West. European banks defy capital market downturn

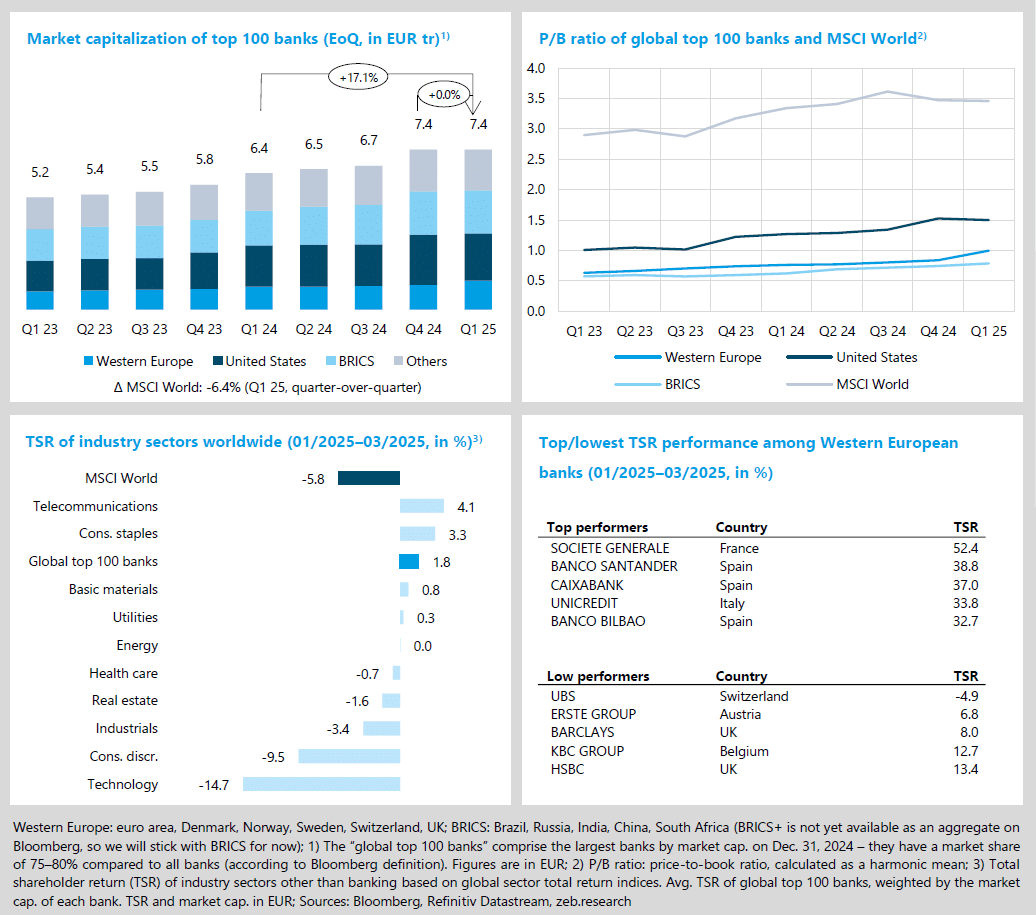

- In Q1 25, the global capital markets experienced a dip (MSCI World market cap. -6.4% QoQ, TSR -5.8% QoQ).

- Western European banks (TSR +20.8% QoQ, USA -5.2% QoQ) offset the capital market performance of the global top 100 banks (TSR +1.8% QoQ).

- At the end of Q1 25, Western European banks achieved a price-to-book ratio (P/B ratio) of 1.00x for the first time since Q3 17.

- If the US tariff policy presented on April 2, 2025, materializes, further significant declines are to be expected on the capital markets worldwide.

German borrowing package drives up EUR int. rates

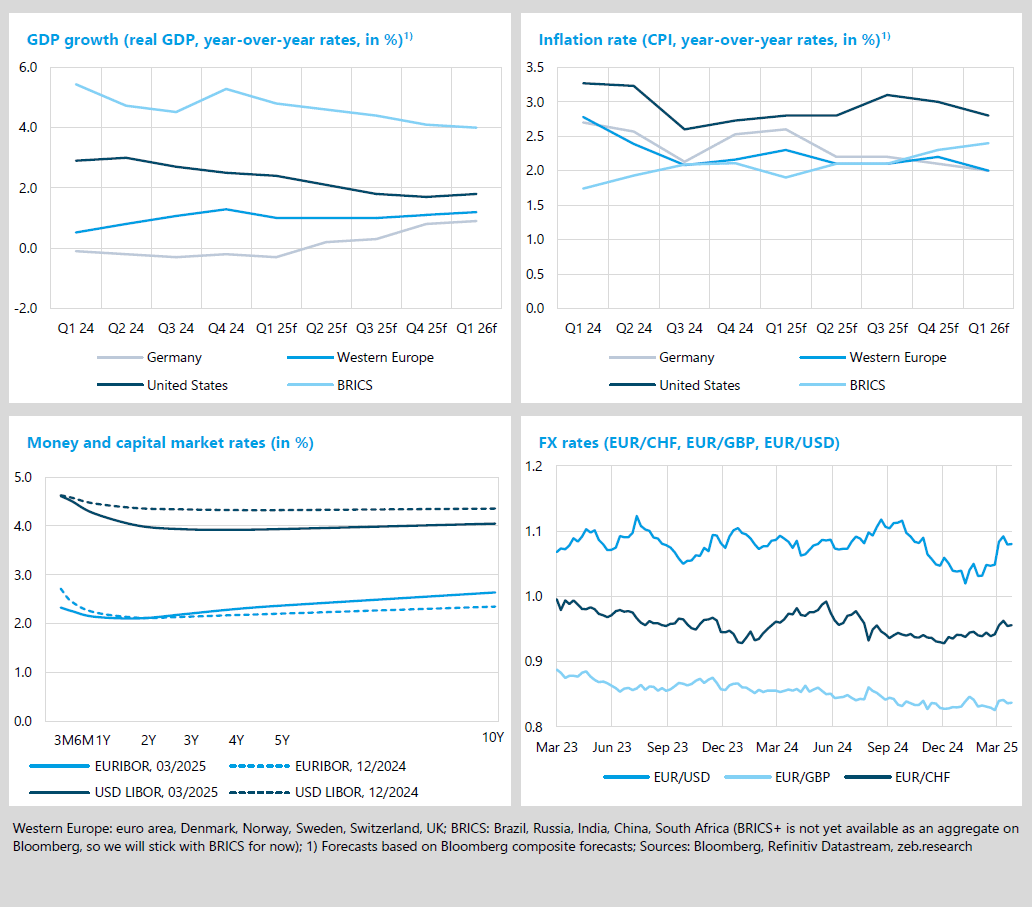

- Inflation in Germany is expected to rise slightly to 2.6% YoY in Q1 25. As to GDP, analysts expect a shift of -0.3% YoY – the seventh GDP decline in a row.

- The inverted yield curve in the euro area normalized in Q1 25 after a long time in light of increasing returns at the “long end”.

- Banks are already adapting to the new interest rate environment. They are raising their mortgage interest rates and thus end the short-lived downward trend. Deposit interest rates continue to fall in line with the ECB’s expected interest rate cuts.

Start of a transatlantic divergence between the USA and Europe

After a euphoric Q4 24, the global capital markets experienced a dip in Q1 25 (MSCI World market cap.

-6.4% QoQ). These negative developments have been driven by the US markets. With its global confrontational policy and transactional style of governing, the Trump administration has caused great uncertainty and economic turbulence. In contrast, the investment package for defense and infrastructure recently adopted in Germany is an attempt to provide significant growth momentum for the largest economy in Western Europe. The top 100 banks reflect this development. The rapid increase in market capitalization in Q4 24 was still attributable to the US banks. In Q1 25, the positive TSR performance (+1.8% QoQ) was largely induced by Western European banks (+20.8% QoQ) (USA -5.2% QoQ, BRICS +2.5% QoQ).

- The price-to-book ratio of Western European banks increased significantly by +0.16x QoQ in the wake of the strong capital market performance in Q1 25 and reached the magic threshold of 1.00x for the first time since Q3 17 (USA -0.03x QoQ to 1.50x).

- The historic US tariff announcements from April 2, 2025, were barely priced into the Q1 25 figures, and the most pessimistic market expectations have now been exceeded. This has led to considerable price corrections on April 3 (vs. Q1 25) (MSCI World TSR -5.4%p, top 100 banks -5.8%p). US stocks and companies with significant US business are particularly affected.

- With a TSR of +52.4% QoQ, Société Générale is the Q1 25 top performer in the ranking of Western European banks. Based on a profit of EUR 4.2 billion in 2024, the bank achieved an increase of more than 60% compared to the previous year. UBS brings up the rear, as its valuation was recently downgraded by analysts due to uncertain future capital requirements (TSR -4.9% QoQ).

Trump and German fiscal package could delay interest rate cuts

With expected negative GDP growth of -0.3% in Q1 25, Germany is facing its seventh consecutive quarter of declining economic performance. The effects of the latest US tariff policy, which are not yet included in the forecasts shown, are likely to severely temper the cautiously optimistic growth expectations for Germany and Western Europe and significantly accelerate the decline in US GDP growth. Whether Germany and Western Europe will actually achieve the forecast target inflation rate of 2.0% in Q1 26 remains questionable given the rapidly changing world order. The plans presented on April 2, 2025, are like a “nuclear bomb on the global trading system” (Ken Rogoff, former chief economist at the IMF), driving US inflation expectations and thus limiting the scope for the US Fed in particular.

- Despite the foreseeable achievement of target inflation, the inflation rate in Germany is expected to rise slightly in Q1 25 by +0.1%p to 2.6% YoY (Western Europe +0.1%p to 2.3% YoY).

- The emerging transatlantic divergence is also reflected in the EUR and US dollar yield curves in Q1 25. While US long-term interest rates fell, the long end of the euro area yield curve rose on account of the agreed German borrowing package, which led to a steeper EUR yield curve. Market players expect the ECB to lower the EUR key interest rate by a further 0.25%p on April 17, 2025. Good news from a European banking perspective: this brings back the possibility for generating income from maturity transformation.

- The euro appreciated in Q1 25. Markets expect higher returns in the euro area thanks to an increased demand for investment, which boosts the attractiveness of investments in euros. Initial market reactions to April 2, 2025, point to further significant EUR appreciation and USD depreciation.

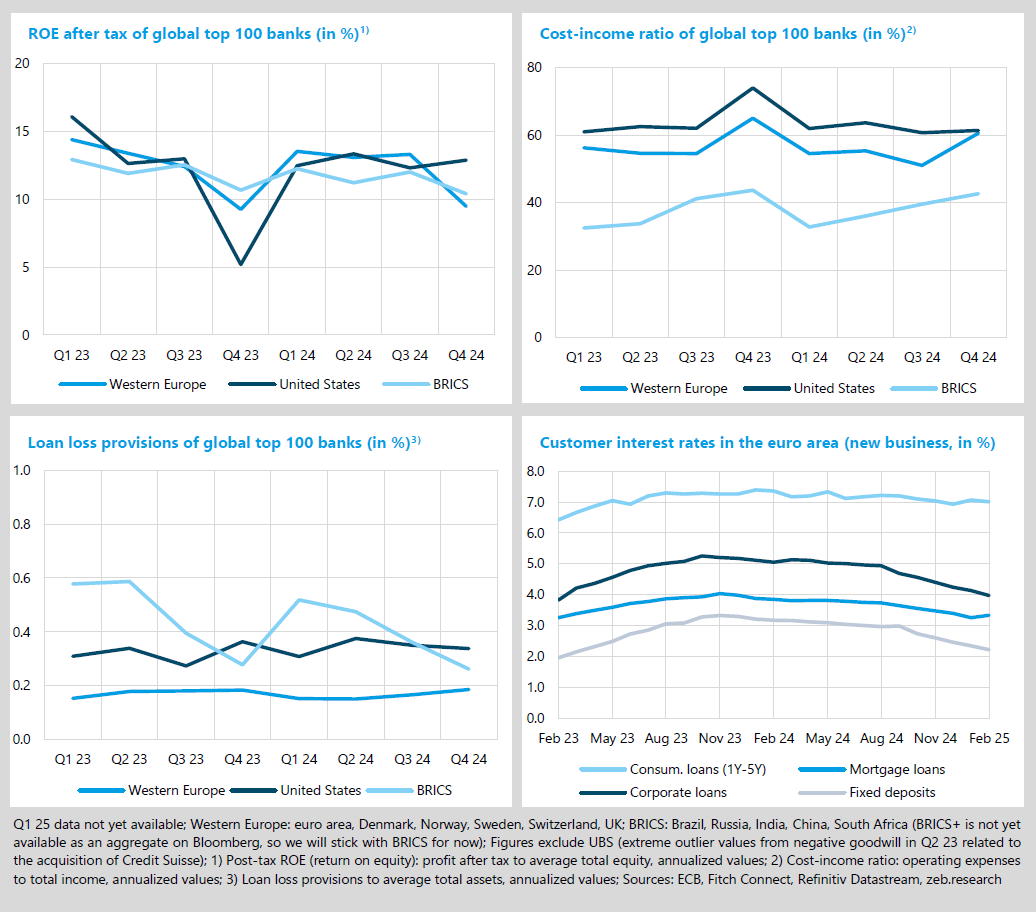

In Q4 24, US banks increased their ROE slightly by 0.6%p QoQ to 12.9%, again taking first place in a comparison of the regions (Western Europe 9.5%; BRICS 10.4%). US banks benefited in particular from falling short-term interest rates, which caused interest expenses to drop more drastically than interest income. The ROE decline among Western European banks of -3.8%p QoQ is attributable to a loss of profits of -28.7% compared to the previous quarter. This is mainly due to Q4 one-off effects, with HSBC (again) reporting high one-off effects in Q4, which resulted in a significant QoQ loss of profits (decline excluding HSBC

-18.6%). However, compared to the same quarter of the previous year, Western European banks’ net income increased by +9.1%.

- Western European banks reported a rise in their cost-income ratio of +9.5%p QoQ to 60.6% in Q4 24. This was caused by a +26.7% increase in costs compared to the previous quarter, while income increased only slightly (+6.8% QoQ). The cost-income ratio of US banks was subject to only minor fluctuations in 2024 and rose slightly by +0.7%p QoQ to 61.4% (BRICS +3.1%p to 42.7%) at the end of the year.

- Over the course of 2024, Western European and US banks made only small adjustments to their risk provisioning. At the end of Q4 24, Western European banks increased their loan loss provisions by +2 bp QoQ (US banks -1 bp QoQ, BRICS -10 bp QoQ). In light of the high level of (geo‑) political uncertainty, the volatile economic situation in the USA and the announced tariffs, the topic of risk provisioning could be placed higher on the agenda for 2025.

- At the start of Q1 25, customer interest rates in the euro area continued to decline. However, the data does not yet fully reflect the effect of the German borrowing package and the US tariff announcements, which have caused long-term interest rates to rise and are therefore supposed to disrupt the trend, particularly with regard to mortgage loans.