How do trading platforms for crypto assets work?

Operating a trading platform for crypto assets involves managing one or more multilateral systems. These platforms facilitate the technological execution of buy and sell orders by matching various crypto asset orders. Consequently, the platform enables trading transactions through the exchange of crypto assets for fiat money or other crypto assets.

A crypto asset trading platform allows market participants to place buy and sell orders for crypto assets. The platform operator is responsible for ensuring that crypto asset trading activities run smoothly. Additionally, they must provide trading participants with a valid, MiCAR-compliant white paper before including new crypto assets in their trading offering.

The following functions are essential for the operation of a trading platform:

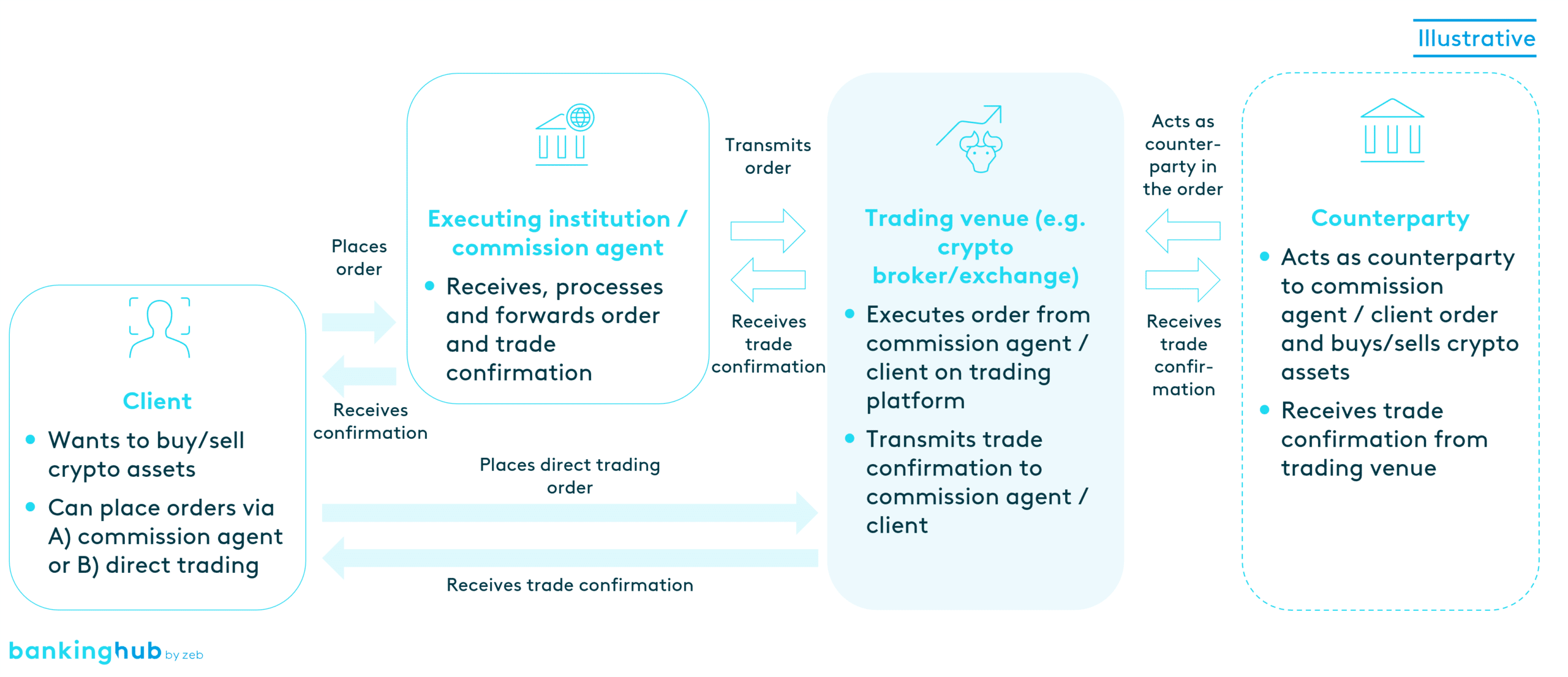

- Acceptance of orders: The trading platform receives orders, which are generally placed directly by market participants (private and institutional investors) or through commission agents. The buy and sell orders received are recorded in an electronic order book. The characteristics of the orders are also taken into account. This includes, for example, the type of order. A daily market order is executed during the course of the day at the best possible price. A limit order, on the other hand, is executed when certain price/unit thresholds are reached.

- Matching orders: The platform matches buy and sell orders by bringing together buyers and sellers. This is based on the order book, which ensures that an incoming buy order is paired with a matching sell order and vice versa. Orders are matched according to defined rules that take into account priorities based on price (e.g. a buy order with a higher price is executed first) and time (e.g. if two orders have the same price, the earlier order is given priority).

- Execution of transactions: Once a buy and sell order are matched, the transaction is executed on the platform. The buyer receives the crypto assets, and the seller receives the agreed equivalent (in cryptocurrencies or fiat money) in return. The transaction is marked as final in the order book. The final transaction data is forwarded to the respective financial institutions / crypto asset service providers for unit delivery and cash settlement. The crypto asset trading platform also publishes completed transactions, current bid and ask prices and trading volumes in real time.

The operation of a crypto asset trading platform often involves processing thousands of transactions per day, as well as numerous trading requests during normal trading hours. In exceptional situations, such as financial crises, wars, and pandemics, extreme peaks in the number of transactions and trading requests to be processed can occur, exceeding the operations during normal trading hours many times over. Accordingly, an efficient and secure trading platform for crypto assets must be provided by the operator to ensure reliable and efficient processing of transactions at all times.

In addition, the trading platform must ensure that price information is transparent and made available to all market participants simultaneously in order to create fair and transparent market conditions. Buy and sell orders must be executed in a fair and non-discriminatory manner.

Best execution policies must also be implemented for transactions and their recording in transactions must be ensured and demonstrated to the supervisory authority. It must also be ensured that all users of the platform are treated equally, regardless of their size or trading volume.

What are the regulatory requirements?

In order to offer the operation of a trading platform for crypto assets in the EU, specific requirements and procedures must be met, which are defined in regulations such as MiCAR. This is similar to the provisions of MiFID II for the operation of MTFs and OTFs, although no distinction is made between MTFs and OTFs.

The activity is further defined as the management of a multilateral trading facility that brings together the interests of a large number of third parties in the purchase and sale of crypto assets in a manner that results in a contract, by exchanging one crypto asset either for another or for fiat money.

The trading platform must comply with the requirements of MiCAR regarding authorization pursuant to Article 59 et seq. and the operating rules of the platform, in particular pursuant to Article 76, as well as the transparency and disclosure obligations pursuant to Article 20. These include requirements for monitoring transactions, preventing market manipulation and protecting against money laundering and terrorist financing (AML/CFT guidelines).

In addition, there are further requirements relating to the proper organization of the business. Platform operators are subject to ongoing supervision by the national supervisory authority and are required to submit regular reports on their activities and compliance.

In addition to the MiCAR, the DLT pilot regime is of particular interest. It enables the creation of decentralized market infrastructures based on distributed ledger technology (DLT) and facilitates the trading and settlement of financial instruments as defined by MiFID II. Financial institutions that already operate a trading platform for traditional securities can obtain a temporary authorization from the supervisory authority to operate a DLT-based trading venue. Simplified requirements apply to the operation of the DLT-based trading venue in order to test innovations.

Related digital asset services according to MiCAR: