These new market players focus on fully digitalized and customer-centric solutions – for now, mostly in the payments and accounts area—and offer them at extremely favourable prices, as they benefit from economies of scale and are not hindered by legacy infrastructures. Swiss banks thus have to launch digital offers without rushing into cannibalizing their existing and at present still profitable business models.

“digital pulse check”: survey of almost 50 Swiss banks in collaboration with SFI

To determine the digital pulse of Swiss banks, zeb and the Swiss Finance Institute (SFI) have transferred the well-established digital pulse check to the Swiss market. 46 representatives of Swiss banking institutions participated in the survey and answered 50 questions, which were divided into the four core dimensions “Digitalization Strategy”, “Business Model”, “Data, Processes & IT” and “Management & Organization”. The share of Swiss participants in the overall survey amounts to 25% and thus enables a substantiated comparison of Swiss banks and their European peers. The survey findings are complemented by 19 qualitative C-level interviews with representatives of all banking sectors and bank sizes.

Top-class in terms of strategy, but with a need to speed up implementation

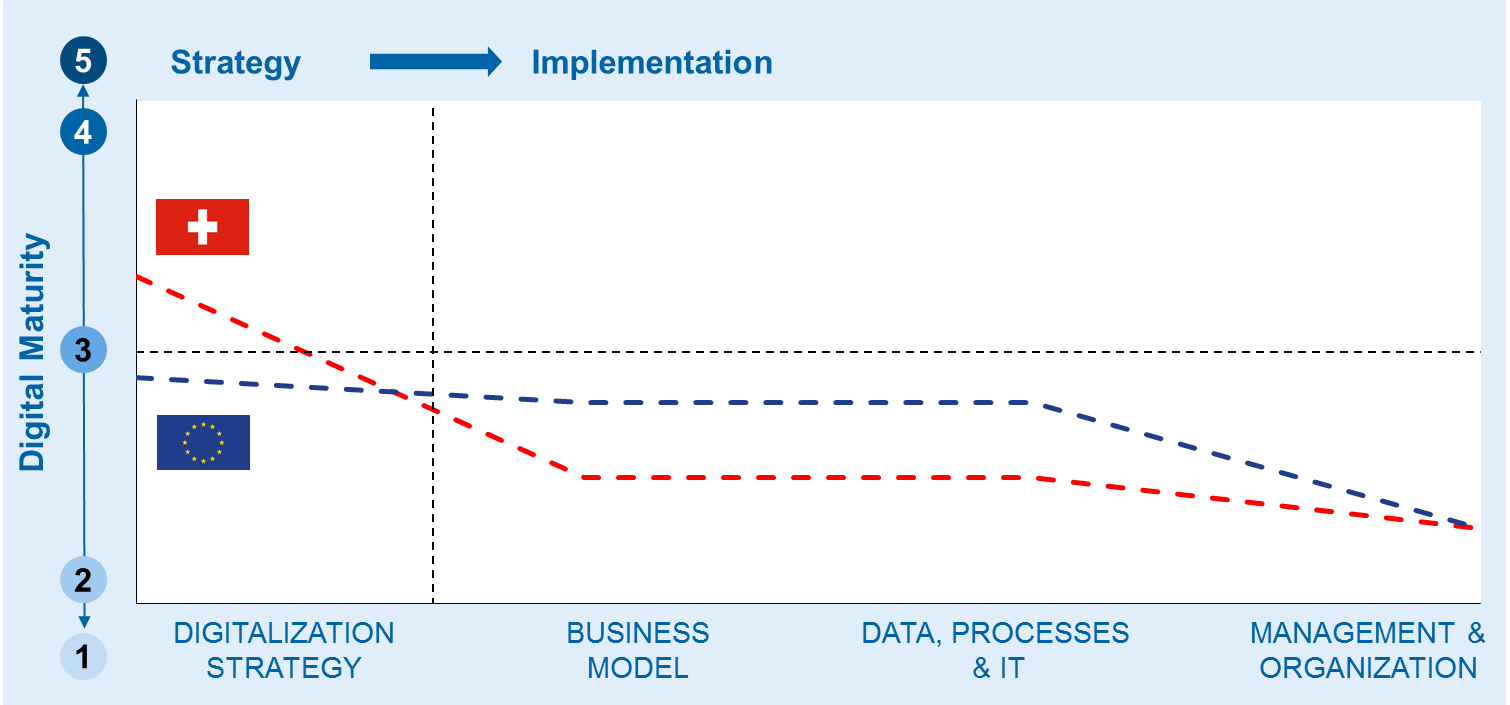

The Digital Pulse Check survey and interviews reveal that Swiss banks have no reason to shun comparison with their European peers when it comes to strategy. They have a clearly lead in strategic trend recognition and in drafting the digital agenda. Based on this finding, one would assume a similar advantage in the implementation dimensions, yet the data analysis shows a different picture: not only do Swiss banks lose when it comes to implementation—they are clearly lagging behind their European competitors with regard to implementing digital business models and preparing processes, data management and IT for the challenges of the digital word (see figure below).

Figure 1: Comparing digital maturity / digitalization progress of Switzerland and Europe

Figure 1: Comparing digital maturity / digitalization progress of Switzerland and EuropeRoughly 60% of Swiss banks only offer less than half of their products and services online. Additionally, user interfaces are mostly not optimized for mobile use. It is nearly impossible to switch channels without any friction. The “Data, Processes & IT” area reveals that Swiss banks are less inclined to opt for end-to-end automation and processes than European banks. In data analytics, domestic and foreign banks are on a par: approximately 50% have not started any or have just started first initiatives. Many banks still do not regard data as an asset and thus miss out on opportunities.

“digital pulse check” indicates lack of digital pioneers among managers and employees

Institutions both in Europe and in Switzerland show deficits in the “Management & Organization” area. Banks mostly lack “digital leaders” who possess extensive digital know-how, actively integrate it into their leadership strategy and also promote the development of digital skills for their employees. This is of central importance: the analysis clearly proves that banks with a high proportion of executives with a “digital mindset” also lead the way in driving transformation forward. Agile working methods and network organizations have been implemented far more consistently and holistic IT strategy and architecture management has been introduced more frequently, just to name some examples. It is therefore difficult to benefit from the best strategy if you are not able to derive and implement concrete measures.

«Banks are afraid of cannibalizing their current business model by investing in digitalization.

CEO of a big Swiss bank “digital pulse check”

Three overarching key conclusions can be drawn from the study to ensure future success in a digitizing banking world:

- Don’t miss the moment: Swiss banks report that they mostly apply a “smart follower” approach. Their stated goal is to learn from others’ mistakes and then take the necessary steps to jump on the bandwagon. Considering the numerous unknowns and risks, the logic behind this approach can hardly be denied. Banks can thus benefit from the advantages of a de facto somewhat shielded market. Nevertheless, this approach entails the risk of being late and missing the right moment to implement defined strategies and concepts in order to catch up with leading international competitors as well as with new contenders. This is especially true, if banks lack the will to experiment with new and innovative (greenfield) approaches.

- Involve and convince your employees: At the same time, most participants state that the further digital development of their organization is greatly important for its future success. According to the interviews, employees also have to embark on the digital journey. The digitalization of the financial sector begins in people’s minds, either in spite or because of the impending fundamental structural change of the industry. Only when banks succeed in preparing and motivating their employees for the digital transformation and foster the development of digital leaders across a bank can digitalization be successful for all involved.

- Become more agile: Digital realignment requires that banks also radically rethink their organizational structures. A strict separation of IT-data management and business expertise is not conducive to achieving objectives and is increasingly being replaced by a more agile approach, even if currently mostly limited to projects. The skills of business and IT experts need to be merged and also combined with cutting-edge expertise in analysing and developing customer-centric solutions to harness the innovative power that is necessary for keeping up with the new dynamic competitors. The infrastructure has to be promptly prepared to accommodate, for example, a flexible and cooperative IT architecture and an integrated data management, in order to evolve banking according to changed customer expectations and new technological opportunities. Here certain banks should also deliver Greenfield-approaches.

Conclusion from the “digital pulse check” survey

In summary, it should be noted that the focus of the Swiss banking sector should not be so much on digitalizing the banking business, as it should be on developing a digital Swiss banking, which will bring the unique features of the Swiss banking system in line with the unavoidable digital evolution. The path towards this goal is fraught with risks. However, Swiss banks have built a solid foundation on which they can continue to develop their digital future, as long as they demonstrate the same level of ambition in the implementation of digitalization as they have shown in the strategy development phase.

SFi: Swiss Finance institute