Background

The background to these measures is the development of prices in the commodity and food commodity markets over the previous years which was characterized by—in parts quite significant—price rises in combination with extreme fluctuations. This development is not regarded as due to a changed market situation regarding supply and demand, but the price effects result primarily from the commitment of the market participants in derivatives of the commodity types mentioned.

Subject of regulation

In order to achieve a reduction in commodity speculation, the entry into force of MiFID II in January 2018 will be accompanied by the introduction of position limits in commodity derivatives which are set and published by the national supervisory authorities. These limits determine the maximum position a market participant may hold.

Both securities firms and trading venue operators must provide the national supervisory authority with detailed position reports. For ETDs (exchange traded derivatives), trading venues have to perform a consolidation and provide the national supervisory authority with aggregated position information. For OTC (over the counter) contracts which are economically equivalent to ETDs the securities company has to report directly to the supervisory authority.

Based on the information about the positions reported in combination with the defined position limits, the supervisory authorities can ask market participants to reduce the volume of a certain position.

Scope and definition of commodity derivatives according to MiFID II

The definition of commodity derivatives in the sense of MiFID II covers all options, futures, swaps, forwards and all other derivative contracts relating to commodities. Relevant financial instruments also include all other securities that entitle the holder to buy or sell such securities or that lead to a corresponding cash payment which is determined on the basis of transferable securities, currencies, interest rates or yields, commodities or other indices or metrics.[1]

Thus, in its current form, the definition also includes in particular the entire range of certificates on raw materials, such as gold or oil. The new regulation also concerns emission permits and derivatives of these.

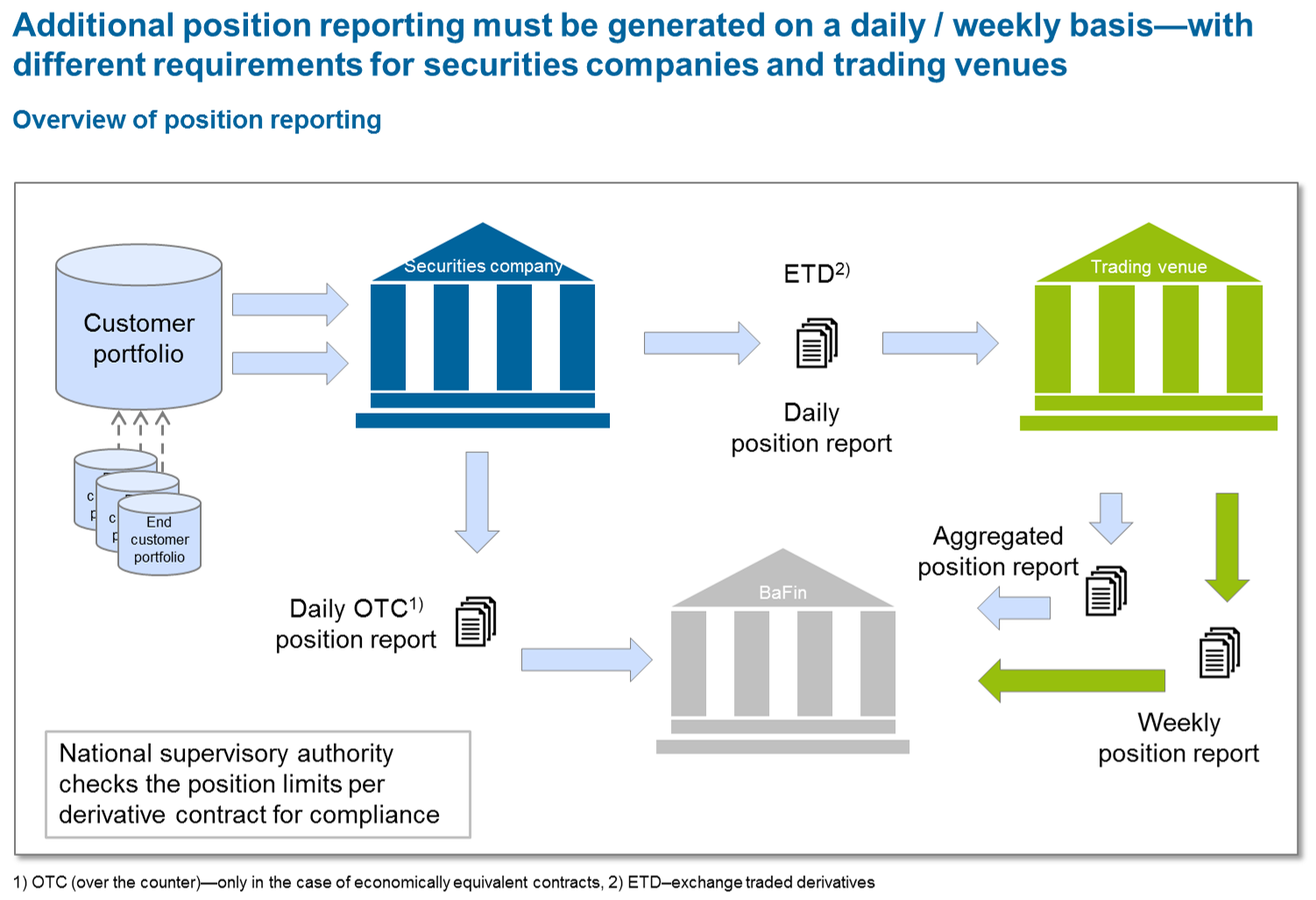

Daily position report and weekly “Commitments of Traders” report

With the “Draft implementing technical standards under MiFID II” (ITS) of December 11, 2015, ESMA published further specifications regarding the obligations defined in MiFID II Art. 58 (5) on position reporting in commodity derivatives, emission permits or derivatives of these in the ITS 4.

The current text (ITS 4) mainly states different reporting obligations for securities companies and operators of trading venues.

Securities companies have to generate a position report per customer on a daily basis. In this report, all positions of the securities company and the customers’ positions right through to their end customers must be disclosed. The respective holders of the position must be clearly identified by means of a legal entity identifier (LEI) or national ID (usually ID card number). For ETD transactions, the report must be submitted to the respective trading venue. Economically equivalent OTC transactions must be reported daily to the supervisory authority in charge. Positions entered into as a hedge in the context of normal business activity must be listed separately as these are not included in the calculation of the position limits.

Additionally, the operators of trading venues are obliged to create a weekly “Commitments of Traders” report showing the total commitment of the market participants in a contract broken down into categories of securities companies.

Figure 1: Overview of position reporting

Figure 1: Overview of position reportingCall for reduction of position in commodity derivatives

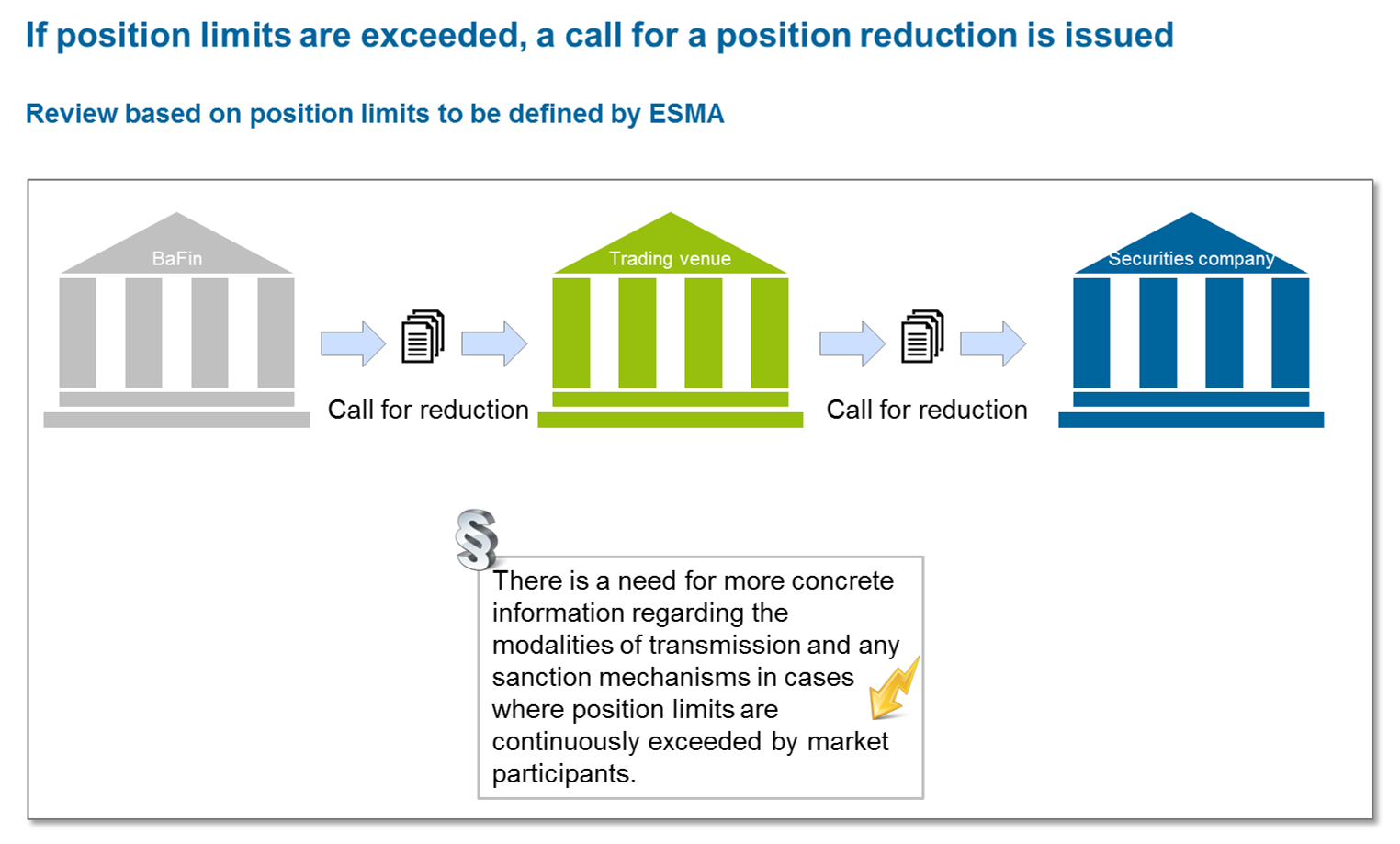

With the new regulation, the supervisory authorities are given the possibility to instruct market participants to reduce positions based on the predefined position limits. If the market participant in question does not follow this instruction, then the trading venue is entitled to take measures allowing the reduction of the position concerned. A more concrete definition of the measures described here or a legal basis for enforcing these authorizations, as announced in MiFID II Art. 57 (14), is still pending on the part of the EU Commission.

Figure 2: Overview—call for reduction of position in ETD transactions

Figure 2: Overview—call for reduction of position in ETD transactionsSchedule and need for action

The entry into force of MiFID II having been postponed, the requirements described above must now be implemented by January 3, 2018. In order to meet the requirements, securities companies must take both organizational and technical implementation measures:

- With a view to recording and maintaining basic customer data, as for all other reporting under MiFID II, the LEI (for legal entities) or the respective national ID (for natural persons) as a means of customer identification must be recorded and, if required, updated on a regular basis for position reporting.

- In future, it must be determined as soon as the order is placed whether a position is used for hedging, i.e. to reduce risk, or whether it is a speculative transaction.

- For the generation of the reports it is necessary to check all accounts daily for positions in commodity derivatives, emission permits and derivatives and to create and submit the daily report based on this. In this context, it is important to note that relevant positions are established not just through purchases, but also for example through deposit account entries. A core issue will therefore be data provisioning for the purposes of position reporting as, for the majority of companies concerned, it cannot be assumed that the required data are already available in consolidated form from a single source. Surely, this must also be considered against the background of additional reporting requirements resulting from MiFID II.

- In the current consultation process, especially the as yet still open questions regarding the concrete details, particularly of the supervisory authorities’ sanction mechanism in the context of position reduction, must be addressed and their development supported. Concretization on the part of the EU Commission is required for the definition of the obligations of securities companies in the context of calls for the reduction of a position. At the moment it is still unclear in how far a securities company is supposed to intervene directly or whether its obligations are fulfilled with communicating the call for reduction to the customer.

- Additionally, organizational measures must be taken and, if necessary, technological infrastructure provided in order to cover the required information along the information chain from end customer to national supervisory authority and, in the case of sanctions, also in the opposite direction.

- In the case of a sourcing approach, the respective customer and end customer data must be provided by the sourcing partner. Regarding the transfer of customer data required for this, it remains to be seen how the market participants concerned will handle the implementation in practice. For instance, it is feasible that trading venues might in future offer reporting as a service as they have most of the required data on hand anyway.

In this scenario as well, the required information about the customer will however have to be passed on to the respective service provider. When customer data are transferred by third parties, as a matter of principle, the issue of data protection must be considered on a national level.

Before organizational and technical measures are implemented in the companies concerned, it needs to be clarified whether a strategic revaluation of the product portfolio or the service offer for the product groups concerned must be performed. In this context it should be noted that especially the permits concerned can be traded by a large and diverse group of customers in regulated trading venues.

[1] See also MiFIR Art. 2 (1) No. 30, MiFID II Art. 4 (1) No. 44 c, MiFID II Annex I Section C Numbers 5, 6, 7 and 11.