FORBEARANCE: BASICS ON THE SUBJECT

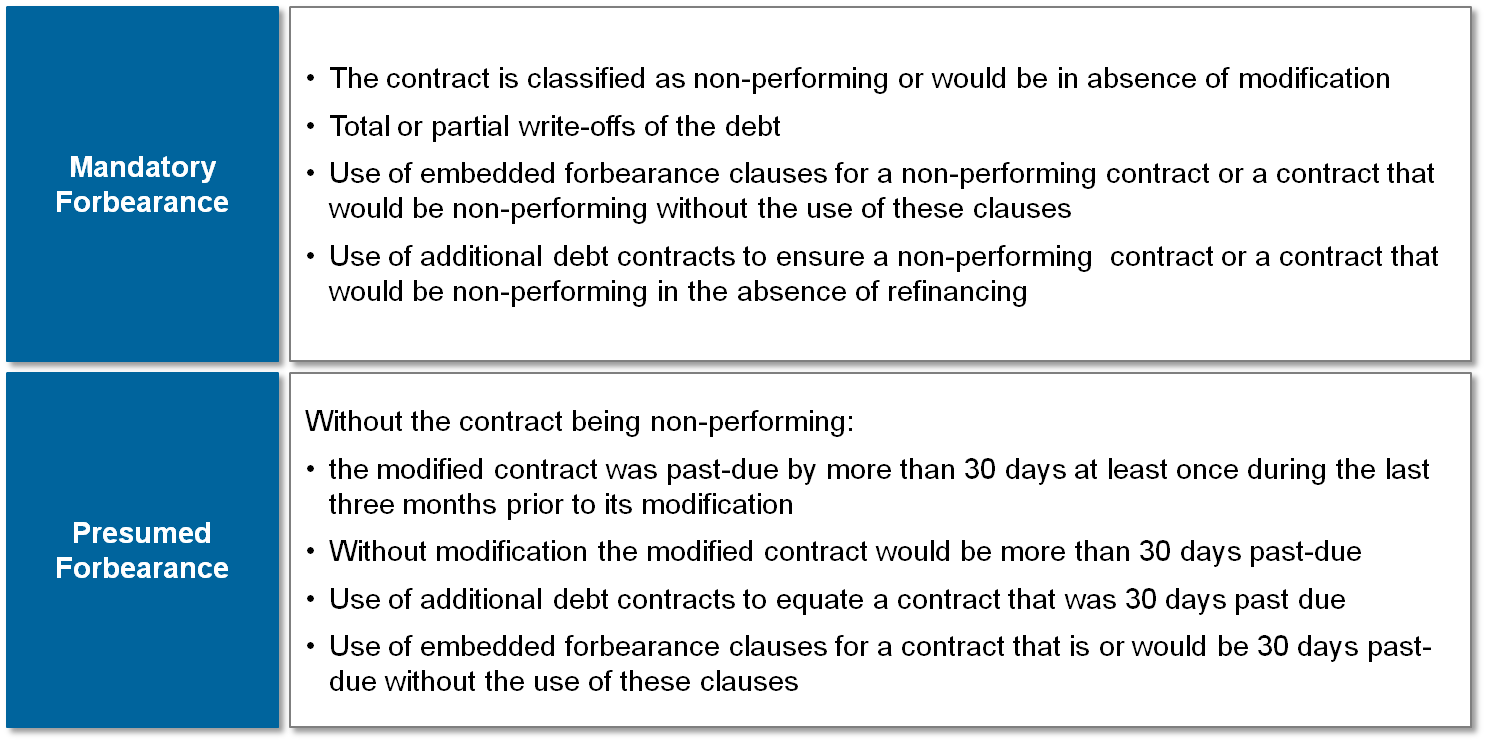

Pursuant to EBA/ITS/2013/03, forbearance is given if:

- a debtor cannot fulfill his contractual obligations due to financial difficulties and

- the contractual terms are then changed in a way that the debtor regains the ability to fulfill his obligations or if the contract is fully or partially refinanced/restructured

In this context, it is also possible that rights included in the contract already upon its conclusion (so-called embedded forbearance clauses), which allow the debtor to change the terms of the loan contract, can lead to circumstances in which forbearance is given. In the course of the review, pursuant to ITS a distinction is made between “mandatory” forbearance and “presumed” forbearance, which can be rebutted by the institution.

Figure 1: Criteria for the identification of forbearance

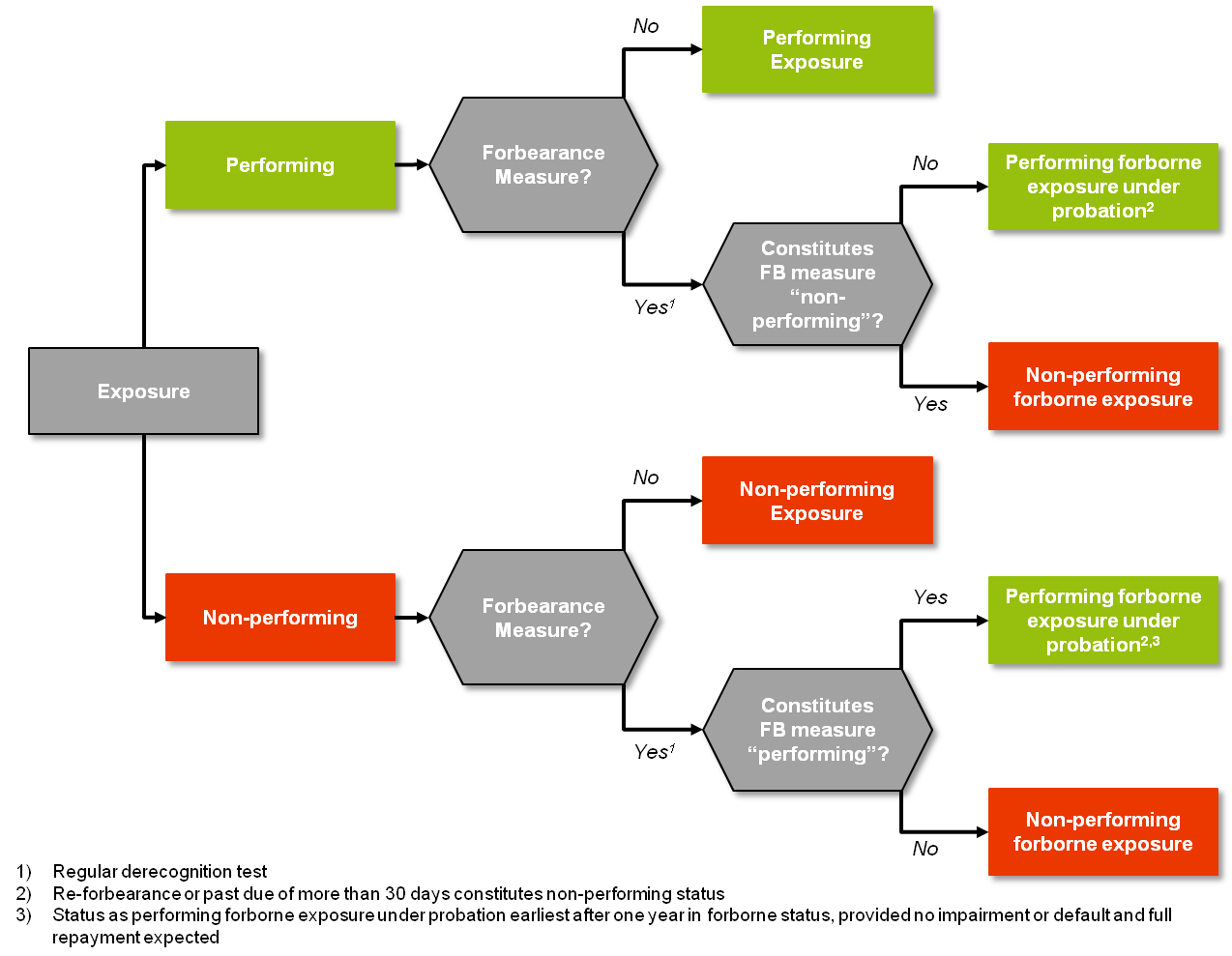

Figure 1: Criteria for the identification of forbearanceBorrowers who have been classified as “forborne” are subject to special monitoring regulations and have to be marked accordingly. For the forbearance status to be lifted, exposures that were classified as “forborne” in the previous period have to cumulatively fulfill the following “exit criteria” (this review has to be conducted at least quarterly):

- the exposure is classified as “performing”

- a probation period of at least two years since the classification as a performing exposure has been completed successfully

- a not insignificant proportion of interest and redemption payments was made at least during half of the probation period

- at the end of the probation period, none of the debtor’s exposures is more than 30 days overdue

In the context of the EBA ITS / FINREP requirements, specific review frameworks have to be implemented, which have to be applied in the identification of forbearance triggers / the forbearance measures implementation. Various review criteria have to be taken into account, as illustrated in the decision tree below:

Figure 2: Categorization of “forborne” loan exposures

Figure 2: Categorization of “forborne” loan exposuresFORBEARANCE: PRACTICAL CHALLENGES

In practice, the implementation of the forbearance requirements proves to be challenging and brings about the following tasks, amongst others:

- Developing a system for the automatic identification and marking of “forborne” exposures and for the periodic execution of derecognition tests

- Checking the availability of the required markers in the data base and, if applicable, adding further data fields

- Implementing processes for monitoring “forborne” exposures incl. a review of the probation periods and all classification criteria

- Harmonizing the forbearance procedure with the balance sheet-related risk provision processes / impairment, especially with a view to conducting impairment tests

- Considering the embedding of the “forborne” marker as an impairment trigger pursuant to IAS 39 and harmonizing the forbearance procedure with the new expected loss / expected lifetime loss-based impairment model under IFRS 9 at an early stage

- Reviewing the product portfolio with a view to embedded forbearance clauses

- General necessity to implement harmonized credit and accounting processes, IT architectures and data data warehouses

With a view to the first remittance date – December 31, 2014 – there is only a relatively short period of time left to complete the full implementation of forbearance reporting requirements. In the light of the given time constraints, many institutions implement interim solutions for the first reporting. However, according to the assessment of zeb, in the medium term the implementation of powerful, integrated target solutions will be required in order to ensure an efficient and high-quality regulatory reporting on a permanent basis.