Transformations have already begun in payments

In Germany, it took until 2018 before the majority of payments were cashless for the first time. The younger generation in particular shows a high affinity for mobile payment methods, which has led to a significant shift from cash to cashless transactions in recent years.

Instant payment is another real cash alternative that offers low costs and high convenience. At the same time, regulatory attention has increased in payments. Not everyone in the payments market—acquirers, issuers, gateways, processors, payment service providers (PSP), etc.—is affected by the changes in equal measure.

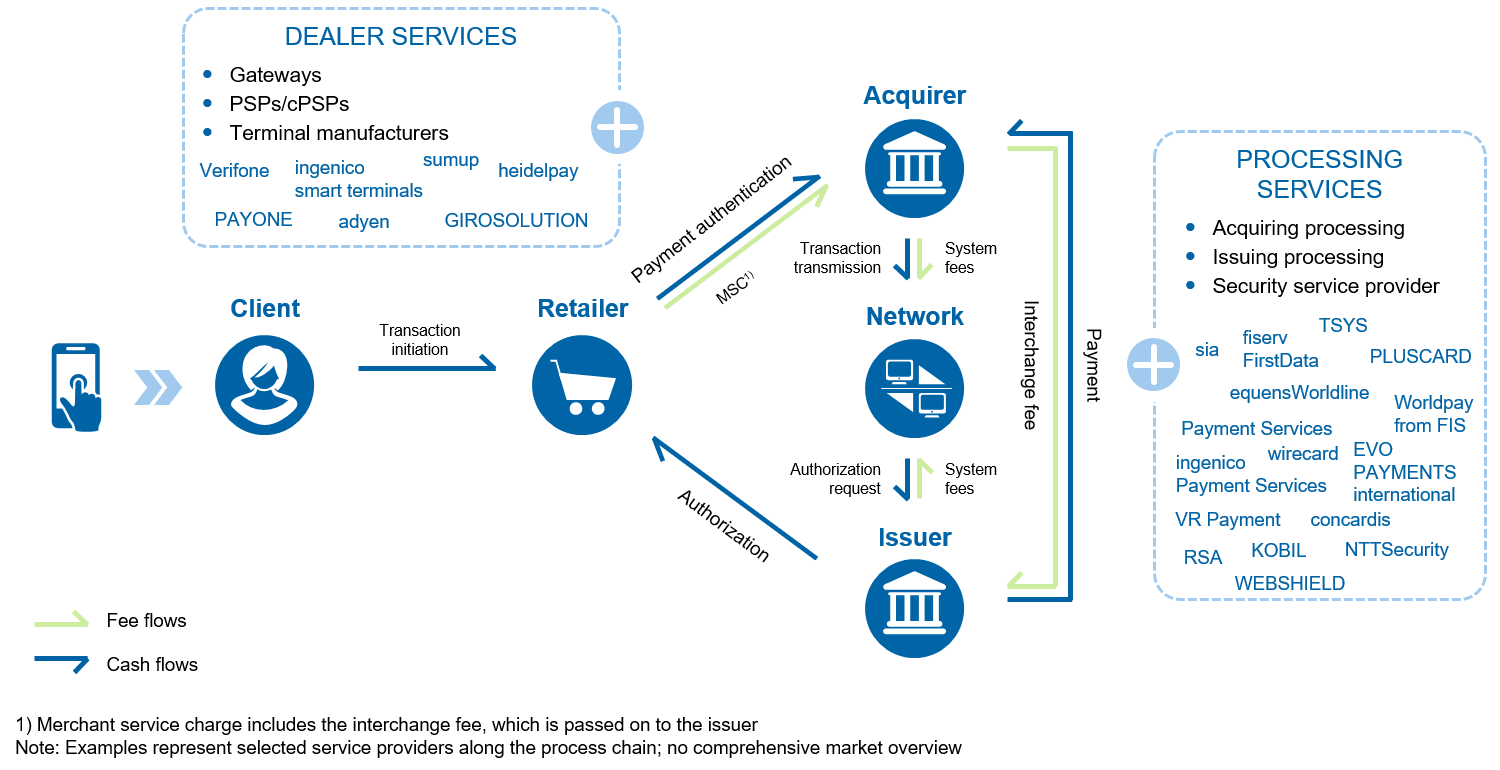

Figure 1: Overview of market participants in payments (using the example of a card transaction)

Figure 1: Overview of market participants in payments (using the example of a card transaction)German banks have partially withdrawn from the payments market, for example with the sale of Concardis in 2017. At the same time, existing market participants have joined forces in several waves—also catalyzed by investments from private equity investors.

In addition to the market shakeout, digitalization is fundamentally changing the way payment transactions are carried out both at the point of sale and in e-commerce—especially the user experience. Fintech and big tech companies are bringing innovative payment methods such as Apple Pay or Amazon Pay to the market in order to increasingly position the smartphone as a mobile wallet and to be able to offer customers another product in their ecosystem. As a result, it is primarily those players who are at the customer interface who are in the field of tension.

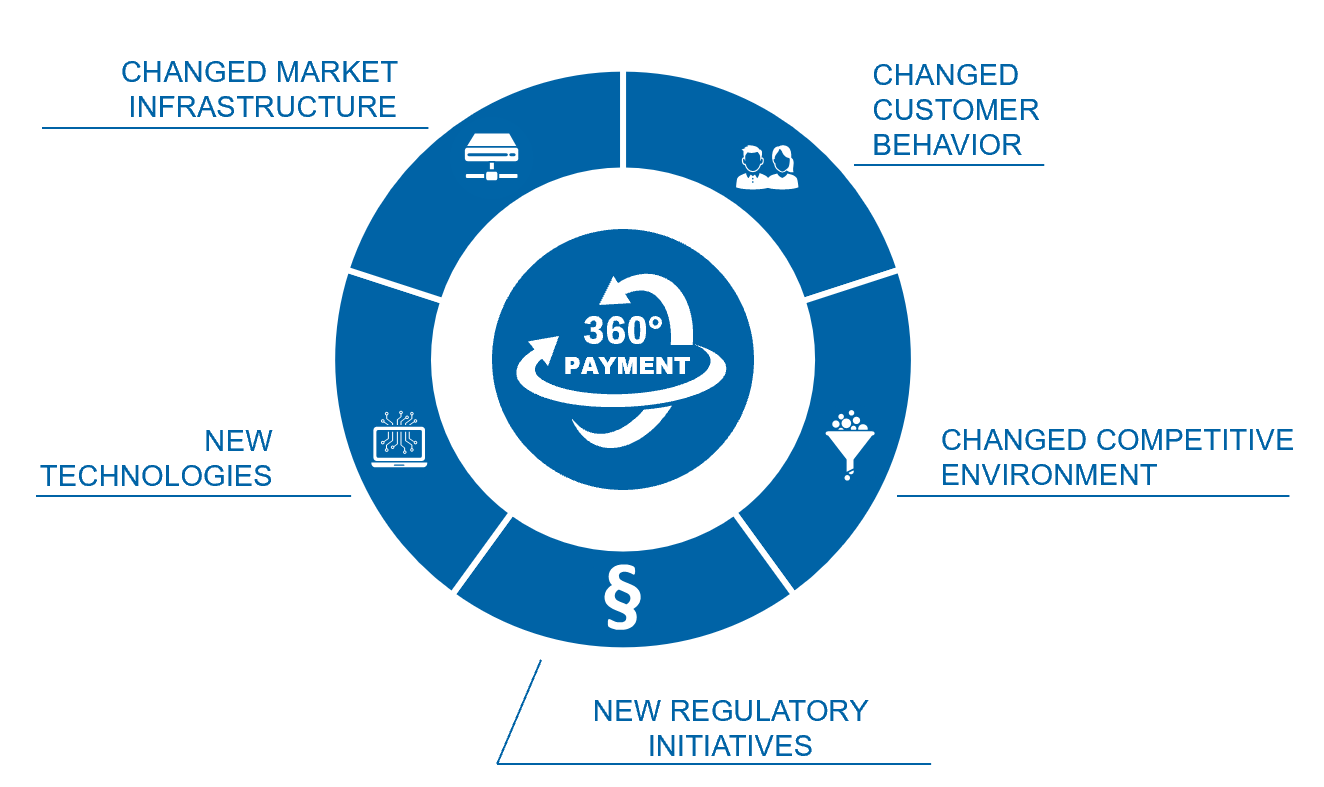

In summary, five factors have an impact on the payment industry: (1) changed customer behavior, (2) changed competitive environment, (3) new regulatory initiatives, (4) new technologies and (5) changed market infrastructure (see Figure 2).

Figure 2: Change drivers in the payments market

Figure 2: Change drivers in the payments marketCustomer behavior: customers’ need for fast, secure and smooth payments

As part of digitalization and new innovative competitors joining the market, payment service providers have to cope with changing customer requirements. The factors critical to success here include a clear customer orientation and a high degree of flexibility in payment solutions.

Aside from these success factors, it is also important to meet central requirements for the payment procedure from the customer’s perspective:

- Fast—immediate execution and settlement of national and international payments around the clock (24/7)

- Simple—smooth processing of payments without media/channel interruptions

- Secure—permanent data and transaction security and transparency to protect against fraudulent activities

- Cost-effective—reduction of existing costs for executing (international) transactions

- Anonymous—no electronic traceability of individual transactions on a personal basis

Due to the high dynamics and growth in the market, German end customers are now increasingly turning to cards rather than paying with cash. As reported by the retail research institute EHI, for the first time in Germany more was paid for with a debit or credit card than with cash (card payment: EUR 209 bn, cash payment: EUR 208 bn)[1].

Furthermore, (mobile) payment providers with their real-time solutions will be able to further increase the rate of adoption in Germany in the medium term if acceptance on the part of merchants is further expanded.

With regard to instant payments, merchants should be able to obtain payment security similar to that of credit cards, but at a much lower cost, giving them a genuine 24/7, immediately valid, irreversible payment similar to cash.

Although Bitcoins and the like are a largely comparable anonymous form of payment, they are only suitable to a limited extent as a cash alternative as a way to retain values and have clearly limited usability.

Competitive environment: increased competition due to new participants entering the payment market

Innovative payment methods such as mobile payments are already a reality in many countries, and new domestic and international solutions are regularly being added Europe. The rapidly growing number of new competitors is intensifying the dynamics, and at the same time the new providers are intensifying the market environment with their aggressive pricing models and their ranges of modern and flexible products.

Numerous fintech companies have successfully managed to fill the customer interface in B2B and B2C. Even world-leading fintech companies such as Wirecard, Adyen, TransferWise and PayPal now have to assert themselves against the large tech corporations (GAFA)[2], which have significant dominance over (mobile) devices and customer data.

In this competition, it is very promising to also look at global interaction between players. Wirecard was the first payment service provider to successfully integrate the two most famous Chinese payment methods – Alipay and WeChat Pay – into the European retail sector[3].

The key difference to Wirecard is that Google, Apple and Facebook do not primarily want to offer banking products, but rather use the payment functionalities primarily as an extension of their data-based business model. For this reason, some of them do not pursue direct profit-making intentions like traditional banks, but are primarily interested in customer data—what they want is primarily data, not money.

In addition to this development in the sector, there are start-ups that aim to build new payment platforms on a “greenfield site” instead of using grown infrastructures. Shorter innovation cycles and agile product development are success drivers for the new competitors, allowing them to offer better products to customers.

Adyen, a Dutch payment processor, managed to increase its transaction volume by 55% within two years. This success story highlights the shift in market share in the industry and at the same time shows the untapped potential in the payment industry. With Revolut and TransferWise, there are also extremely successful market entries in the market for processing international payments—they are clearly outperforming the historically grown cost structures of banks.

Regulatory initiatives: new guidelines to promote innovation and competition

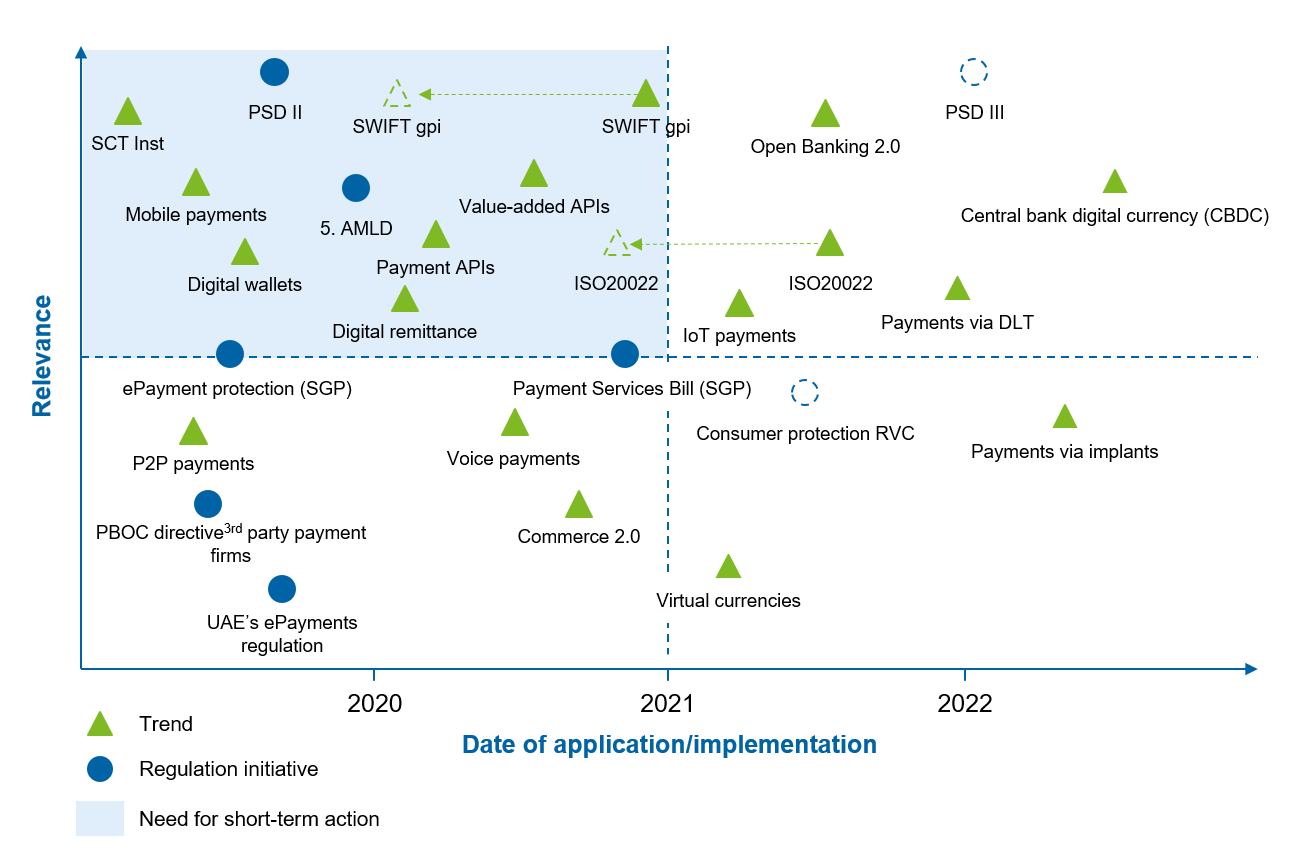

Figure 3: Overview of trends and regulatory initiatives in payments (extract)

Figure 3: Overview of trends and regulatory initiatives in payments (extract)The legislative pressure on the payments sector has increased considerably in recent years. Regulatory initiatives and requirements must be anticipated promptly and implemented efficiently. The regulatory initiatives are mainly aimed at further harmonizing payments, increasing consumer protection and promoting innovation.

In particular, the new EU Payment Services Directive PSD II[4] enables innovation and increased competition—among other things by opening up account information to third parties. At the same time, PSD II increases the security of payments through stricter requirements for customer authentication. In the next few years, we expect further consumer protection-oriented initiatives to be taken, which will be combined into a kind of PSD III.

Figure 3 shows the main upcoming trends and regulatory initiatives. On the one hand, these initiatives tie up resources for implementation on the part of the payment service providers, but on the other hand they promote innovation and competition.

Technologies: Use of new technologies to reduce costs and increase efficiency

The increased competitive pressure, caused by fintech and big tech companies, among others, is pushing existing market participants to invest. This is because, in a direct comparison, the new competitors have significantly lower basic costs due to their “greenfield” platforms, some of which are very focused, and strong IT teams.

The use of modern technologies offers the necessary flexibility to respond to ever-changing customer requirements. At the same time, existing manual processes are improved and costs are significantly reduced. Two promising technological developments in payment are artificial intelligence (AI) and open banking.

AI can be used for process automation in customer service and for the optimization of payment flows, while offering enormous cost reduction potential. The demand for AI solutions in the back office areas will increase, especially with the increased market penetration of real-time payments, for example to perform fraud and embargo checks in real time.

The enormous potential is offset by possible restrictions due to the strict data protection and regulatory requirements in Germany. AI solutions must therefore be checked for their legal feasibility early in the conceptual design stage, and an assessment of the potential to be realized must be made.

Open banking enables the provision of new solutions through the use of APIs[5], which are designed to greatly simplify cooperation. New solutions can thus be integrated quickly into ecosystems and partnerships without frictional losses. An example of a new API that is important for payment transactions is the XS2A API, which within the framework of PSD II.

In the future, non-payment APIs such as digital identity services or intraday bank statements will also gain in relevance. In addition, consortia such as The Berlin Group are already working on the first value-added APIs.

Market infrastructure: replacement or revision of outdated payment infrastructure in the market

At the same time, various global initiatives are being worked on with the aim of modernizing the payment infrastructure. The modernization includes the renewal of clearing and settlement mechanisms, the introduction of real-time gross settlement systems and the consolidation of TARGET[6] services on a central platform.

Examples include new standards for international payments such as SWIFT gpi and new communication standards such as ISO 20022. This requires planning and implementation efforts with a high involvement of resources on the part of the market participants, which must be made in line with the implementation of regulatory requirements.

Munich Airport’s roughly 48 million annual passengers will be able to use a new type of mobile payment. Wirecard, SES-imagotag and wirecube have jointly developed a “Smart Checkout” version for mobile payment, enabling customers to pay with their own smartphone directly at the shelf using an electronic price tag[7]. This clearly reshapes payment infrastructure leaving out classic POS terminals and cashiers even in store.

Conclusion: Payments—an industry undergoing radical change

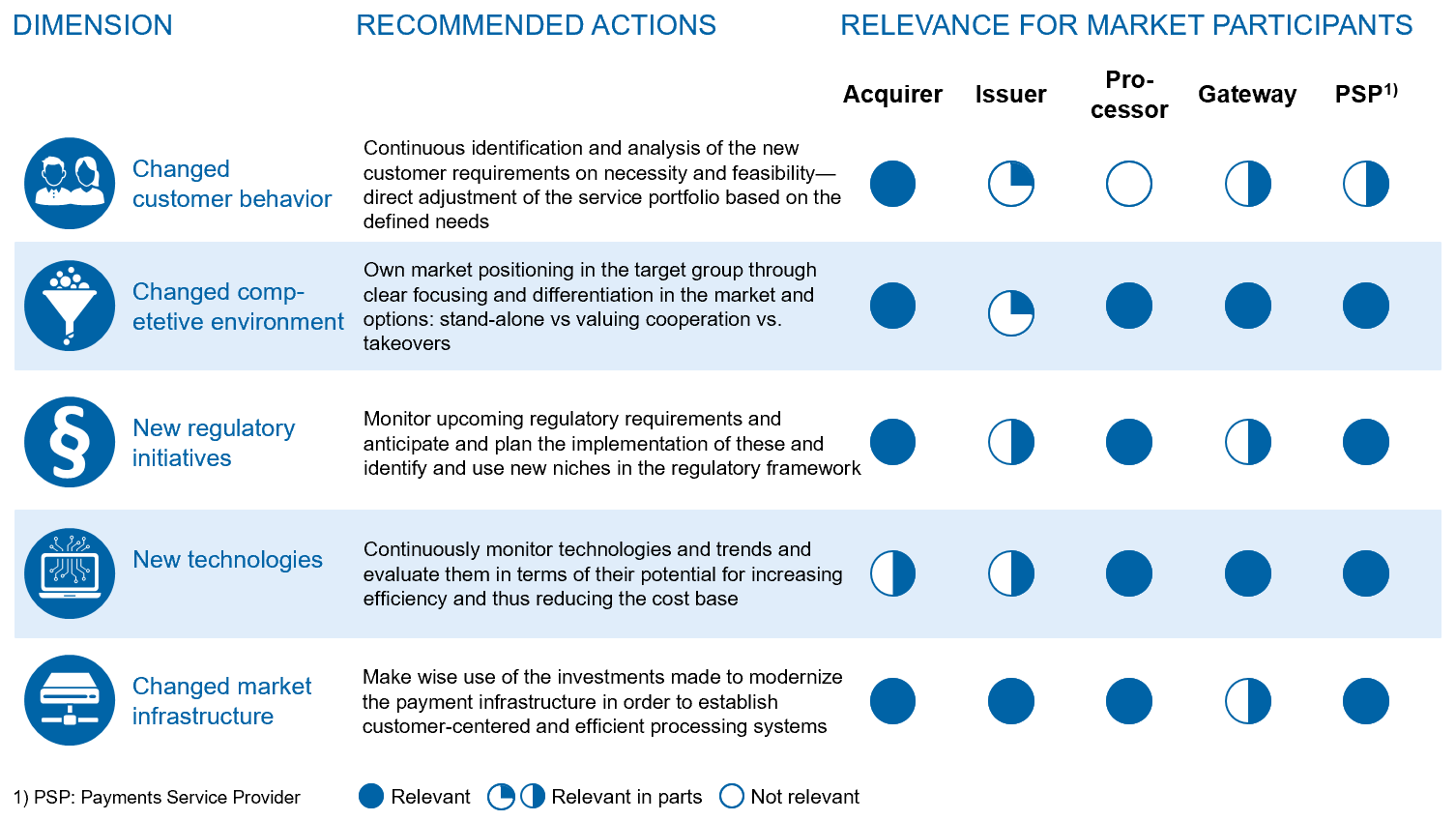

The five dimensions mentioned above result in different recommendations for action for the individual market participants along the value chain. In Figure 4, these recommendations for action are evaluated by dimension for the players in the payment industry.

Figure 4: Relevance of the dimensions and recommendations for action for payment market participants

Figure 4: Relevance of the dimensions and recommendations for action for payment market participantsThe changes described above result in a high level of pressure for action by market participants. The resulting needs for increased investment and resources have led to consolidation within the payment sector in recent years and new competitors in the form of fintech and big test companies entering the market. The reorganization of the German and European markets present an opportunity for the establishment of a new competitive structure.

Innovative payment methods will become more widespread in the German market. Due to the withdrawal of the German banks, they have not yet taken up a strong strategic position, while at the same time the new payment providers are on the advance. German banks are thus faced with the challenge of making the classic “make, cooperate or buy” decision and, against the background of their overall strategy, to position themselves clearly in the payment industry as well.

One response to “Payments—an industry undergoing radical change”

Digital payments

Technology innovation in modern times is driven by demand. Specifically, through the pursuit of addressing the needs of small businesses, technology developers are getting more and more demand-oriented. Anyway, the demand is indeed consistent in modern times, which makes the technology developers focus on innovation; rather than just productivity.