How does buying and selling crypto assets work?

In the context of buying and selling crypto assets, the following services of crypto asset service providers are relevant:

- Reception and transmission of orders in the sense of investment brokerage

- Execution of orders for crypto assets in the sense of financial brokerage

- Exchange of crypto assets for fiat money or other crypto assets in the sense of proprietary trading

The transmission and execution of orders for third parties and the exchange of crypto assets for fiat money or other crypto assets play a critical role in the crypto markets, enabling private and institutional investors to efficiently invest in cryptocurrencies.

The services are differentiated as follows:

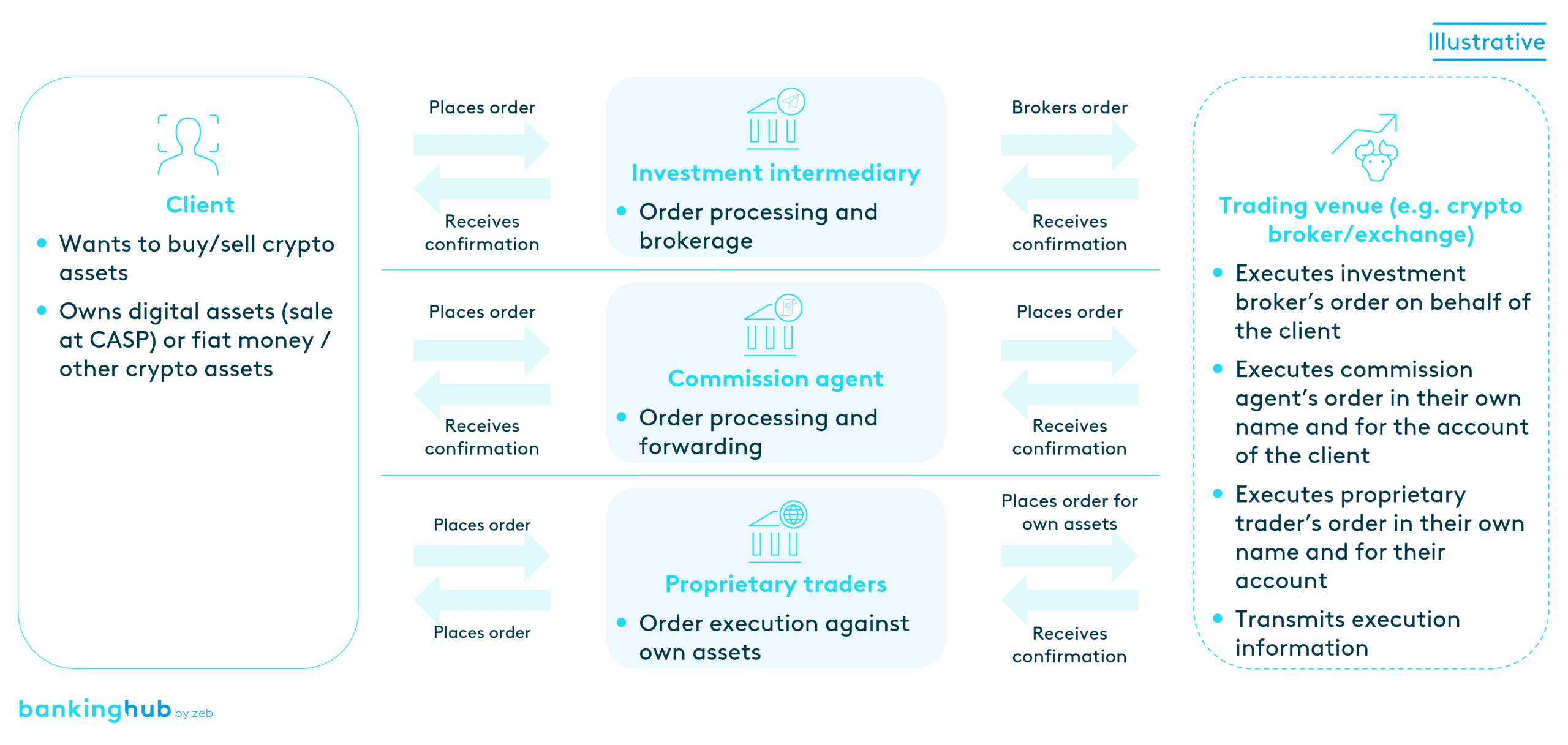

- Investment brokerage: Article 80 MiCAR “Reception and transmission of orders for crypto-assets on behalf of clients” describes investment brokerage services. The client places their buy or sell order with their crypto asset service provider (intermediary), specifying the order information (including the number of units). The intermediary forwards the order to another crypto asset service provider for execution, without acting as a trading partner.

- Commission business: Article 78 MiCAR “Execution of orders for crypto-assets on behalf of clients” describes the commission business. The client places their buy or sell order with their crypto asset service provider (commission agent), specifying the order information (including the number of units). The commission agent executes the order with another crypto asset service provider in its own name, but for the account of the client.

- Proprietary trading: When “exchanging crypto-assets for funds or other crypto-assets” in accordance with Article 77 MiCAR, the client places their buy or sell order with their crypto asset service provider, specifying the order information (including the number of units). The crypto asset service provider has previously informed the client of the terms and conditions and executes the client’s order directly against its own holdings. The crypto asset service provider’s own holdings were previously purchased by the crypto asset service provider in its own name and for its own account.

Irrespective of the service, it is necessary for the client to have the corresponding liquidity in fiat money / crypto assets via a deposit or a corresponding credit line in their settlement account / wallet prior to placing their order. The crypto asset service provider ensures that the client has sufficient funds available for their order by means of a liquidity check.

The placement of an order involves the following main steps:

- Order placement: The client provides essential order information (number of units and execution period) and transmits their buy or sell order to the crypto asset service provider. As part of the disclosure and transparency obligations, the client is provided with up-to-date market information (including prices) and an ex-ante statement of the fees likely to be incurred.

- Order acceptance: The crypto asset service provider receives and processes the buy or sell order.

- Order forwarding: In the case of investment brokerage (Article 80 MiCAR), the order is forwarded to another crypto asset service provider.

- Execution: The crypto asset service provider executes the order on a trading platform in its own name but for the account of the client and buys or sells the crypto assets (Article 78 MiCAR). Best execution requirements must always be met in order to achieve the best possible result for the client. The decisive factors are price, costs, speed, probability of execution and settlement.

- Alternatively, the crypto asset service provider may execute the client’s order directly against its own holdings (Article 77 MiCAR). Prior to this, the client must be informed of the conditions under which the client order will be directly executed (e.g. execution price). Crypto assets must also be procured by the crypto asset service provider prior to the transaction.

- Closing: Once the order has been successfully executed, the trade will be closed and the client will receive either the number of crypto assets acquired (in the case of a purchase) or the proceeds of the crypto asset in fiat money or other cryptocurrencies (in the case of a sale). Upon completion of the transaction, the client must be provided with comprehensive information about the transaction and the fees incurred.

What are the regulatory requirements?

From 2025, the regulation of trading in crypto assets will be governed by EU standards under MiCAR (Markets in Crypto-Assets Regulation). In line with traditional banking supervisory law, the regulatory approach here is also dual, i.e. product- and service-specific.

E-money (fiat-based stablecoin), value-referenced (e.g. gold-linked stablecoin) and non-value-referenced tokens (e.g. cryptocurrencies) are regulated by MiCAR. This regulation governs the transmission and execution of orders for crypto assets on behalf of clients, as well as the exchange of these assets for fiat currency or e-money.

These MiCAR services are also subject to classic securities trading regulations such as best execution (including price, costs, speed, probability of execution), disclosure, and transparency obligations (including ex-ante fee statements) in the course of executing the trading transaction.

With regard to client due diligence obligations, crypto asset service providers must also ensure transparency with regard to selection criteria and client requirements when onboarding clients.

Related digital asset services according to MiCAR: