Bancassurance, as a strategic sales collaboration between banks and insurance companies, has firmly established itself as a promising business model in Europe. Despite the current stagnation in the German market, some institutions still have untapped sales potential.

In this article, we highlight the current challenges faced by cooperation partners and the current market trends.

Bancassurance at a glance

By European standards, the German bancassurance market is stagnating. This trend is mainly due to a recent slowdown in new life insurance business and the inadequate integration of insurance products within banking processes.

Many medium-sized credit institutions have significant untapped earnings potential, with the possibility of doubling bancassurance commission income compared to leading competitors by enhancing customer share of wallet in the insurance business.

Key cornerstones of a successful cooperation are deeply integrated IT solutions, such as the joint development of digital platforms by the banks and their insurance partners, as well as sales through embedded insurance.

How big is the international bancassurance market?

The international bancassurance market is booming and shows no signs of slowing down. In 2023, the global market volume reached USD 1.4 trillion. Experts predict that by 2030, premium income could rise to USD 2.1 trillion, reflecting an annual growth rate of 5.5%. The bancassurance model has become particularly popular in Europe.

In countries such as France, Italy, and Spain, more than half of all life insurance policies are now sold through banks.

How big is the German bancassurance market?

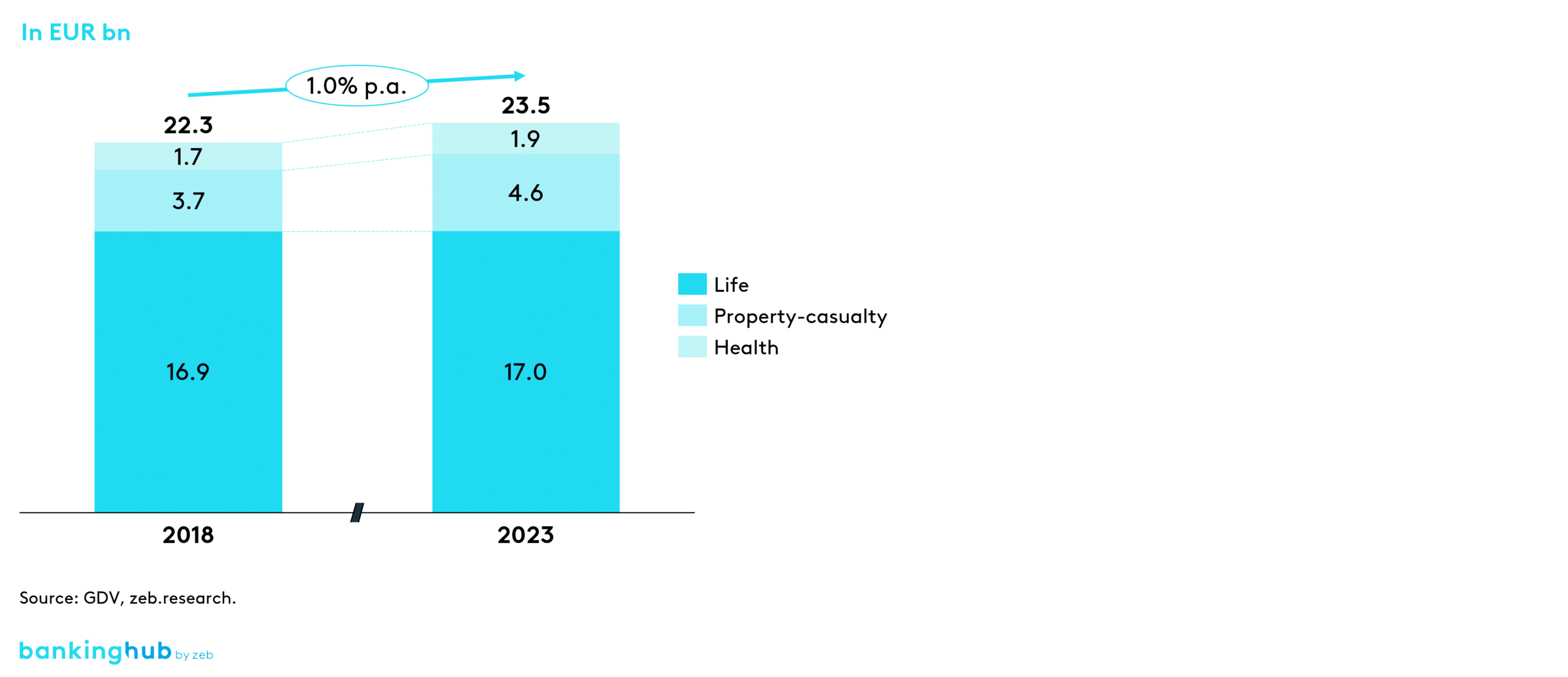

The German market, however, is lagging behind, with growth of just 1% per year to date and a total gross premium income of around EUR 23.5 billion in 2023. Life insurance represents the largest share of the German bancassurance market. In 2023, it accounted for approximately EUR 17 billion, making up about three-quarters of the total bancassurance-specific premium volume. New business, however, has weakened in recent years. The rise in interest rates, in particular, has made banks’ deposit products more attractive, posing challenges for banks to generate new business in life insurance.

Meanwhile, property-casualty insurers significantly increased prices in response to inflation, which also impacted premiums in bancassurance sales. At EUR 4.6 billion, these insurance policies represented 20% of the market in 2023, but still have potential. Product penetration in this segment is often only half the level of life insurance. Additionally, commissions from the property-casualty business offers a stable source of revenue that is hardly affected by current interest rate trends and does not compete with other banking products.

Health insurance has experienced moderate growth in the bancassurance market in recent years. However, this type of insurance plays only a subordinate role, accounting for around 8% of the premium volume in 2023.

Figure 1: Development of gross premiums written in the German bancassurance market

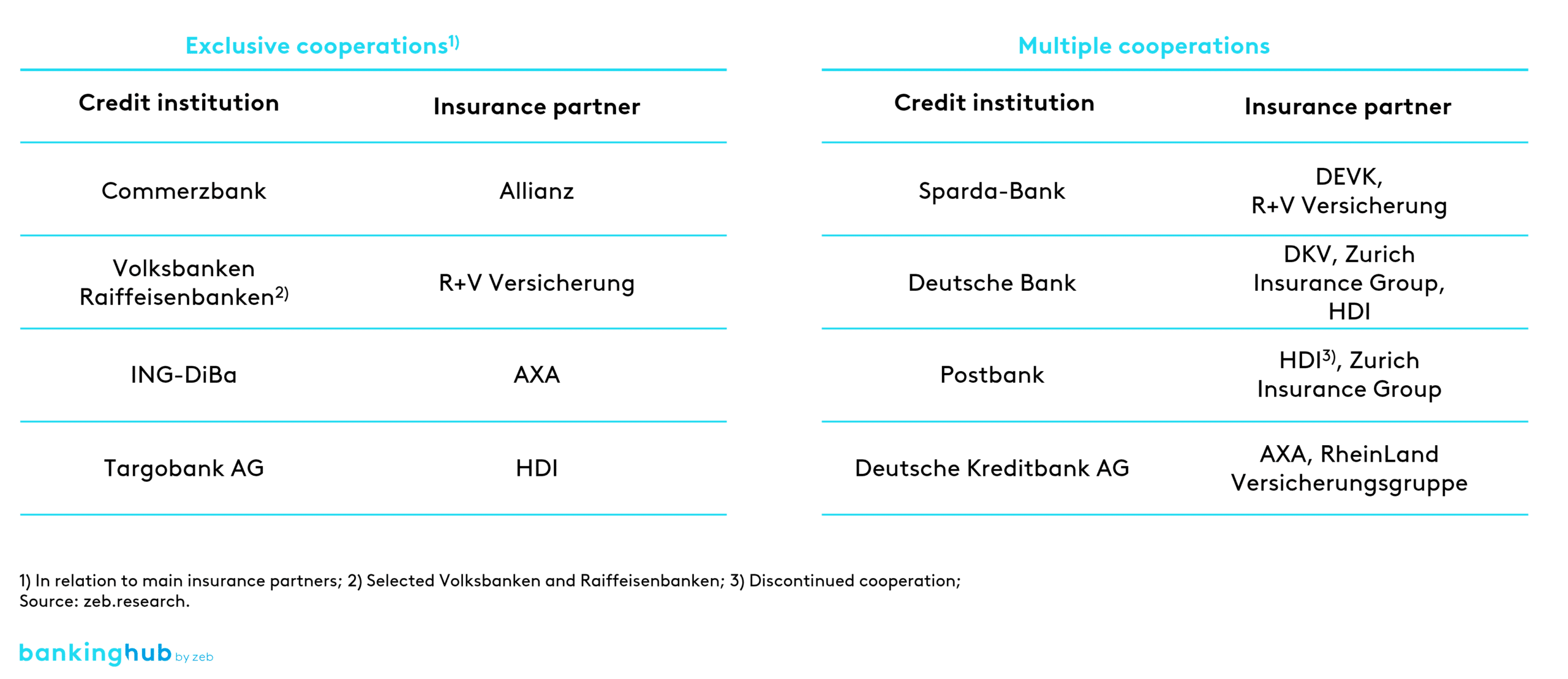

What types of bancassurance partnerships exist?

In Germany, banks and insurers work together in various ways to offer their customers a wide range of financial products. There are two main types of cooperation: exclusive cooperations, where a bank collaborates solely with one insurer, and multiple cooperations, where a bank engages with several insurers at the same time.

Figure 2: Overview of selected bancassurance cooperations in the German market

What untapped potential is there for banks?

Success stories in the German bancassurance market vary widely. While some retail banks generate significant commission income through this channel, other institutions fall short of their expectations. Comparing an average medium-sized bank with its leading competitors, the zeb.Retail Banking Study shows that in many cases there is potential to double commission income from bancassurance.

The key success factor is to systematically increase customer share of wallet. The actual exploitation of this potential, however, largely depends on the bank’s strategic objectives, the breadth of its product portfolio and the effectiveness of its customer and sales structures.

A 2021 study conducted by Bankenforen Leipzig and Versicherungsforen Leipzig underscores this potential: around 25% of surveyed customers prefer banks as a sales channel for insurance and expect to be actively approached about suitable products. What is striking, however, is that more than a third of those surveyed have never been contacted by their own bank about insurance offers – a further indication of untapped sales potential.

What are the current challenges in the bancassurance market?

Despite the international success of bancassurance, its potential often remains untapped in Germany. But why is that? What are the factors that make some banks more successful than others?

In many German banks, insurance services are not seamlessly integrated into the banking system. While other European markets have already invested in bancassurance platforms and joint sales strategies, German institutions lag behind. The result is a fragmented customer experience and an inefficient sales structure.

In addition, German banks often lack a strong link between sales and insurance expertise. While employees specialize in banking products such as accounts, loans and investments, selling insurance products requires specific sales expertise and advisory strategies. There is often a lack of targeted training and further education to impart this knowledge.

Investments in personnel development, dedicated advisory teams and modern technologies are either absent or insufficiently dimensioned. As a result, bank advisors are reluctant to deal intensively with insurance products and to actively approach customers. Financial incentives are also limited, as there is no direct participation in sales success.

What trends are emerging in the bancassurance market?

The bancassurance model in Germany is currently undergoing a transformation, driven by technological innovations and new market requirements. While some of the potential remains untapped, there are promising approaches to successfully integrate banking and insurance services.

More flexible sales strategies and digital platforms, which are being developed in cooperation between banks and insurers, offer new opportunities. Insurance manager apps give bank customers a convenient overview of their insurance coverage and can also transfer third-party contracts from other sales channels to their bank.

Another development is the direct integration of insurance services into banking products. Examples such as automatic purchase protection insurance for current accounts show how embedded insurance is finding its way into the bancassurance sector. Integrated cyber insurance, which protects against identity theft or fraudulent use of banking information on the Internet, also greatly simplifies the purchasing process.

As regulatory requirements tighten, banks and insurers are increasingly focusing on compliance and data protection. There is also a growing demand for sustainable products. Successful bancassurance partnerships are therefore increasingly focusing on offers that not only meet financial, but also environmental and social criteria.

Taking advantage of these trends requires targeted action. Read our article on success factors and best practices to learn more about what makes a successful strategic partnership between banks and insurance companies:

FAQ: You should now be able to talk about these key points of the article:

Why is the German bancassurance market stagnating? Growth in the German bancassurance market is faltering due to weak new business in life insurance and the inadequate integration of insurance products into banking processes. The rise in interest rates has made banks’ deposit products more attractive, posing challenges for banks to generate new business in life insurance.

What are the challenges in the German bancassurance market? Insurance services are often not seamlessly integrated into banking systems, resulting in a fragmented customer experience. There is also no strong link between sales and insurance expertise. Bank advisors need targeted training and further education in insurance sales.

What is the role of sustainability and compliance in the bancassurance sector? Successful bancassurance partnerships are increasingly focusing on offers that not only meet financial, but also environmental and social criteria. Compliance and data protection requirements are becoming increasingly important in the face of stricter regulatory requirements.

What are the key factors for a successful bancassurance cooperation? Decisive factors include deeply integrated IT solutions, the joint development of digital platforms, sales through embedded insurance, close integration of sales and insurance expertise as well as targeted training and further education for bank advisors.

Many banks and insurance companies are stagnating in the German bancassurance market. What differences exist between successful and less successful collaborations? And what factors decisive for the success of bancassurance cooperations?

Analyses, articles and interviews about trends & innovation in banking delivered right to your inbox every 2 weeks

"(Required)" indicates required fields

You are currently viewing a placeholder content from Vimeo. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.