Payments market: Status quo

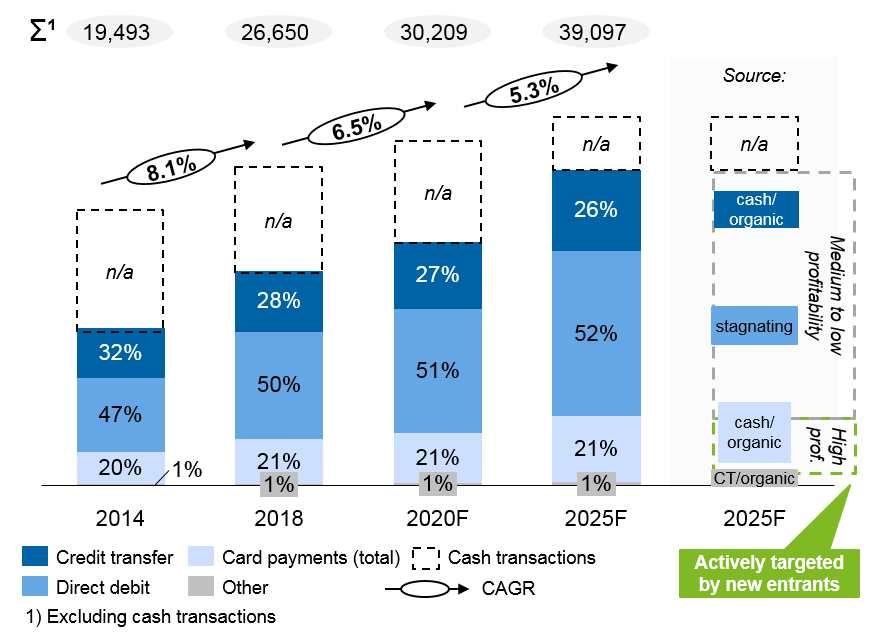

Looking into transactional numbers for Germany and Austria, the overall market size in 2018 accounts for around 27 billion cashless transactions p.a., with a continued slower growth expected in the future. Around two-thirds of the growth in number of transactions will result from the shift from cash to cashless and one-third will arise from the economies’ organic growth.

A vast number of options on the market offers customers the possibility to easily switch not only providers, but also types of transactions they are executing (with the recent rise of e-money as a good example). This results in an emerging trend among current consumers to switch from profitable towards less profitable transactional segments (see Source bar below). In addition to increasing competition (especially in the growing fintech community) within already shrinking profitable segments, this poses another threat to the bank’s top line.

Figure 1: Of cashless payment transactions in Germany and Austria (in million), ECB

Figure 1: Of cashless payment transactions in Germany and Austria (in million), ECBTaking the assumed 2025 transactions, we believe that about 20% of the overall volume will represent high profitability business, which will be targeted by new entrants such as big tech and fintech companies and neobanks, leaving incumbent banks with less or even non-profitable business.

Structural changes in the industry

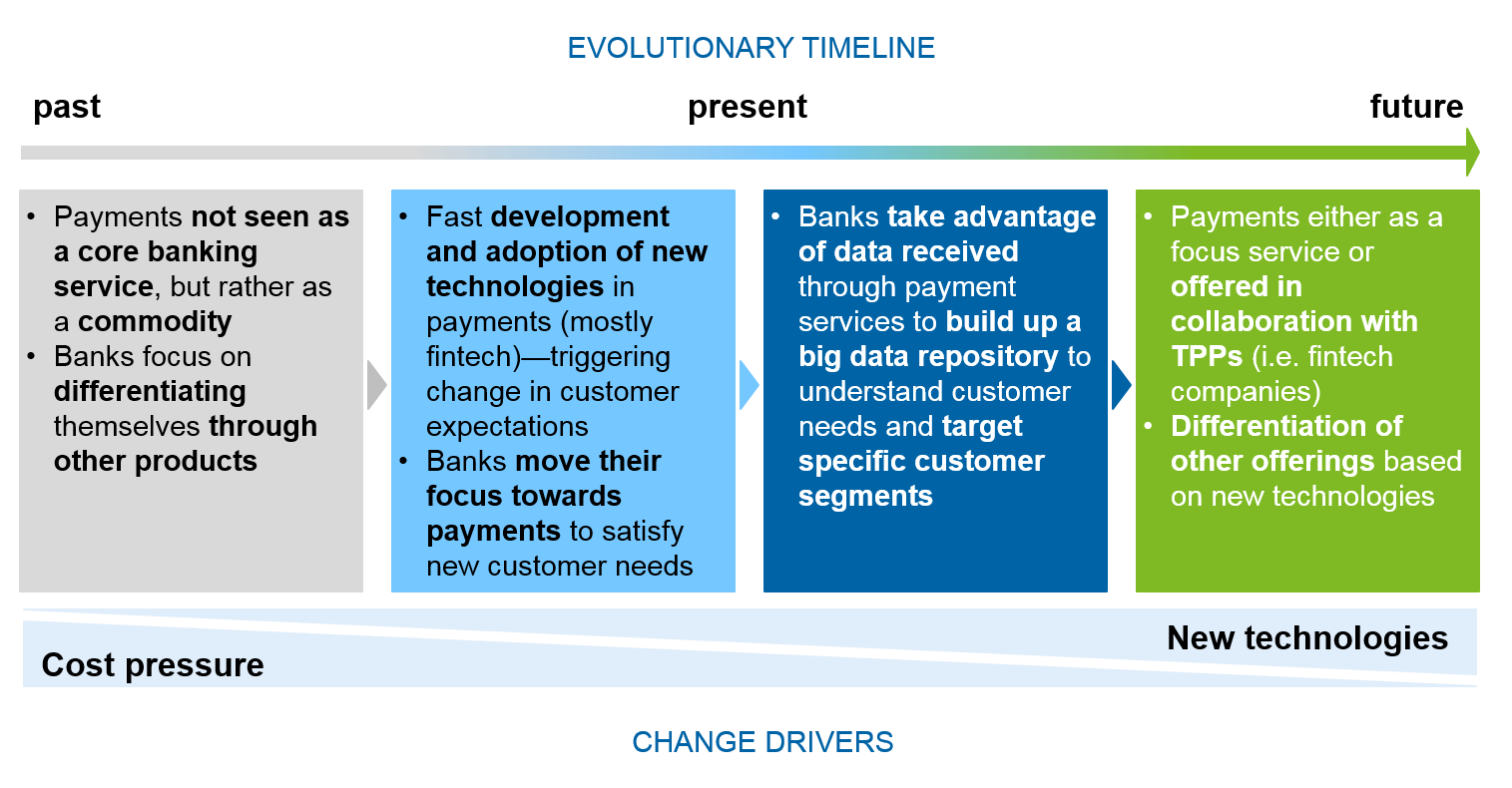

The strategic role of payments in banks’ product portfolios is gaining significance due to the development of new technologies, the rise of new market players and the variety of innovative offerings available. These are the major triggers for changes in customer expectations, which are now directed towards a more convenient service and seamless experience.

Consequently, payments have the potential of becoming more of a differentiating service and less of a commodity good. One upside for banks embarking on such a shift in “payments mentality” is the resulting abundance of customer data available for creating targeted offerings for specific customer segments. This is only one of many aftereffects of the latest technological developments and the same impact is expected to be noticed also in other product areas.

Figure 2: Change drivers in the industry over time

Figure 2: Change drivers in the industry over timeConsequently, banks cannot give up or just outsource their payment business without risking the customer interface as such.

Challenges and how banks should respond

As to cards and payments, banks will be facing several challenges in the next couple of years. As a result, the share of revenues from payments in the total revenue of banks is expected to decrease by 10%. Major drivers include:

- pressure on margins in the EU expected, since banks need to give up their fees on cross-border payments in non-euro area countries;

- increasing competition due to the entrance of new players providing advanced and innovative financial technology;

- increasing regulatory requirements for data management, AML/KYC checks, cybersecurity, etc.;

- changing customer expectations requiring better targeted offerings and a differentiated service, which put additional pressure on the bottom line.

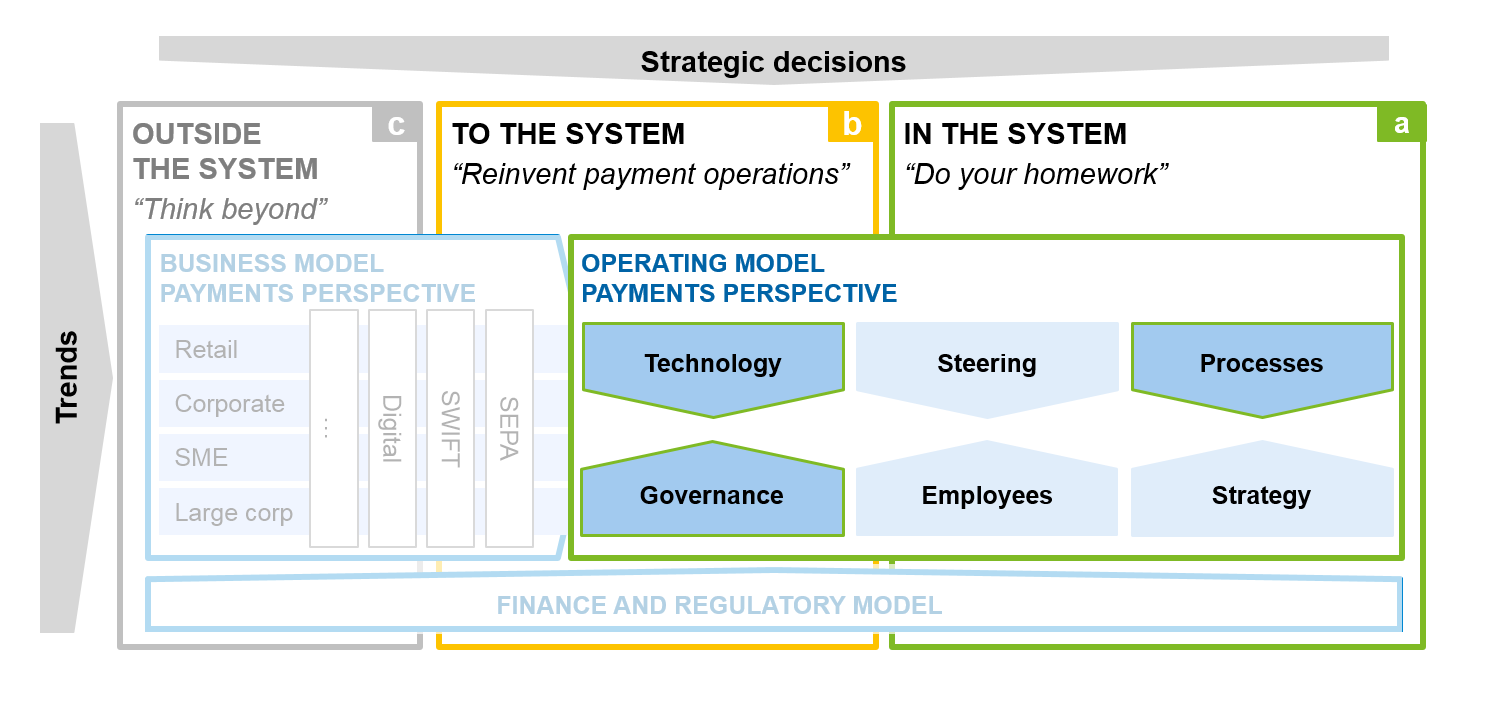

In order to cope with these challenges, banks will need a more flexible operating model. Going forward, banks should be able to support commodity products from a lower cost base and differentiate service quality in their processes including the possibility to integrate third-party services. Operating model changes require banks to act both “in the system” and “to the system” (see our zeb transformational change diagram below).

Figure 3: Operating and business model – payments perspective

Figure 3: Operating and business model – payments perspectiveKey success factors for the future are:

- a collaboration enabling governance

- adoption of new technologies

- efficient processes as service differentiators

Governance

Since the payment business is no longer restricted to banking only (mostly a consequence of regulation), changes in the governance of payment products are required. The general focus will be moving from setting up internal procedures to partner management, aimed at enabling collaboration with TPP[1]s. From zeb’s point of view, banks will need third-party providers who integrate further partners and vice versa to excel in the future “open banking” market. Such collaborations range from completely outsourcing this area of business to simply adopting new technologies (e.g. distributed ledger technology, DLT) for faster, securer and cheaper settlement. A possible way of designing the new governance model is to switch payments from being managed within segments and transfer them into a separate organizational unit responsible for partner management, while the responsibility for very specific cases (or customers) rests with the relevant segment depending on their size, volume, contribution margin, etc.

Technology

Talking about changes in technology also linked to collaboration with TPPs, banks need to make sure their IT architecture is flexible enough to easily adopt new technologies and integrate new solutions into their current landscape. One of the most common ways to achieve this is to establish a BPM[2] layer (which should also enable the exchange of data with third parties) by separating processes from the systems in use. This way, banks can not only avoid changing processes after every system change, but can also manage them more efficiently, and finally, prepare their infrastructure for the integration of forthcoming technological solutions (e.g. KYC and settlement on DLT, AML through artificial intelligence, etc.) for faster payment processing.

Processes

When it comes to processes, organizations have been focusing on optimizing their throughput times, i.e. increasing their STP[3] rates. Process-based costing gained even more importance during the post-crisis times in 2008 when banks were forced to increase transparency about their fees and as a consequence needed to find ways for optimizing their bottom line. While not much can be done on the customer’s side to reduce pauses and breakdowns in transaction processing (missing/invalid information, duplicated orders, insufficient funds, etc.), on the bank’s side—apart from obvious measures (reduction of multiple approval layers or exchange rate orchestration) – a strategic approach is needed.

Banks will need to establish selection criteria based on an effort-to-output approach by looking into contribution margins of different payment types and their costs to serve (i.e. costs of execution, settlement, etc.). Processing low-margin orders should either be outsourced or highly standardized. Significant manual effort should be reserved for products with higher contribution margins.

Consequently, a high level of standardization allows for process automation, thus resulting in higher STP rates and efficiency increases (zeb has a market-proven approach to STP implementation, learn more here).

As the operating model is ready for the next step, further changes are coming from “outside the system”, thus requiring a change in the business model itself. The classic approach would be to change the business model first. But this time, it is different: the operating model needs to enable a set of possibilities on which the business can build new product/service models.

In five to ten years, we will be living in a slightly different banking market. PSD2 regulation has brought to life the hot topic of open banking, i.e. the banks’ anticipation of their role in the new world of payments and beyond. We will keep publishing on open banking developments, so stay tuned.