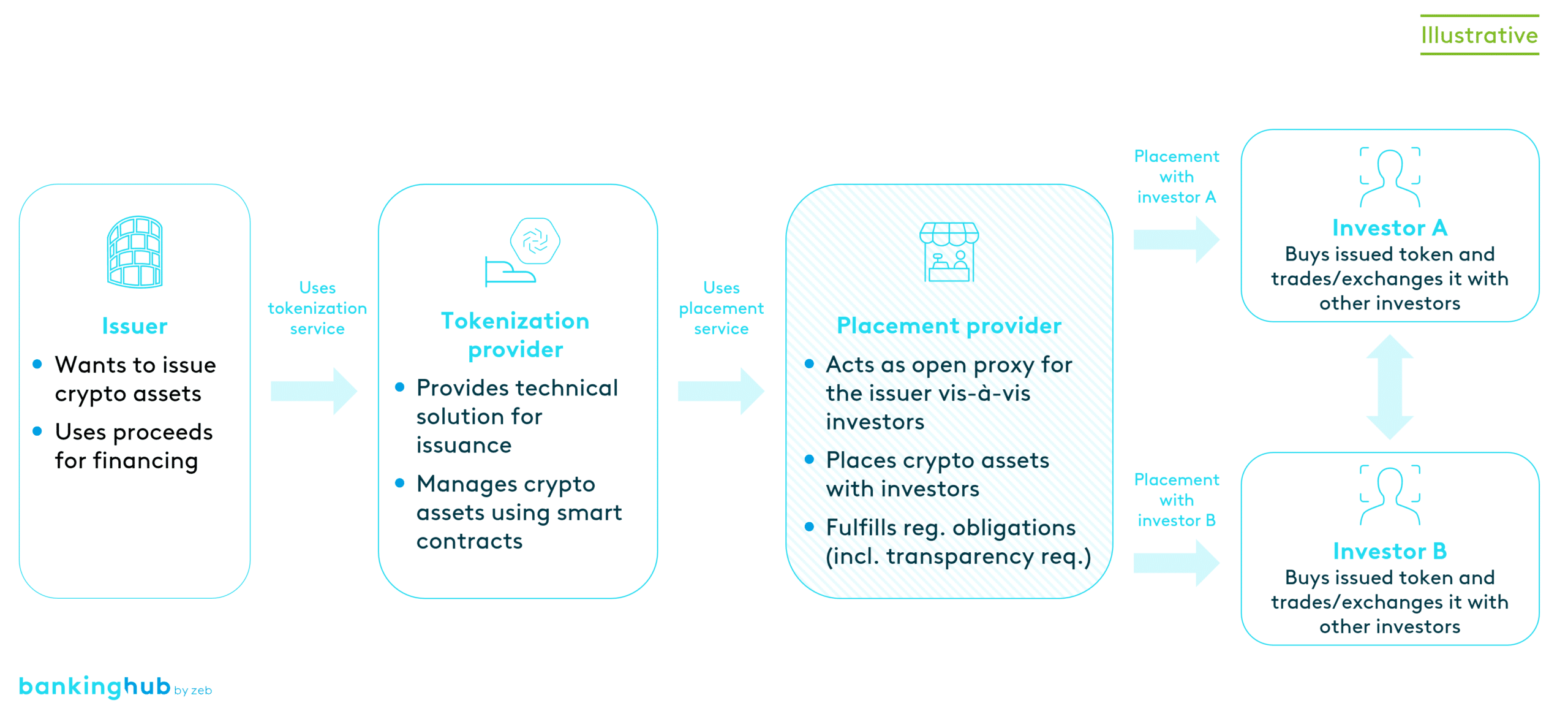

How does the placement of crypto assets work?

The business of placing crypto assets describes the marketing of crypto assets to buyers on behalf or for the account of the provider or a party affiliated with the provider.

The placement business is a special form of contract brokerage where the financial institution acts as an open agent for the client (principal) in the course of a placement of crypto assets.

When crypto assets are placed without a firm underwriting commitment, the sale is made on behalf and for the account of a third party. The issuance is not part of the placement process itself but is often related. For instance, a service provider may issue crypto assets on behalf of a third party to fund their business. After the initial issuance, these crypto assets are offered (“placed”) by the placement provider, who may also issue the crypto asset at the same time.

What are the regulatory requirements?

The European regulation for crypto assets MiCAR (Market in Crypto-Assets Regulation), which comes into force in 2025, sets out comprehensive rules for the placement of crypto assets. A financial institution wishing to place crypto assets must have specific and appropriate procedures in place to prevent, monitor, manage and disclose conflicts of interest. This applies in particular to conflicts of interest that arise when institutions place crypto assets with their own clients, or when the proposed price for the placement of crypto assets is set too high or too low.

Pursuant to Article 79 MiCAR, crypto asset service providers wishing to place a crypto asset must obtain the following information and the consent to the information from the issuer:

- Type of placement under consideration, including whether a minimum amount of purchase is guaranteed or not

- Amount of transaction fees

- Timing, process and price for the proposed operation

- Information about the targeted purchasers

Besides the requirements for the crypto asset service provider, there are additional requirements for the issuer who commissions the placement.

Prior to the placement, a white paper must be published that summarizes the most important information for investors in a comprehensible manner. In particular, it must include the purpose of the placement, information about the issuer and provider as well as important trading information. The white paper must specify the name of the crypto asset service provider appointed to place the assets and the type of placement (with or without a firm underwriting commitment).

MiCAR also sets out cryptocurrency-specific requirements for client information, redemption and issuance restrictions in terms of investor protection. In addition, it specifies the information to be provided to investors prior to issuance and outlines procedures for identifying, avoiding, managing and disclosing conflicts of interest.

Related digital asset services according to MiCAR: