Forms of financing and growth

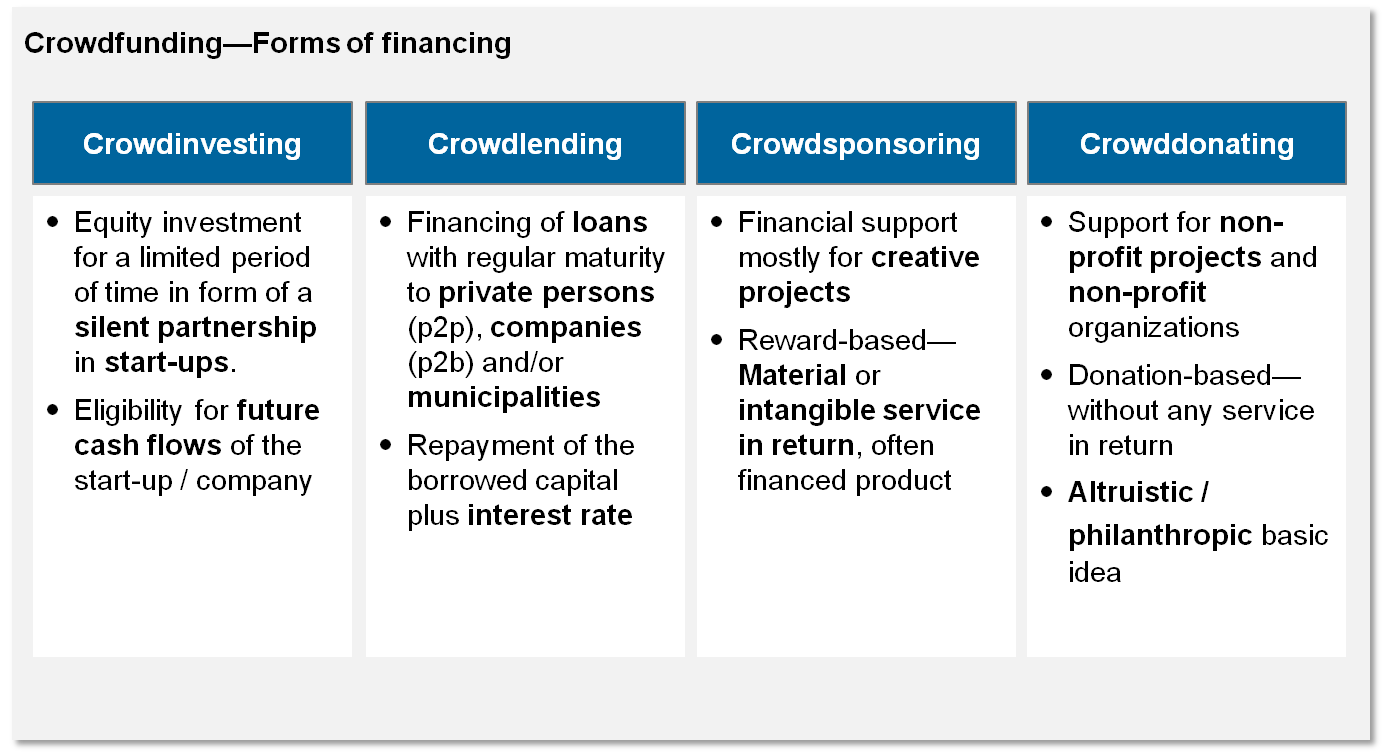

The term crowdfunding generally comprises four different financing models, which are characterized by the respective return service for the investor. Figure 1 illustrates the major differences between the individual approaches.

Figure 1: Financing models of crowdfunding

Figure 1: Financing models of crowdfundingExamples of crowdinvesting may be Seedmatch and companisto, while Lendico offer crowdlending, Startnext offer crowdsponsoring and Betterplace offer crowddonating. A comprehensive overview of existing crowdfunding platforms is, for example, provided under Crowdfunding.de.

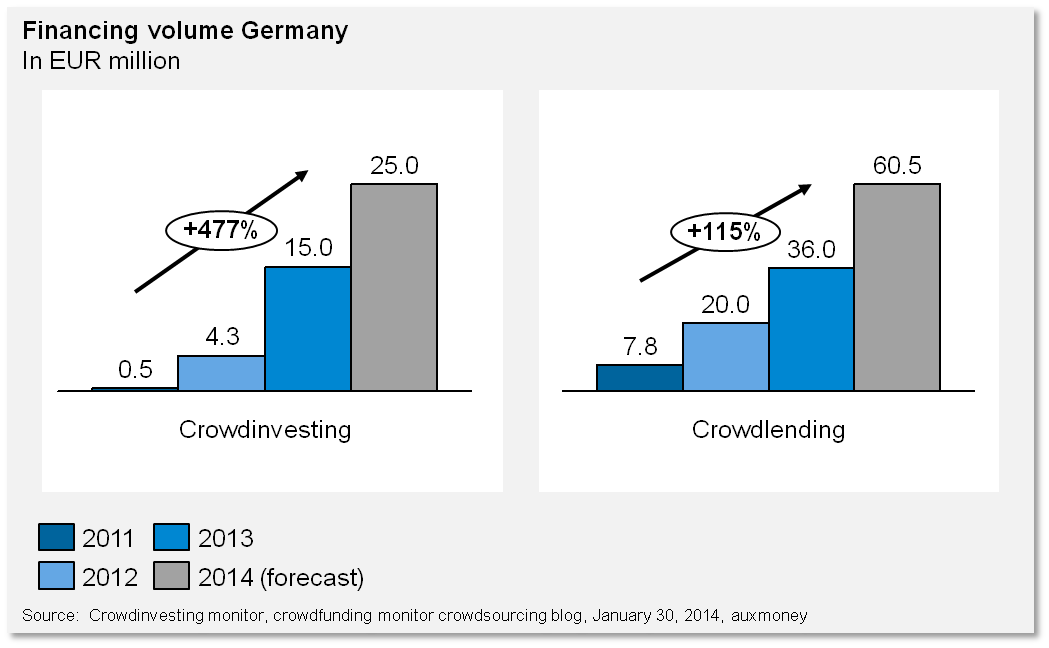

The crowdfunding market is characterized by major growth. Crowdinvesting and crowdlending can especially tie in the functioning of a bank due to their design based on equity and external funds. Both forms of financing were able to report strong growth of ~480% and ~115% in Germany between 2011 and 2013. According to forecasts, this trend will continue in 2014 (see figure 2).

Figure 2: Growth of financing volume through crowdfunding across Germany

Figure 2: Growth of financing volume through crowdfunding across GermanyRisks and regulation

The crowdfunding model has been spared from too strict regulations so far, which, above all, might relate to the manageable financial volumes. Looking at the trends in the USA, which have already become active in terms of legislation, a stronger regulation of business isn’t likely. A new law eased, on the one hand, the registration and prospectus requirements, that go hand in hand with a significant cost reduction for start-ups, and on the other hand induced a regulation of investment limits, that are to ensure the protection of investors. The European Commission announced to further tap into crowdfunding potentials in Germany.

It will be interesting to watch developments that occur when a high-volume financing cannot be repaid on one of the platforms, thereby entailing a large amount of aggrieved investors. Thus, the Prokon insolvency for instance led to initiatives of several federal ministers to regulate the so-called “gray capital market” more strictly (see FAZ, 05/22/2014 Mehr Schutz auf dem „Grauen Kapitalmarkt“).

Implications for banks

Several financial institutions have already become active and have shown how crowdfunding can be individually used for the business model. The platforms “BW Crowd” of BW Bank and “Viele schaffen mehr”, a platform of a cooperation of VR banks, rely on crowddonating and enhance social projects in the respective operating district. Therefore, the principle of regionality is even more integrated in the business model. Whereas Berliner Volksbank is shareholder of a platform, Fidor Bank, which is already active in the web 2.0, goes one step further and directly cooperates with several crowdfunding platforms. These are integrated in the Fidor bank system via an app and are thus easy to access for customers. This means, Fidor Bank acts without an own crowdfunding platform, but can benefit from the aforementioned advantages and therefore offer added value for its customers.

The volumes of projects that have been financed through crowdfunding are still manageable. Banks aren’t under pressure to act with regard to the low market share. However, the sector is changing. Many crowdfunding platforms are still in their identification stage, only some of them will establish themselves on the market and increase their values. The trend of this topic is to be observed in future as well as challenges and opportunities that could be used for financial institutions on a mid or long-term basis.