Although Germany is known as a cash-dominated economy and the number of mobile payment transactions is still very low, especially in comparison to other countries in Europe, e.g. Sweden, more and more players are offering mobile payment solutions.

Back to main article: “The future of mobile payments in Germany”

A heterogeneous Mobile payment market in Germany

The reason for this is the growing digitalization level, changes in customer behavior and the advent of the PSD2 regulation. The German mobile payment market is heterogeneous, not only from the perspective of different types of solution providers, but also when looking at the deployed technologies such as NFC or QR codes.

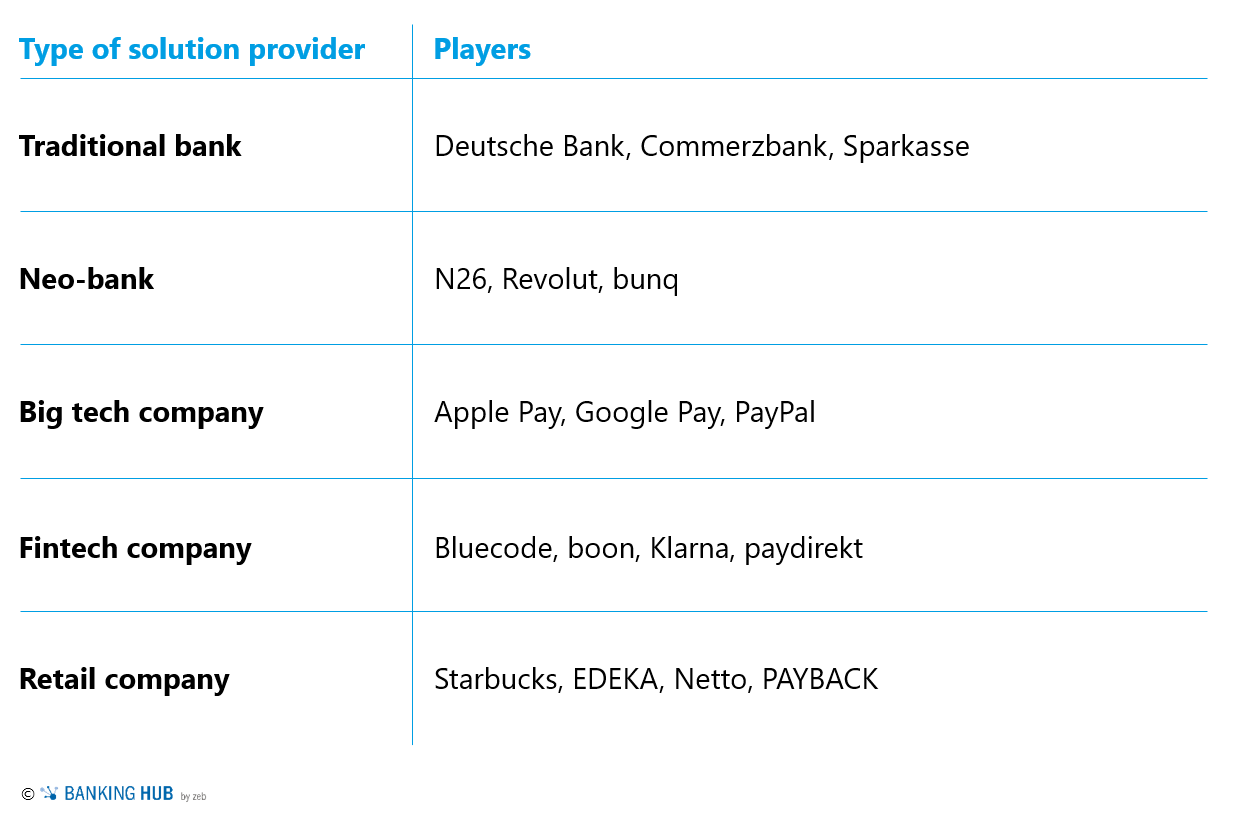

Figure 1: Most significant players offering mobile payments in a wider sense (including contactless payments, online payments and/or P2P payments) in Germany

Figure 1: Most significant players offering mobile payments in a wider sense (including contactless payments, online payments and/or P2P payments) in Germany- Traditional banks are facing rapid disruption. In order to retain customers, they have to adapt to new standards, switch from old-school players to operators who provide mobile banking to their customers, often in cooperation with digitally advanced fintech companies. Deutsche Bank and Sparkasse are the only two banks in Germany offering their own mobile payment solutions[1]. A number of different banks provide mobile payments through partnerships with Google Pay and Apple Pay. Commerzbank, for example, is partnering with Google Pay to offer mobile payments, but independently offers P2P payments.

- Neo-banks differentiate themselves by offering a 100% digital banking experience and ease of use. Main players include Revolut, bunq and Germany-based N26 bank, which is currently being used by over 5 million customers in 25 countries. These players still do not offer their own mobile payment solutions (instead they rely on respective partnerships with big tech companies), but they provide some innovative functionalities, such as budget management and bill splitting.

- Big tech players, represented by Apple Pay and Google Pay, are dominating the German mobile payment market. The two market leaders in Germany, Apple Pay and Google Pay, do not process payments themselves, both are based and dependent on debit and credit cards. Apart from online payments, they do not offer any additional significant functionalities, but are the only two solutions widely accepted by merchants. Like neo-banks, their solutions are delivered through a highly technologically sophisticated and very user-friendly interface—propably their biggest strength besides their large customer base.

- Fintech players such as Bluecode, boon and paydirekt offer payment schemes that enable cashless payments with merchant-driven value-added services. paydirekt is a mobile payment solution with 3.2 million registered customers that has been launched by a consortium of German banks as an alternative to PayPal, offering e-commerce and P2P payments. Despite the large number of registered customers, paydirekt has not yet gained traction in the German market.

- Retail players, such as Starbucks, EDEKA, Netto or PAYBACK PAY, offer cashless payments to provide an added incentive for loyalty through coupon and discount integration. Starbucks, EDEKA and Netto, however, offer solutions that can only be used in their respective shops. PAYBACK PAY, which is based on the idea of collecting points, currently has several hundred thousand users in Germany. Out of this number, the majority is also using PAYBACK PAY via the app, which provides a mobile card, coupons and a contactless payment function.

Convenience is not readily available in the German mobile payment market

Since they offer varied levels of functionalities, this myriad of solutions on the German market is not always in direct competition between each other. For example, Google Pay and Apple Pay do not offer a cheap and reliable solution for P2P transfers and bill splitting. paydirekt has a P2P transfer feature, but only offers online payments and no contactless payments. PAYBACK PAY offers contactless payments, but not online payments. It is clear that an average German consumer, willing to digitalize their finances and payment habits, needs to use a multitude of solutions and apps. Convenience is not readily available.

In order to be successful in the German market, mobile payment providers need to keep pace with changing consumer demands by offering not only POS, but also online and P2P payments, while providing a high level of security at all times. Customers will continue to expect more convenient solutions tailored to their individual needs.

This article was written by students of the CEMS Master at Vienna University of Economics and Business (WU) during their business project in cooperation with zeb. Special thanks to:

Jonas Badenhop, Alessandro Buffoli, Julienne Feria, Rafael Garcia Lopes, Marta Mirowska, Valentine Sharmar and David Žic

Jonas Badenhop, Alessandro Buffoli, Julienne Feria, Rafael Garcia Lopes, Marta Mirowska, Valentine Sharmar and David Žic[1] Both players are also simultaneously offering Apple Pay

![Thede Küntzel, Manager Projects & Innovation at Sparkasse Bremen and Managing Director of ÜberseeHub GmbH.]](https://www.bankinghub.eu/wp-content/uploads/2023/04/thede-kuentzel-bankinghub-768x549.jpg)