.It would be negligent to simply make sweeping costs cuts-sustainable cost reductions require a holistic approach using the 3×3 method

If you see the IT of an institution simply as a large block of costs, it is easy to arrive at the statement that CIOs are often confronted with: “The IT is too expensive”. Based on top-down benchmarks this statement is not strictly wrong, but it is too undifferentiated to derive impetus for actions. The approach of reducing IT costs in an inconsiderate, radical manner by simply making cuts according to the principle that “20% are always possible” should be avoided by all means. Announcing an ambition level may certainly sensible and cuts across the board may bring about the desired short-term effects, but rash measures carry the risk of medium and long-term disadvantages. The “lawn mower” approach entails the inherent risk that the ORG/IT department as a facilitator for the realization of business targets may no longer be able to meet all expectations and requirements. Based on benchmark results for example, it is in fact recommendable to conduct a differentiated analysis of the IT costs in order to achieve long-term, sustainable effects.

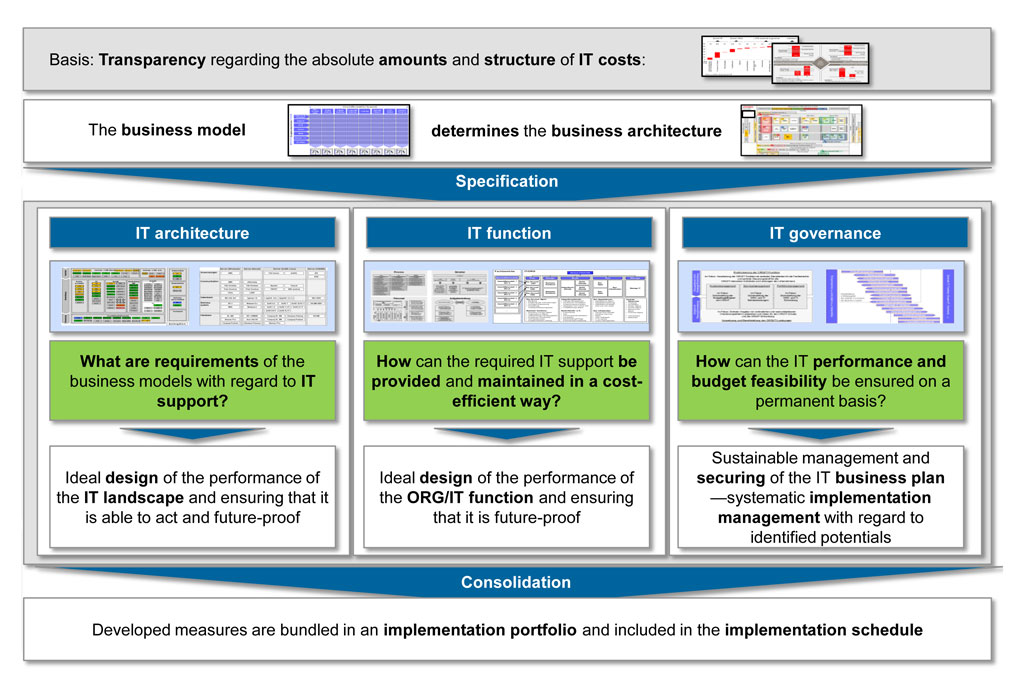

zeb’s experience has shown that a suitable method for a systematic analysis of IT costs is a three-step procedure that covers the three main IT core elements—a 3×3 method for a systematic IT cost analysis. The procedure starts by creating fundamental transparency regarding IT costs. Next, a detailed analysis of the three IT core elements set out below is conducted with the aim of identifying effective and sustainable cost measures in the following and transferring these into an implementation portfolio:

- Core element I: IT architecture—What are the requirements of the institution’s business models with regard to IT support?

- Core element II: IT function/organization—How can this IT support be provided in a cost-efficient way?

- Core element III: IT governance—How can the IT performance and budget feasibility be ensured on a long-term basis?

Figure 1: 3x3 method for a systematic analysis of IT costs

Figure 1: 3x3 method for a systematic analysis of IT costsStep 1: Creating fundamental transparency about IT costs

Creating transparency is the prerequisite for any kind of analysis. Thus, a comprehensive assessment of all IT costs in terms of their absolute amounts and structure constitutes the starting point of the detailed analysis. This may seem simple at first glance, but often this step already unveils some initial problems. This is due to the fact that—in addition to technical flaws in the execution of the structural assessment of the IT costs—total bank controlling and the ORG/IT unit often do not use a common definition of IT cost types. In the medium-term planning of the Controlling unit, it is not uncommon that IT costs are simply included as “one large block of costs” and thus, they are not transparent to anyone outside the IT unit. Moreover, a considerable share of IT costs is incurred in decentralized areas (e.g. in the business units)—this share of the costs needs to be considered as well. In addition to a lack of clarity regarding the composition of the IT costs (types of costs) / the cost units, the allocation of types of services and the conveyance of the IT services corresponding to these costs (e.g. service levels) is often insufficient.

A structural assessment of the IT costs offers not only transparency about the current cost level and its prospective development but also a benchmarking of costs against a suitable peer group. On the basis of the competitor comparison, it is already possible to develop initial ideas about the target cost level.

Step 2: Identification of cost drivers by means of a drill-down along the IT core elements (detailed analysis)

Core element IT architecture—Cost analysis for the application landscape

The transparency about IT costs that was achieved in the first step, differentiated by the different cost types, makes it possible to allocate costs within the application landscape in the next step. With the help of an explicit allocation, for example of license, sourcing and personnel costs to specific applications, a heat map can be created which reveals the cost drivers of the application landscape and their causes. By means of an analysis at cost type level, it is possible to detect unprofitable sourcing (e.g. operation of proprietary IT solutions for commodity business processes) and high maintenance costs, which indicate an inadequate architecture, and to develop specific starting points for the optimization. At the same time, the detailed cost analysis also allows for a comparison with competitors on the level of business fields. If the expenditure per business field is significantly above the benchmark value, this can be a first indicator for excessive overall “expectations” of the business units regarding IT equipment and should be taken as an occasion to rethink the current IT governance critically.

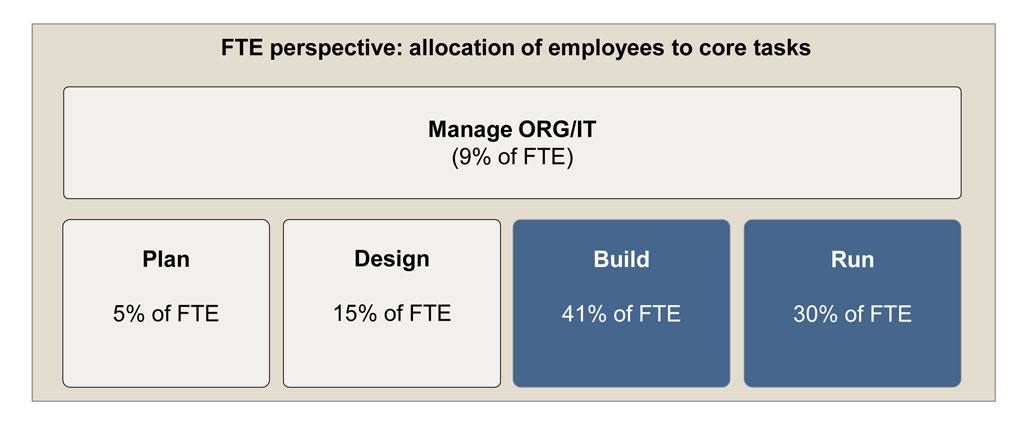

Core element ORG/IT function—Analysis of the structural and operational organization of the IT

The primary focus of the application landscape analysis is on material costs. However, personnel costs also account for a significant share of the IT costs. Thus, the analysis of the ORG/IT function focuses on an adequate utilization of personnel resources in comparison to the ORG/IT strategy and the sourcing strategy. For example, an extensive allocation of employee capacities to “build” and “run” to the disadvantage of “plan”, “design” and “manage” indicates a lack of an active solution management and an unclear sourcing strategy.

Figure 2: Client example: ORG/IT fulfilling the role of implementer and operator

Figure 2: Client example: ORG/IT fulfilling the role of implementer and operatorA strong and efficient ORG/IT function should look different. The detailed benchmarking of the ORG/IT function outlines whether the ORG/IT function—with its current available capacities and their allocation—is capable of putting sufficient emphasis on “manage IT” tasks (IT strategy, architecture, controlling or portfolio management) as well as “plan” and “design” tasks. It is important to define a clear IT and sourcing strategy and to allocate the capacities accordingly. Ultimately, the guiding principle for a powerful ORG/IT is to drive the innovative strength and productivity as well as the optimization of the use of applied solutions and processes and to manage them sustainably in a proactive manner and in close collaboration with the business units. In this context, also refer to the BankingHub article by Schick/Behrmann 2014: The right setup of ORG/IT leads to corporate success.

Core element IT governance—Analysis of management mechanisms for the IT

A lacking or insufficient governance for ORG/IT deployment in the institution can be a significant cost driver with direct implications for the IT core elements “architecture” and “function”. This shows that, at the end of the day, optimization efforts can only be successful and sustainable if they are laid out in an adequate governance. If the ORG/IT function used to act as an “implementer and operator” as described above, a mere reallocation of employee capacities is not going to improve the situation. On the contrary: if the governance structures remained unchanged, this would inevitably lead to resource bottlenecks for “build” and “run” tasks, resulting in operational risks combined with unpredictable costs.

Thus, it is necessary to incorporate the optimization in the bank’s governance as well. In an active role, the ORG/IT function ideally acts as a central interface between business unit and provider. It is the only way in which the governance can fulfill its actual function, i.e. ensuring budget feasibility and sustainable IT cost management. For this purpose, appropriate new management processes and collaboration models should be established within the ORG/IT function and at the interface with business units and providers. This also includes suitable cost planning and management processes that make it possible for the business units to influence their ORG/IT costs in the short and medium term. The “black box” IT costs has to be opened, in order to enable the business units to calculate their utilization of IT in the business field strategies, e.g. by means of a transparent and cause-based IT cost allocation based on clear service commitments of the ORG/IT function.

A lack of transparency regarding IT costs and a state where there is no cause-based allocation of IT costs to the business units placing the corresponding orders only lead to the rash conclusion that “the IT is too expensive”, if it is not possible to establish connections between the IT costs incurred and the corresponding services that have been rendered.

Step 3: Summary of the required measures and the implementation schedule

A detailed look at the three core elements shows clearly that a cost optimization should not be conducted by means of isolated measures but rather across all areas. Mutual interdependencies require a holistic view and turn a sustainable optimization into a complex undertaking. Especially a comparison with competitors and experiences regarding typical cost drivers can offer the necessary orientation in this context. By means of best practices, it is possible to conduct a systematic review of the own cost situation and to derive appropriate optimization measures and bundle these in an implementation schedule that runs parallel for all IT core elements.

Only a synchronized optimization along the IT core elements architecture, ORG/IT function and governance makes it possible to break the cycle of optimization and gradual deterioration until the next optimization initiative.