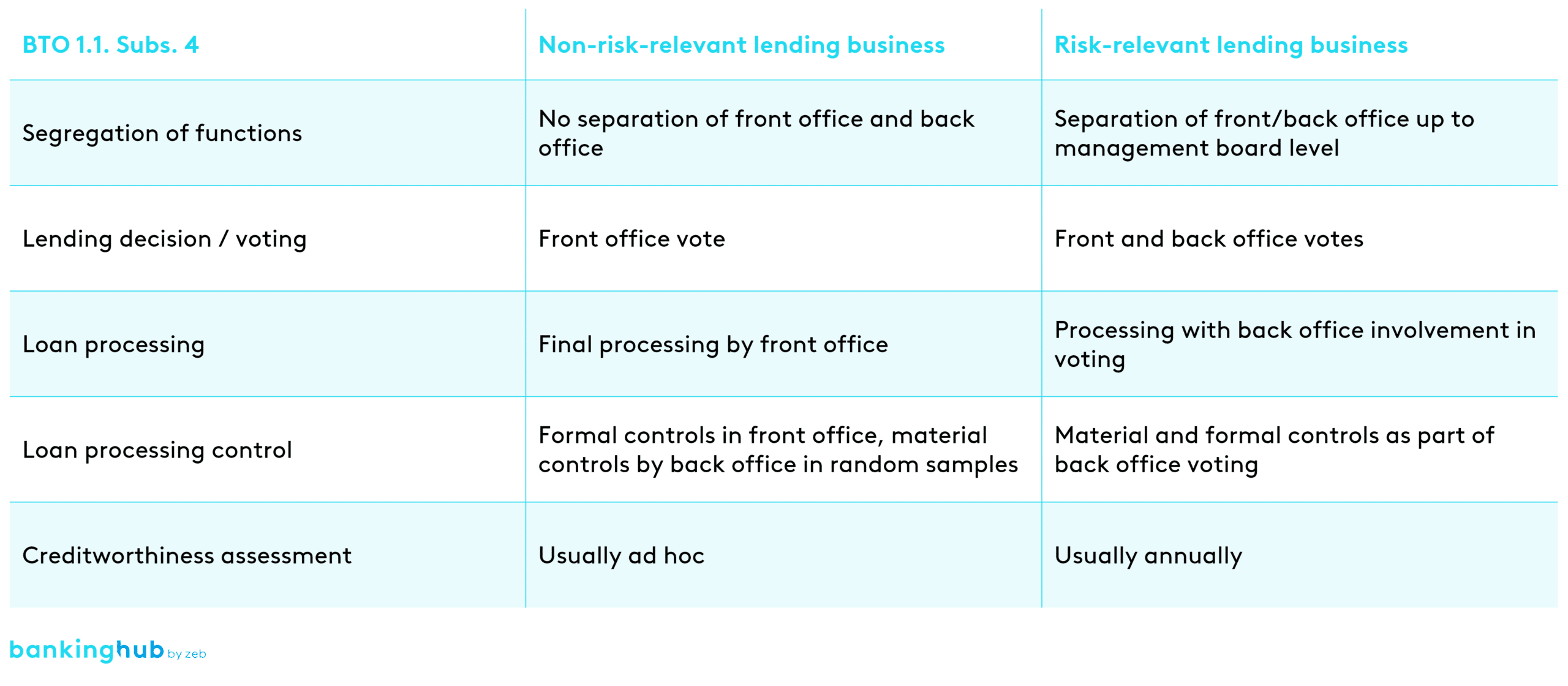

Activities according to their risk relevance

Audit-proof derivation of the threshold

Determining the risk relevance threshold is not a trivial matter, as there are no clear guidelines for defining the criteria. Each institution must establish its own threshold based on its loan portfolio and risk culture. This derivation is often the subject of external audits (annual audits and special inspections), which is why extensive documentation and justification are required.

An important aspect in the determination is the distribution of risk above and below the defined threshold. In practice, very high rates of 80% to 90% of the risk tend to be attributable to risk-relevant credit exposures. However, the threshold set is often lower than it could be from a risk-oriented perspective, which is due to a lower risk appetite or a need for security on the part of the management.

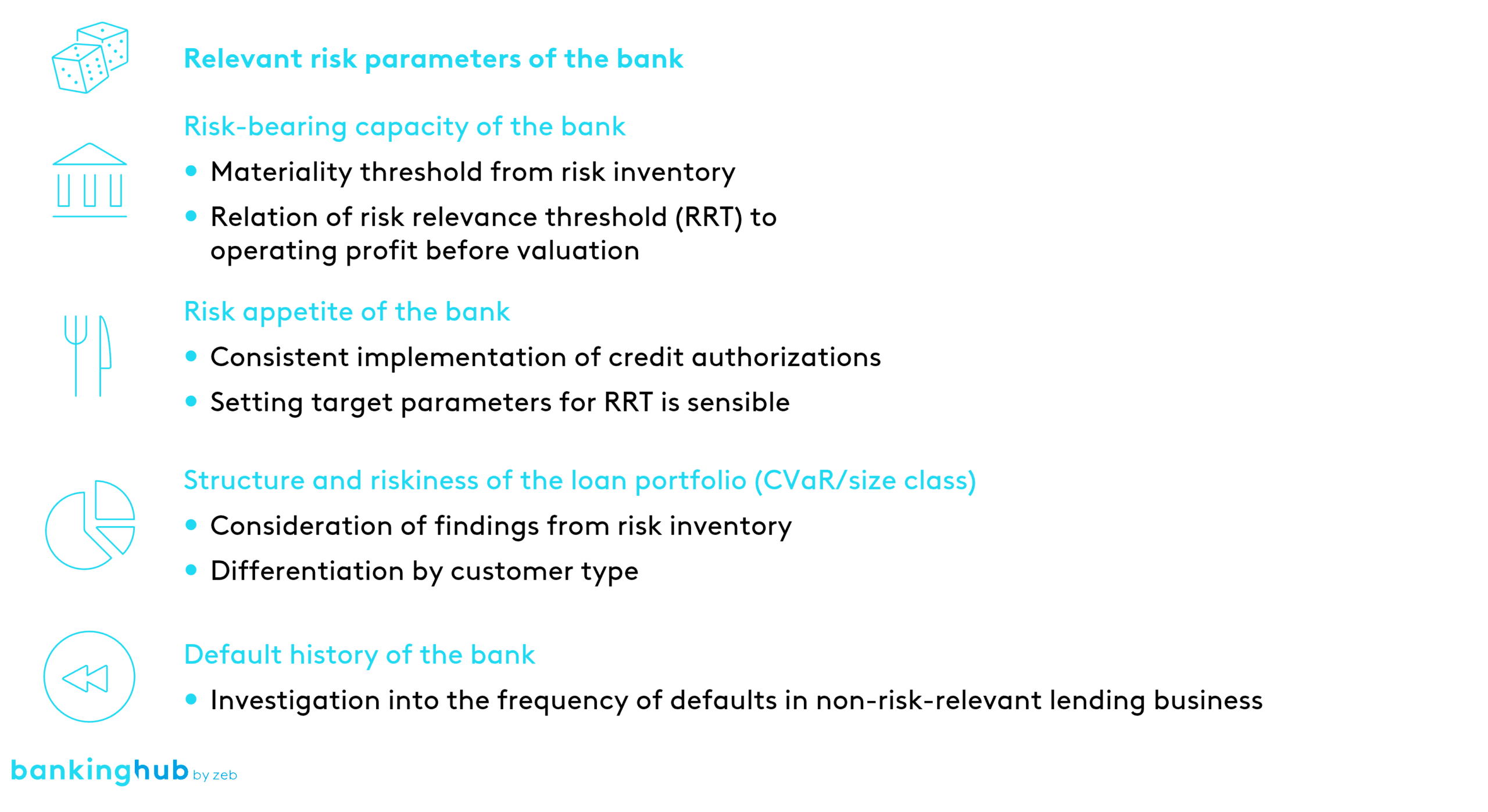

The risk relevance threshold must be validated annually and on an ad hoc basis, for example in the event of a change in the risk situation or for new business areas. A careful and audit-proof derivation of the risk relevance threshold is of crucial importance in order to meet regulatory requirements and at the same time increase the efficiency of lending processes. Various risk parameters should be taken into account, for example the borrower’s creditworthiness, the type and amount of collateral as well as the term and structure of the loan.

At the same time, the strategic objectives and risk appetite of the institution must also be considered in the derivation process. Regularly reviewing and adjusting the risk relevance threshold ensures that the defined thresholds always correspond to the current circumstances and risks of the loan portfolio.

Finding the right level

Banks often deliberately decide to set a lower risk relevance threshold than would be possible from a risk perspective.

When internally determining the proper level, other circumstances and limits in the lending business must also be taken into account. For example, a loan volume of more than EUR 750,000 results in increased efforts, as this is the disclosure threshold for documents relevant to creditworthiness in accordance with Section 18 of the German Banking Act (KWG) and the rating procedures also include additional requirements above this amount.

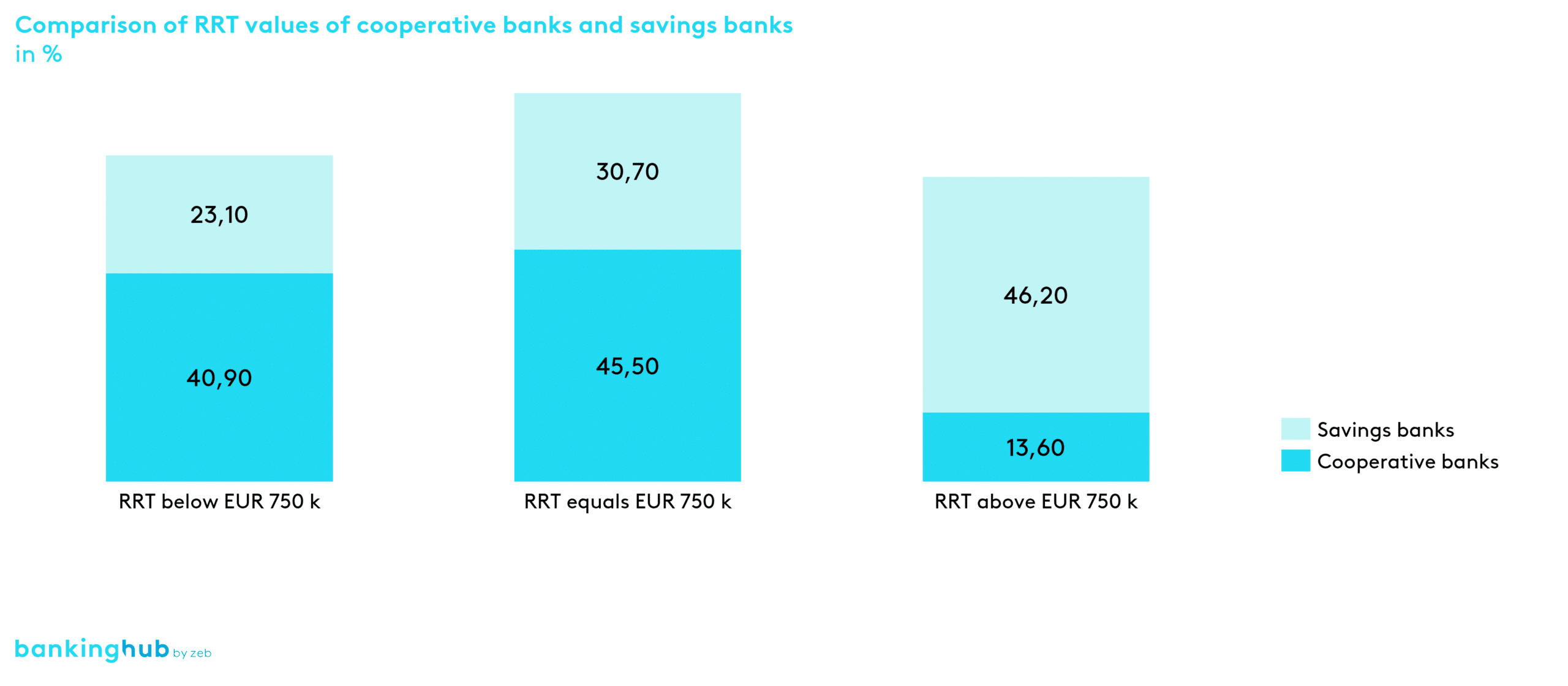

Our latest lending business study shows that the proportion of institutions with a risk relevance threshold of more than EUR 750,000 is still relatively low. The proportion is higher for savings banks than for cooperative banks, which is due to the fact that savings banks are larger on average (see Figure 3[1])

It can make sense to set the threshold at over EUR 750,000, as the scope and complexity of risk assessments below the risk relevance threshold may be lower. This concerns, for example, the calculation of debt service capacity and the preparation of votes.

The level of the risk relevance threshold is also important for deriving other limits and thresholds in the lending business. Careful consideration of the advantages and disadvantages of a higher or lower risk relevance threshold is therefore essential.

- A threshold that is too low can lead to an unnecessary strain on resources and restrict flexibility in lending.

- Too high a threshold, on the other hand, can increase risk and jeopardize compliance with regulatory requirements.

It is therefore important to make a balanced and well-founded decision that ensures both efficiency and compliance with regulatory requirements when defining lending processes.

Process simplifications in lending

The process simplifications resulting from the definition of the risk relevance threshold are diverse and affect various areas of the lending business. The clear separation between risk-relevant and non-risk-relevant loans means that the review and approval processes in non-risk-relevant lending business, for example, can be simplified and/or completely automated. This leads to faster processing of loan applications and greater customer satisfaction.

In addition, by setting the risk relevance threshold, the requirements for documentation and disclosure can also be relaxed, which further reduces employee workloads and increases efficiency.

Example: With a risk relevance threshold of EUR 750,000, authorizations can be designed in such a way that loans up to this amount can be granted without a second approval or vote by the back office. Advisors can give their customers a loan approval much more quickly and do not require someone else to check it.

Furthermore, the risk relevance threshold often serves as the basis for deriving other important thresholds and processing standards in the lending business. These include authorizations, collateral review thresholds, de minimis thresholds for early risk detection, follow-up disclosure and debt service capacity calculations. These are directly dependent on the level of the risk relevance threshold. The definition of the risk relevance threshold therefore has far-reaching effects on the entire lending process and can lead to considerable simplification and efficiency gains.

Example: The institution previously had a risk relevance threshold of EUR 250,000. From this, a threshold amount for early risk detection was derived, below which only simplified processes are carried out. Here, 20% of the risk relevance threshold, i.e. EUR 50,000, was specified as a de minimis amount on a risk-oriented basis. Raising the risk relevance threshold to EUR 1,000,000 would result in an increase in the threshold for early risk identification to EUR 200,000.

Applying de minimis rules

Irrespective of the separation into risk-relevant and non-risk-relevant lending business, the Minimum Requirements for Risk Management (MaRisk) also permit the use of de minimis rules. These are particularly interesting if a relatively small additional loan is to be granted for a risk-relevant credit exposure. In such cases, dual approval is not mandatory, and the front office can make a lending decision on its own within defined limits.

Here is an example: A customer already has a EUR 1 million loan and needs an additional EUR 50,000 for a short-term investment. Within the defined de minimis thresholds, the front office could make this decision independently without the need for additional approval.

The de minimis rules enable banks to react quickly and flexibly to customer needs. By clearly defining de minimis thresholds, lending decisions can be made more efficiently, and employees’ workloads can be reduced. This leads to greater customer satisfaction and improved competitiveness for banks. The use of de minimis rules therefore offers a valuable opportunity to increase flexibility and efficiency in the lending business in compliance with regulatory requirements.

Conclusion on optimization in the lending business using the risk relevance threshold

The risk relevance threshold is of enormous importance for organizing the lending business in banks and represents a key lever for optimizing processes in lending. The clear separation between risk-relevant and non-risk-relevant loans enables banks to improve their risk management and deploy their staff efficiently.

The use of de minimis thresholds can further increase efficiency and flexibility when granting loans. Careful and audit-proof derivation and regular review of the risk relevance threshold are essential. In this context, the following should be noted:

- A process and a fixed time for carrying out the regular validation should be agreed. Criteria for ad hoc validation should also be defined.

- The validation should be based on current portfolio data and risk appetite. In addition, experience with previous process simplifications in the front and back office should be taken into account.

- The implications for downstream processes and the consistent implementation of the risk relevance threshold should always be considered.