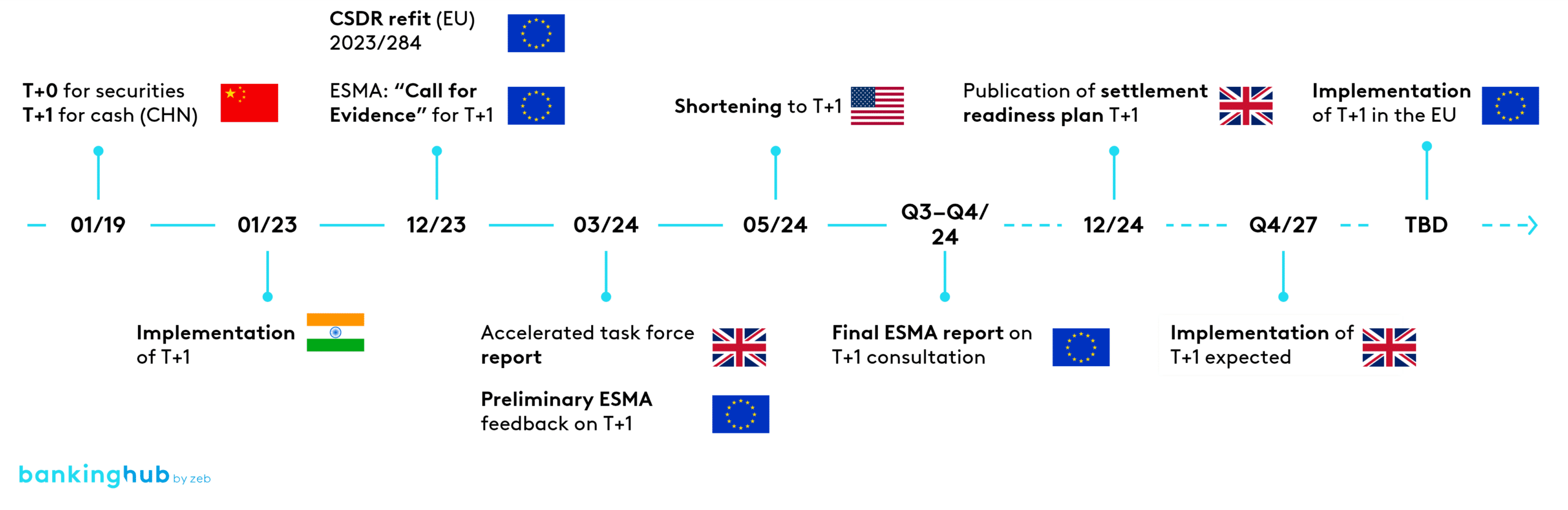

Current discussions about T+1 in the EU follow international trend

The T+2 settlement cycle for securities transactions currently applies across the EU. This means that the settlement of a trading transaction typically occurs two business days after the trading day (T+2). The T+2 rule derives from the Central Securities Depository Regulation (CSDR), which has governed the legal framework for the settlement of securities transactions and central securities depositories (CSDs) in the EU since 2014.

In light of global developments, particularly the introduction of the T+1 settlement cycle in the USA, there is intense debate in the EU about shortening the settlement cycle to T+1, too. This shows that the discussions in Europe follow global trends: China has already implemented T+1 for cash and T+0 for securities since 2019. India is seen as a pioneer as it has had a full T+1 settlement standard in place since January 2023. Canada followed the USA’s lead and introduced T+1 on the same date.

Against this backdrop, the European Securities and Markets Authority (ESMA) has been commissioned to conduct a cost-benefit analysis regarding the introduction of a T+1 settlement cycle in the EU as part of the CSDR Refit at the end of 2023.

In March 2024, ESMA published a preliminary statement. It shows that market participants see obstacles to the introduction of a T+1 settlement cycle, such as the need for extensive technical adjustments. At the same time, however, a shortened settlement cycle is considered to be unavoidable in the medium to long term, as otherwise the competitiveness of the European market would be jeopardized.

ESMA’s final report, containing further findings, is anticipated for publication in the third or fourth quarter of 2024. This report is expected to include a statement on implementation planning.

Additionally, the UK is expected to present a timetable for the transition to a T+1 settlement cycle in parallel to the EU by the end of 2024, aiming for full implementation by the end of 2027. Market participants’ concerns about potential problems caused by a misalignment between the UK and the EU support the theory that the EU will also aim for implementation by the end of 2027.

Adjustments to the operating model, trade processing and business practices necessary

In order to meet the requirements for a possible T+1 settlement cycle, financial market players must make far-reaching process-related and technical adjustments.

Optimization of the operating model

One of the most significant consequences of the transition to T+1 is the drastic, nearly 80% reduction in available processing time. This change demands a high level of automation and harmonization of settlement processes. In the future, financial market participants will need to perform many tasks, such as affirmation and confirmation, on the trading day itself to provide an adequate buffer for downstream processes.

In addition, the transition requires the development of new or the enhancement of existing standards, particularly in the context of the Standard Settlement Instructions (SSIs), to ensure efficiency and consistency in settlement.

Coordination with intermediaries

The introduction of T+1 increases the complexity of global trade. Different markets have different trading and settlement times, creating additional challenges for coordination and harmonization.

The successful implementation of T+1 therefore requires that the processes between the various intermediaries, such as banks, asset managers, custodians and CSDs, be closely aligned and coordinated. This includes, for example, a possible adjustment to the start of T2S night-time settlement.

Adjustments to business practices

The need to ensure the timely availability of securities also affects securities lending. Securities lent must be delivered in good time to enable settlement, creating additional challenges for market participants.

Adjustments are also necessary for cash management, particularly regarding the change to the SEPA direct debit procedure and foreign exchange transactions. Up to now, SEPA payments have to be announced to the service provider the day before the payment, which would no longer be feasible under a T+1 standard. Optimized liquidity management will therefore be required.

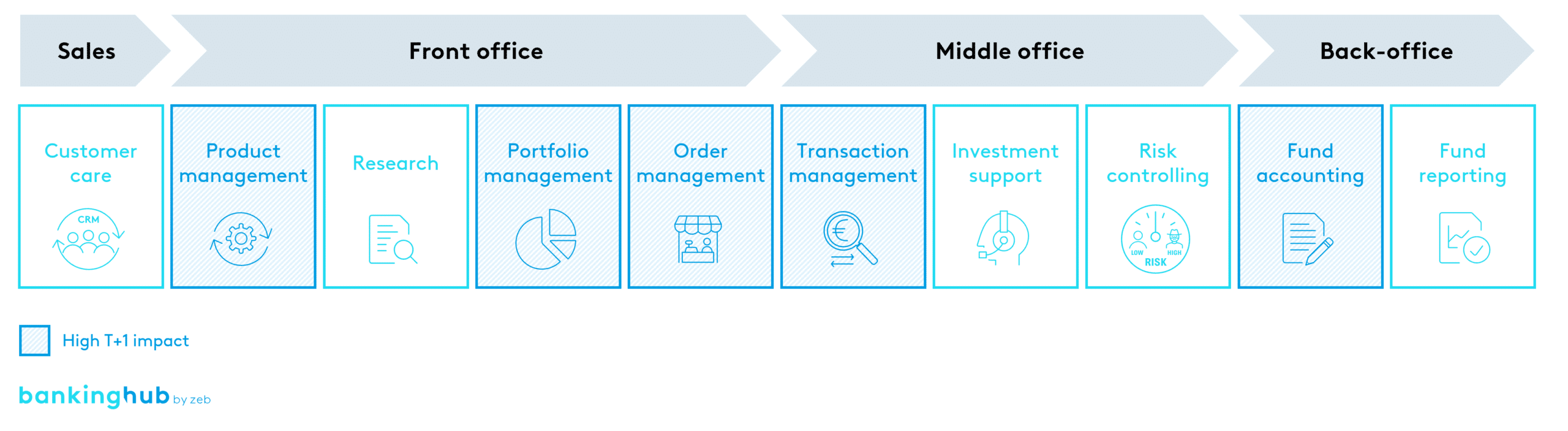

Spotlight on asset management: implications for the entire value chain

The transition to T+1 will have a profound impact on the entire asset management value chain, making early action necessary.

Sales department and front office

In product management, legal documents and sales prospectuses for individual investment products must be adapted to the new market standard. In addition, higher levels of cash and cash equivalents are required for portfolio management purposes. This is to ensure the settlement of FX transactions, particularly in foreign currencies, within the T+1 settlement cycle.

Another crucial aspect of order management is the selection of trading partners based increasingly on efficiency criteria in order to optimize order routing and ensure the swift execution of transactions.

Middle office

Transaction confirmation and matching processes require a faster workflow and a higher degree of automation. Close system integration and adaptation of the systems to near-time communication/

coordination (SWIFT, FIX) to ensure more consistent and faster collaboration are beneficial.

The introduction of standardized electronic systems for all matching processes also helps to comply with the new, significantly shorter cut-off times. The excursus in the next section examines the challenges in transaction management in more detail.

Back-office

Comprehensive optimization and automation are particularly necessary in payment processing and NAV calculation. Prompt implementation of these adjustments prevents delays in downstream process steps. Waiting times should be minimized and calculation processes parallelized.

The use of APIs for the direct provision of NAV calculation results saves additional time. In addition, documentation and regulations must be adapted to the new requirements.

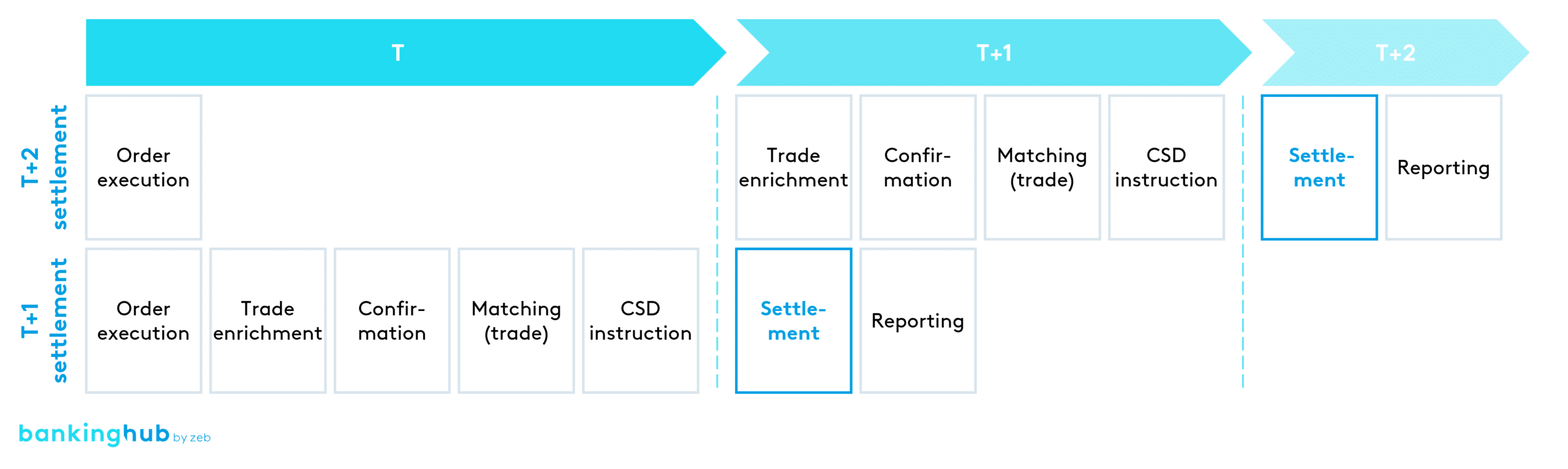

Excursus on transaction management: shifting existing processes to time T is essential

The transition to the T+1 settlement cycle places very high demands on transaction management, as key processes need to be accelerated. A crucial step is to complete the processes that follow order execution on trading day T+0 so that settlement and downstream reporting can take place on T+1.

Shortening the process flow requires significant adjustments to processes and systems. One challenge in trade enrichment is maintaining data quality and integrity. Often, manual adjustments are necessary due to late, incomplete or inaccurate data. Additionally, a lack of data synchronization between systems and parties involved frequently results in inconsistencies and delays.

A similar challenge can be observed in trade matching: the T+1 cycle shifts the clearing partners’ cut-off deadline, requiring an earlier conclusion. This means that existing matching systems and processes have to be reconfigured.

To ensure T+1, challenges in trade confirmation must also be overcome. Status delays often occur due to errors in economic or non-economic data. Furthermore, batch or end-of-day processing, which can be necessary for business or technical reasons and sometimes takes several days, leads to additional waiting times.

zeb recommendation: early impact analysis to identify challenges

The transition to T+1 incurs considerable direct and indirect costs, especially for system enhancements and process optimizations. The simultaneous introduction of T+1 in different regions such as the UK, Switzerland and the EU, each with unique timelines and constraints, further increases complexity. Given these factors and the wide-ranging effects of the T+1 transition, it is crucial for financial institutions to act early.

We recommend conducting an impact analysis to determine how to achieve settlement in T+1. This analysis can be used to derive a target picture as a guide for subsequent implementation.