the other hand the scope of the data as well as the influence of the EU taxonomy on the (sustainability) strategy. In describing the influence, reference can be made both to a strategy implemented throughout the Group and to the automotive bank’s own initiatives. Furthermore, it shall be described how aspects of the taxonomy are integrated into the product design and the consulting process.

Finally, from 2023 onwards, the reporting of a Green Asset Ratio (GAR) will also be mandatory, in the context of which taxonomy alignment must also be checked. An example of a potentially taxonomy-aligned automobile is the electric vehicle, which as a so-called zero-emission vehicle (0 g Co2/km)2/km) can make a significant impact on the environmental objective of climate protection.

Special features of the KPI calculation for automotive banks

The calculation of the quantitative KPIs is based on the accounting approach and the values according to FinRep. In the context of the taxonomy, exposures towards customers are considered taxonomy-eligible in the case of automotive banks. In the case of financial institutions, on the other hand, tangible assets cannot sensibly be classified as taxonomy-eligible at present.

However, the accounting treatment of leases depends on the specific classification of the transactions, which may differ under the German Commercial Code (HGB) or IFRS. The different classification may result in different accounting treatment and disclosure either as receivables or as leased assets.

Under HGB, the accounting treatment of leases follows fiscal enactments, whereby claims arising from finance leases are accounted for as exposures. On the other hand, any other form of leasing is understood as a rental relationship in general. Consequently, accounting is also based on the standard procedure for leases under HGB.

According to HGB, operating leases are currently mostly reported under tangible assets and therefore do not qualify for taxonomy. The transfer of risks and rewards is the main criterion for classification as a finance or operating lease pursuant to IFRS. Under IFRS, it is thus possible to account for both finance and operating leases as exposure and to test them for taxonomy eligibility accordingly.

Current challenges and outlook

Automotive banks are facing a number of challenges as a result of the EU taxonomy. Like other institutions, they are currently struggling with the task of collecting data on the taxonomy eligibility of transactions and mapping it in the data warehouse. For this purpose, new data processes and responsibilities must be set up, as extensive adjustments will be necessary in the coming years in terms of data, and a high degree of flexibility is required. The gradual introduction of the taxonomy will also significantly expand the future demands on data and processes.

The introduction of a mandatory Green Asset Ratio – from fiscal year 2023 onwards – will require a large amount of product-related data on mobility solutions such as vehicles as part of the necessary alignment assessment. These include, for example, Euronorm, CO2 emissions or the recyclability of materials. The additional data must be mapped in the data warehouse at an early stage, and the processes for obtaining the data must be created. In the context of sales financing, early communication with the manufacturer is particularly important. In addition, measurable criteria are to be published in 2023 for the other four environmental objectives as well[5]. This expands the review of economic activities to include all environmental objectives, which will further increase data needs.

A specific challenge for automotive banks arises from the different treatment of lease receivables and leased assets in taxonomy reporting. The aim is to achieve comparable treatment of leasing transactions irrespective of the specific legal form of the contract and the accounting standard. This can be achieved by working closely with associations to develop best practices and by regularly exchanging information with supervisory authorities and legislative bodies. Otherwise, if taxonomic inequality persists, automotive banks will have to ask themselves whether a changed design of the leasing business or a switch to IFRS accounting would be beneficial in order to meet the taxonomic KPI requirements.

Conclusion: EU taxonomy for automotive banks

The core business of automotive banks is already included in the EU taxonomy and can therefore be classified as a potentially sustainable business. The prerequisite is the fulfillment of the dedicated criteria of the EU. At the same time, automotive banks are already facing special requirements. In addition to the well-known challenges in the areas of data and processes, a number of regulatory issues remain unresolved, especially in the leasing business.

Currently, different accounting approaches and frameworks used result in enormous deviations in the eligible activities. The goal should be to achieve a taxonomy-aligned result that leads to a comparable outcome regardless of the chosen accounting approach.

While the scope of reporting for fiscal year 2022 is largely unchanged, fiscal year 2023 will see the introduction of the Green Asset Ratio and thus a taxonomy alignment review. In addition, a continuous development of the EU taxonomy is already foreseeable. For automotive banks, this means that further adjustments to the data warehouse and processes will be necessary in order to be able to react flexibly to new regulations and publication obligations.